INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

ISSN 2277-8616

Using Computer Techniques To Predict OPEC Oil

Prices For Period 2000 To 2015 By Time-Series

Methods

Mohammad Esmail Ahmad, Ali Jalal Hussian, Monem A. Mohammed

Abstract: The instability in the world (and OPEC) oil process results from many factors through a long time. The problems can be summarized as that

the oil exports don’t constitute a large share of N.I. only, but it also makes up most of the saving of the oil states. The oil prices affect their market

through the interaction of supply and demand forces of oil. The research hypothesis states that the movement of oil prices caused shocks, crises, and

economic problems. These shocks happen due to changes in oil prices need to make a prediction within the framework of economic planning in a short

run period in order to avoid shocks through using computer techniques by time series models.

Keywords: Fluctuations in oil prices, prediction, Time-Series Forecasting, computer techniques, Holt Winter, Exponential Smoothing, Analyzing

Techniques, Stationary, information technology.

————————————————————

INTRODUCTION

Oil is important for the entire world, so it doesn’t play as

good as a vital role in economic life as the oil play in

underdeveloped countries. Clearly, oil is the economic life

for countries that have oil, such as Venezuela, Middle East,

Arabian Gulf and North Africa. Oil exports do not constitute

a large share of national income only. Also, it makes up

most of the saving of the oil states. Therefore, Oil is the

primary Source of capital needed for economic

development. Also, Oil as fuel is indispensable for modern

agriculture and industry sector in addition to being a major

fuel meets needs to secure the necessary consumption. So

we can summarize importance of Oil and the role in the

following properties: [2]

1. It could be considered as a key driver of the global

economy.

2. It could be considered as a major or source of energy

within the global economy.

3. It could be considered as more strategic goods traded.

4. It significantly contributes to the G.D.P of underdeveloped countries.

5. It significantly contributes to the government revenues

of underdeveloped countries.

6. It significantly contributes to the balance of payments of

underdeveloped countries.

7. It can contribute to creating interdependence between

industry, agriculture, and services.

_____________________

Assis. Lect. Mohammad Esmail Ahmad is a lecturer at

University of Sulaimani, M.Sc. in the field of Computer

Science, E-mail: mohammad.ahmad@univsul.edu.iq

Assis. Prof. Dr. Ali Jalal Hussian is a lecturer at

University of Sulaimani, PhD in the field of Economics,

E-mail: alijalal4@yahoo.com

Prof. Dr. Monem A. Mohammed is a lecturer at

University of Sulaimani, PhD in the field of Statistics,

E-mail: monem_aziz2003@yahoo.com

1.1 The Research Problem:

Can be summarized as that oil prices affect their market

through the interaction of supply and demand forces of oil

according to tracker for evolution of oil prices to historic

periods of times characterized by large and volatile swings,

sometimes up and down movement due to upward and

downward economic activity for global economy between

stagnation and growth, which is reflects positively or

negatively impact on prices.

1.2 The Research Hypothesis:

The research hypothesis states:

―The movement of oil prices (downward and upward)

caused shocks, crises, and economic problems.‖ These

shocks happen due to changes in oil prices need to make

forecasts within the framework of economic planning in a

short run period in order to avoid shocks.

1.3 The Research Importance:

Time-Series is one of the most important predictive

methods in short-run term because of its importance in the

field of economic planning in general and in particular of

prices. The researchers resorted to use computer

techniques (Microsoft Excel, Statistical Analysis Software

Package-SPSS) and forecasting method (Time-series), in

addition to the analytical method for analyzing the reality of

oil prices in the period of research.

1. THEORETICAL FRAMEWORK

The importance of forecasting in economics field had been

expanded due to increasing of economic problems, it make

adoption of economic planning to avoid these problems. It

came when economic fluctuation happened to avoid losses

in potential resources. The forecasting conducts demands

and prices to make the possibility to apply economic

policies in order to affect demands and prices in different

levels. So predictability needs to increase using economic

indicators such as price elasticity to make policies in order

to overcome problems. The evolution in the field of

computer and information systems generate accuracy of

predictions. [11]

223

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

2.1 The Stages of Forecasting:

The prediction process doing through following stages: [1]

1. Building model: It makes through building model.

2. Estimating model: It makes that building model to find

the data for economic variables in the models, and

choice the relevance method for estimating according

to computer requirement and prediction specification.

3. Evaluate model: It makes building model to analyze the

economic indicators from where the sign and value of

estimated coefficient within the framework of economic

theory.

4. Preparing forecasts through using data accurate

predictions.

2.2 Forecasting Methods:

There are different methods and techniques for forecasting

according to the different level of complexity, the theoretical

foundations, and Statistical requirement. So the methods

used vary about the accuracy of forecasts. The major

technique for forecasting is time-series. It’s interested in

analyzing the time – trend of the economic phenomenon to

be predictable. Forecasting is very important for prediction

of the feature events .Science and computer technology

together has made significant advances over the past

several years and using those advanced technologies and

few past patterns, it grows the ability to predict the future

.Feature prediction is a process of choosing the best subset

of the features available from the selected input data .The

best subset contains the minimum number of dimensions

that contribute more accuracy. [12]

2.3 Time Series Model:

Some models such as the Oil pricing model and the

arbitrage pricing model described as time series data.

However, there is much to be said for analyzing data

without imposing constraints that are implied by a theory.

The aim of time series analysis is to find the most

appropriate statistical model for the data and to use this

model for prediction. In this way, the variables are allowed

to speak for themselves. Without the confine of economic

theories. In Oil markets, the modelling procedures for return

data and for price data are different to understand why. On

needs to draw the basic distinction between stationary and

non-stationary time series Daily and Monthly return data on

most Oil markets are generated by stationary processes

and consequently returns. In fact, they are often rapidly

mean-reverting since there is very little autocorrelation in

many oil market returns. The statistical concepts and

methods that apply to return data do not apply to price data.

For example volatility and correlation are concepts that only

apply to stationary processes it makes no sense to try to

estimate volatility or correlation on price data. Daily (log)

price data are commonly assumed to be generated by a

non-stationary stochastic process. [7]

2.4 Concept of Information Technology:

Human started from ancient to think about how to arrange

their works with methods that guarantee them the best use

of time and effort, with the appearance of computerized

machines which have had a significant role in the conduct

of business, and gradually the computer programmer

emerged, causing a growth in all aspects of scientific,

technical and administrative life as it began this

ISSN 2277-8616

renaissance leading investment into the world of

technology.The term Information Technology (IT) has

appeared in the early seventies with the emergence of

electronic computer on a commercial scale, and the

concept of information technology means all the things that

include computers of various types and data processing in

all its forms and information and all the centers and

functions related to technology and services in

organizations and institutions, as well as software and

programming packages that are used in doing business,

jobs, and product marketing. [8] ―Information Technology

(IT) may be defined as the technology that is used to

acquire, store, organize, process, and disseminate

processed data which can be used in specified applications.

Information is processed data that improves our knowledge,

enabling us to take decisions and initiate actions‖. [13]

2.5 Importance of Information Technology:

The Importance of (IT) can be summarized as the following:

[16]

1. Information Technology works on major changes in the

entire organization, as in their products, markets, and

gives employees the flexibility to work anywhere either

in their organizations or at home.

2. Provide more information to assist controlling the

decisions taken by their users.

3. Help to create new communication channels, therefore,

it increases flowing, processing and exchanging

information and develop modern management

methods.

4. Works to improve and increase business opportunities

between organizations, and between organizations and

the government, which led to a wider spread of

information.

5. Helps detecting deviations to prevent the aggravation

and work on a specialized processor.

6. Helps to improve customer service by meeting their

demands via terminals.

7. Improves the quality of work through the adoption of

new technological methods and thus achieve high

accuracy, shorten the time, reduce costs and risk of

humanitarian unprepared interpretation of the

information and data.

8. Contributes to reduce the volume of the costs which

allocated to provide factors of production.

9. Improves the process of collecting, processing, storing,

retrieving, updating and reducing cost of data as it

would reduce the cost of administrative work.

10. Creating the most effective managerial tools to apply

what can be applied in the normal conditions and

leading the renewal process.

2.6 Component of Information Technology:

Information technology consists of the following five parts,

as shown in (Figure 1): [10]

224

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

ISSN 2277-8616

the next period. Mathematically, a moving average forecast

of order k is as follows: [5]

𝐹

=

∑

Where;

2.

3.

4.

5.

𝐹

= 𝑓𝑜𝑟𝑒𝑐𝑎𝑠𝑡 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒𝑠 𝑠𝑒𝑟𝑖𝑒𝑠 𝑓𝑜𝑟 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡

+1

𝑌 = 𝑎𝑐𝑡𝑢𝑎𝑙 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑖𝑟𝑒𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡

The term moving is used because every time a new

observation becomes available for the time series, it

replaces the oldest observation in the equation and a new

average is computed. As a result, the average will change,

or move, as new observations become available.

Fig. 1: Component of Information Technology

1.

(1)

=

People: The most important part as they make endusers more productive.

Procedure: Refer to rules or guidelines people follow

when using software, hardware, and data. Documented

in manuals written by computer specialists and

provided by software/hardware manufacturers of the

product.

Software: It is the term for programs or sets of

computer instructions written in a special computer

language that enables a computer to accomplish a

given task. It consists of step-by-step instructions,

which the computer can use to convert data into

information.

Hardware: Refers to physical, touchable pieces or

equipment.

Data: Raw, unprocessed facts including text, numbers,

images and sounds. Data describes something that is

stored electronically in a file.

2.7 Statistics by MS-Excel:

There are a number of commonly used, powerful tools for

carrying out statistical analyses. The most popular of these

are Statistical Package for the Social Sciences (SPSS),

Statistical Analysis System (SAS), Stata, Minitab and R.

Many researchers choose to apply Excel as their major

analysis tool or as a complementary to each other tools for

any of the following reasons: [19]

1. It is widely available and so many researchers already

know how to use it.

2. It is not necessary to pay the cost of another tool (as

some of the popular tools are quite expensive).

3. It is not necessary to learn new methods of manipulating

data and drawing graphs.

4. It provides numerous built-in statistical functions and

data analysis tools.

5. It is much easier to see what is going on since, unlike

the more commonly used statistical analysis tools, very

little is hidden from the user.

6. It provides the user with a lot of control and flexibility.

2.8. Techniques Used:

2.8.1 Moving Average:

The moving averages method uses the average of the most

recent k data values in the time series as the forecast for

2.8.2 Exponential Smoothing:

Exponential smoothing uses a weighted average of past

time series values as a forecast; it is a special case of the

weighted moving averages method in which we select only

one weight—the weight for the most recent observation.

The weights for the other data values are computed

automatically and become smaller as the observations

move farther into the past. The exponential smoothing

equation follows: [6]

𝐹

Where;

= 𝛼𝑌 + 1 − 𝛼 𝐹

(2)

𝐹 = 𝑓𝑜𝑟𝑒𝑐𝑎𝑠𝑡 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠 𝑓𝑜𝑟 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡 + 1

𝑌 = 𝑎𝑐𝑡𝑢𝑎𝑙 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡

𝐹 = 𝑓𝑜𝑟𝑒𝑐𝑎𝑠𝑡 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠 𝑓𝑜𝑟 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡

𝛼 = 𝑠𝑚𝑜𝑜𝑡𝑖𝑛𝑔 𝑐𝑜𝑛𝑠𝑡𝑎𝑛𝑡 0 ≤ 𝛼 ≤ 1

2.8.3 Double Exponential Smoothing:

Charles Holt developed a version of exponential smoothing

that can be used to forecast a time series with a linear

trend. The smoothing constant α to ―smooth out‖ the

randomness or irregular fluctuations in a time series; and,

forecasts for time period t + 1 are obtained using the

equation: [6]

𝐹

=𝐿 +𝐵 𝐾 +𝜖

(3)

Forecasts for Holt’s linear exponential smoothing method

are obtained using two smoothing constants, α and _, and

three equations:

𝐿̂ = 𝛼𝑌 + 1 − 𝛼 𝐿̂

+ 𝐵̂

𝑏̂ = 𝛽(𝐿̂ − 𝐿̂ ) + 1 − 𝛽 𝑏̂

𝐹 = 𝐿̂ + 𝑏̂ 𝑘

(K=1,2,…,n)

(4)

(5)

(6)

Where;

𝐿 = 𝑒𝑠𝑡𝑖𝑚𝑎𝑡𝑒 𝑜𝑓 𝑡𝑒 𝑙𝑒𝑣𝑒𝑙 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡

𝑏 = 𝑒𝑠𝑡𝑖𝑚𝑎𝑡𝑒 𝑜𝑓 𝑡𝑒 𝑠𝑙𝑜𝑝𝑒 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡

𝛼 = 𝑠𝑚𝑜𝑜𝑡𝑖𝑛𝑔 𝑐𝑜𝑛𝑠𝑡𝑎𝑛𝑡 𝑓𝑜𝑟 𝑡𝑒 𝑙𝑒𝑣𝑒𝑙 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠

𝛽 = 𝑠𝑚𝑜𝑜𝑡𝑖𝑛𝑔 𝑐𝑜𝑛𝑠𝑡𝑎𝑛𝑡 𝑓𝑜𝑟 𝑡𝑒 𝑠𝑙𝑜𝑝𝑒 𝑜𝑓 𝑡𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒𝑠

𝐹 = 𝑓𝑜𝑟𝑒𝑐𝑎𝑠𝑡 𝑓𝑜𝑟 𝑘 𝑝𝑒𝑟𝑖𝑜𝑑𝑠 𝑎𝑒𝑎𝑑

𝑘 = 𝑡𝑒 𝑛𝑢𝑚𝑏𝑒𝑟 𝑜𝑓 𝑝𝑒𝑟𝑖𝑜𝑑𝑠 𝑎𝑒𝑎𝑑 𝑡𝑜 𝑏𝑒 𝑓𝑜𝑟𝑒𝑐𝑎𝑠𝑡

225

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

2.8.4 Holt-Winters: (Triple exponential smoothing):

Holt (1957) and Winters (1960) extended Holt’s method to

capture seasonality. The Holt-Winters seasonal method

comprises the forecast equation and three smoothing

equations—one for the level ℓ , one for trend 𝑏 , and one

for the seasonal component denoted by 𝑆 , with smoothing

parameters 𝛼, 𝛽 and 𝛾. We use 𝑚 to denote the period of

the seasonality, i.e., the number of seasons in a year. There

are two variations to this method that differ in the nature of

the seasonal component. The additive method is preferred

when the seasonal variations are roughly constant through

the series, while the multiplicative method is preferred when

the seasonal variations are changing proportionally to the

level of the series. With the additive method, the seasonal

component is expressed in absolute terms in the scale of

the observed series, and in the level equation, the series is

seasonally adjusted by subtracting the seasonal

component. Within each year, the seasonal component will

add up to approximately zero. With the multiplicative

method, the seasonal component is expressed in relative

terms (percentages) and the series is seasonally adjusted

by dividing through by the seasonal component. Within

each year, the seasonal component will sum up to

approximately. [22]

It contains three equations: [11]

𝑆 =

+ 1 − 𝑎 {𝑆

+ 𝑏̂

for t= (1,2,..,n) and L=12

}

(7)

Time-Trend Preliminary Equation

(9)

+ 1−𝛽 𝑖

From the three equations above, we get the following

Preliminary Exponential Tripartitly equation:

= {𝑆 + 𝑏̂ 𝑚 }𝐼

(10)

for m=(1,2,…)

2.9 Stationary Time Series:

Let, we have stationary time series {𝑍 ; 𝑡 = 0 ± ,1 ± 2, … },

then, we have the following ARMA (P, q) process: [18]

𝑍 = ∅𝑍 + ∅ 𝑍

− . . . −𝜃 𝛼

Where 𝑍 = 𝑍̃ – μ

+

Then, ARMA (1, 1) distributed Gaussian or normal

distribution.

By using (𝐵) operator we get:

𝑍 {1 − ∅ 𝐵 − ∅ 𝐵 −. . . −∅ 𝐵 }

= {1 − 𝜃 𝐵 − 𝜃 𝐵 −

∴𝑍 =

{𝑍 =

{

{

∅

∅

𝑎}

... ∅

Where

}

}

𝑎

−𝜃 𝐵 }𝑎

(12)

are

𝛩 𝐵 𝑎𝑛𝑑 𝛷 𝐵

the

polynomial functions of order (q) and (p) in (B) respectively.

𝑜𝑟 { 𝑍 = 𝜓 𝐵 𝑎 } where:

1

=𝜓 𝐵 +𝜓 𝐵 +𝜓 𝐵 +𝜓 𝐵 +

𝜓 𝐵 =

(13)

=∑

𝜓 𝐵 =

𝜓 𝐵 ,𝜓 = 1

,𝜓 =

𝜓 = 1, 𝜓 , 𝜓 , ψ , … are the weights.

-

+∅ 𝑍

+

+

With (k = 0, 1, 2 ...), and by using covariance form with lag

(k) is (𝑅 ) then, we have:

Seasonal Preliminary Equation

𝜃𝛼

Covariance of (𝜕 , 𝜕 ± ) = 0, for all k ≠ 0.

Let the auto correlation with lag (k) is:

𝐸 𝑍 .𝑍

= ∅ 𝐸 𝑍 .𝑍

+∅ 𝐸 𝑍 .𝑍

∅ 𝐸 𝑍 .𝑍

+ 𝐸 𝑎 .𝑍

− 𝜃 𝐸 𝑎 .𝑍

−

𝜃 𝐸 𝑎 .𝑍

− −𝜃 𝐸 𝑎 .𝑍

(15)

for t= (1,2,..,n)

𝑍

and

By using Yule – walker equations we get the (ACF) as

follows:

for t=(1,2,..,n) and L= 4

𝐼 =

Variance of (𝜕 )= E (𝜕 )2 =𝜎

For St. Time series (𝑍 , (t = 1, 2, 3… n) [17]

𝑍 = ∅ 𝑍 +∅ 𝑍

+ ....+ ∅ 𝑍

+𝑎 - 𝜃 𝑎 - 𝜃 𝑎

... - 𝜃 𝑎

(14)

(8)

+ 1−𝛾 𝑏

For each (t), (μ) is the mean of time series and {𝑎 }is a

purely random error (white noise) distributed Gaussian with

E (𝜕 )= 0,

2.10 Autocorrelation Function of the Autoregressive

Moving Average Model:

General Preliminary Exponential Equation

𝑏 =𝛾 𝑠 −𝑠

ISSN 2277-8616

+𝛼 −𝜃 𝛼

𝑅 = ∅ 𝑅

+∅ 𝑅

+ +∅ 𝑅

+ 𝐸 𝑎 .𝑍

−

𝜃 𝐸 𝑎 .𝑍

− 𝜃 𝐸 𝑎 .𝑍

− − 𝜃 𝐸 𝑎 .𝑍

(16)

Now, 𝐸 𝑎 . 𝑍

= 0 𝑓𝑜𝑟 𝑘 > 𝑡 .

So, 𝑅 = ∅ 𝑅

+∅ 𝑅

+ +∅ 𝑅

, with (k ≥

q+1)

Let the (ACF) is: 𝜌 =

, (k = 0 ± ,1 ± 2, … .

Then, 𝜌 = ∅ 𝜌

q+1)

∴ 𝜌 =

−

(11)

∑

∑

+∅ 𝜌

+

+∅ 𝜌

, (k = 0 ± ,1 ± 2, …

with (k ≥

(17)

For example: for AR(1) process we have:

𝜓 = ∅ , with |∅ | < 1

By substituting in AR(1) process we get the ACF of AR(1)

as follows:

226

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

∑

=

∑

=0 ± ,1 ± 2, … .

∑

∑

∅ ∅

∅

=

∅

∅

∅

= ∅ ,

With

(k

2.11 The Partial Autocorrelation Function:

The autocorrelation function of an MA series exhibits

different behavior from that of AR and general ARMA series.

The (ACF) of an (MA) series cuts of sharply whereas those

for (AR) and (ARMA) series exhibit exponential decay (with

possible Sinusoidal behavior superimposed). This makes it

possible to identify an (ARMA) series as being a purely

(MA) one just by plotting its autocorrelation function. The

partial autocorrelation function provides a similar way of

identifying a series as a purely (AR) one. Given a stretch of

time series values:

𝑍

,𝑍

,…,𝑍

+

+∅ 𝑍 + 𝑎

Denoted the (i) regression parameters and (𝑎 ) is a

normal error term, uncorrelated with 𝑋

for 𝑗 ≥ 1 But

the additional correlation between (𝑍 ) and (𝑍 ) after their

mutual linear dependency on the intervening variables

{𝑍 , 𝑍 , … , 𝑍

, } has been removed which is usually

followed by a conditional autocorrelation as:

∅

= Cor Z , Z

|Z

So the results shown in the bellow table:

Table 1: Time series model indicators:

,𝑍 ,…

The partial correlation of (𝑍 ) and (𝑍 ) is the correlation

between these random variables which is not conveyed

through the intervening values. If the (𝑍 ) values are

normally distributed, the partial autocorrelation between (𝑍 )

and (𝑍 ) can be defined as the partial autocorrelation

function can be thought of as the partial regression

coefficition ∅ in the representation: [14]

𝑍 =∅ 𝑍

+∅ 𝑍

Where: ∅ ; 𝑖 = 1,2, … , 𝑘

3.1 Descriptive model:

The researchers used Microsoft Excel to estimate the

following time series methods forecasting OPEC oil prices

for period (2000-2015):

1. Time series moving average smoothing.

2. Time series exponential smoothing.

3. Time series Double exponential smoothing.

4. Time series Holt winter-(additive) model.

5. Time series Holt winter-(Multiplicative) model.

6. Time series Holt winter-(No Trend) model.

∅

,

∅

,

And

=

= ∅ −∅

∑

,

∅

,

, (j=1, 2, ... k)

3. PRACTICAL FRAMEWORK

b

55.030

c

56.943

d

55.357

e

57.455

f

54.847

120

100

80

60

40

20

0

Jan-00

(18)

∅

66.444

140

,…,Z

∅

M.S.E.

a

Time Plot of Actual Vs. Forecast

And after solving the equations of general formula to

determining the initial estimates for parameters (∅ ) and

(∅ ) under the stationary condition we have: [11]

∑

Model

The above table shows that the mean squares error

(M.S.E) indicates that the minimum value is (54.847) in

spite of (Holt winter no-trend), but this value is still high

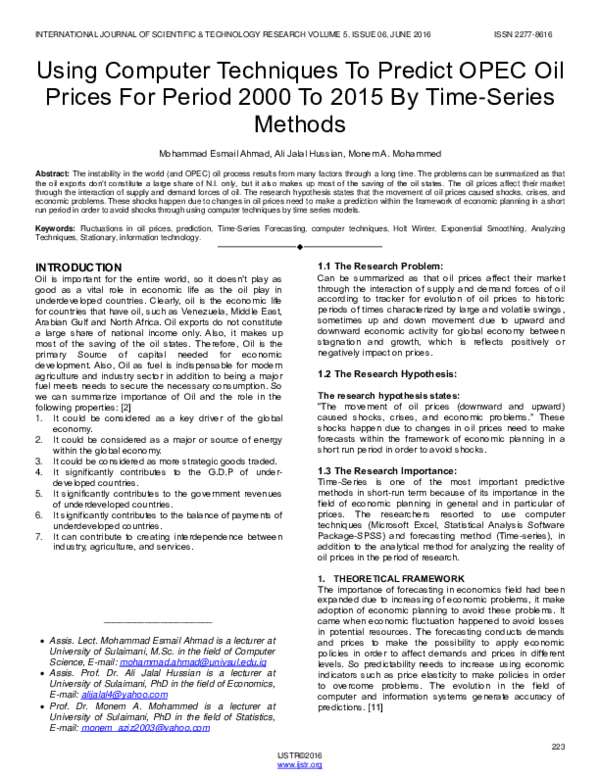

level. We can show, in (Figure 2), the time plot of actual Vs.

Forecast data as bellow.

US $/Barrel

𝜌 =

ISSN 2277-8616

Forecast

Actual

Sep-02

Jun-05 Mar-08 Dec-10 Sep-13

Jun-16

months

Fig. 2: represent the actual price oil Vs. Forecast price oil

(19)

In our research, we gather data of Oil basket price for the

period of Jan 2000 to Feb 2016. We use different methods

to predict the price for next 6 months with the help of

computer system using Microsoft Excel and SPSS

technology, then carried out a comparative study of nine

different forecasting technique. The data set is used, was

collected from the OPEC & OAPEC organization. [21]

We conclude that the model above (f) suffer from

Autocorrelation

problem,

because

the

estimators

characterized by non-stationary estimators.

3.2 Box and Jenkins models analysis:

To analysis the data of (Oil-Price) by using (Box and

Jenkins) models to show the problem of the data in time

series, we can applied the following steps in order to

overcome the problem by using SPSS system:

227

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

Step (1): The actual Sequence Series plot:

ISSN 2277-8616

Step (4): The ACF and PACF of the first difference of

sequence series Plots:

Fig 3: represent the actual Sequence Series plot

Step (2): The (ACF and PACF) of actual sequence series

Plots:

Fig. 7: represent the (ACF and PACF) of the first difference

of sequence series plot

Step (5): From analysis all (Box and Jenkins) models, we

consider the following (ARIMA) Models to forecasting the

(Oil –Prices) in year (2016):

Table 2: Represented the (ARIMA) models:

Fig. 4: represent the (ACF and PACF) of actual sequence

series plot.

Models

R-Square

R MSE

BIC

ARIMA(0,1,2)

0.949

7.350

4.072

ARIMA(2,1,2)

0.949

7.347

4.126

ARIMA(2,1,0)

0.949

7.368

4.077

ARIMA(2,1,1)

0.949

7.386

4.109

From above table we show that the best model is ARIMA (0,

1, 2) has the less values of (R MSE = 7.350, Bic = 4.072)

and has the greatest (R- square = 0.949).

Table 3: Represent Forecasting (ARIMA) models in year

(2016):

Fig. 5: represent the first difference of actual sequence

series plot

Step (3): Take the first difference for Sequence series plot

as follows:

Models

193

194

195

196

197

198

199

200

ARIMA

(0,1,2)

ARIMA

(2,1,2)

ARIMA

(2,1,0)

ARIMA

(2,1,1)

33.

27

32.

33

33.

29

33.

29

31.

87

34.

01

32.

20

32.

14

31.

90

35.

43

32.

21

32.

06

31.

94

34.

28

32.

06

31.

89

31.

97

33.

04

32.

10

31.

90

32.

00

33.

91

32.

10

31.

90

32.

04

35.

12

32.

13

31.

92

32.

07

34.

62

32.

16

31.

95

From above table we show the range of predicted oil prices

for (6) months, approximately between 31 $ to 33 $ for

barrel.

Step (6): We can find the estimate the parameters of

(ARIMA (0, 1, 2) Model as follows:

Fig. 6: represent the first difference of actual sequence

series plot

228

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

Table 4e: Forecast:

t

Sig.

.605

.054

.957

Difference

1

.748

.456

Lag 1

.054

.072

Lag 2

-.193

.072 -2.680

.008

Table 4b: Model Statistics:

ztModel

0

.036

Rsquare

d

Model

Number of

Predictors

Model Fit statistics

Stationa

ry

Rsquared

MA

E

Ljung-Box Q(18)

Normalize

Statisti

d

DF Sig.

cs

BIC

4.31

0

.949

Model

SE

.033

4.072

193

194

195

196

197

198

199

zt-Model_1

U

Forec

C

ast

L

Estimate

Constant

200

33.27 31.87 31.90 31.94 31.97 32.00 32.04

32.07

47.77 51.83 57.81 62.66 66.85 70.60 74.01

77.18

18.77 11.91

-13.04

L

C

L

No

Transformatio

n

Zt

zt-Model_1

Table 4a: ARIMA model Parameters:

MA

ISSN 2277-8616

6.00

1.21

-2.91

-6.59

-9.94

For each model, forecasts start after the last non-missing in

the range of the requested estimation period.

10.467 16 .841

Mod

el

Table 4c-1: Residual ACF:

1

2

3

4

ztModel_1

ACF .003 -.006 .017

SE

.072

.072

5

6

-.031 -.046

.040

.072 .072 .072 .073

Fig. 8: Time plot of actual VS Forecast. ARIMA estimated

model

ztModel

_1

Mo

del

Table 4c-2: Residual ACF:

7

8

9

10

11

12

ACF -.066 -.116 -.058 .073 .097

SE

.073

.073

From the figure above, we show that the actual values VS

predicted values are very approach, which means the

estimators are best and stationary.

.074 .074 .075

.040

4. CONCLUSIONS

.075

ztMod

el_1

Mod

el

Table 4d-1: Residual PACF:

1

2

3

4

5

6

PACF

.003

-.006

.017

-.040

-.031

-.047

SE

.072

.072

.072

.072

.072

.072

ztModel

_1

Model

Table 4d-2: Residual PACF:

7

8

9

10

11

12

PACF

-.065

-.118

-.062

.067

.095

.031

SE

.072

.072

.072

.072

.072

.072

The researcher reaches to the following major conclusion:

1. The oil price was fluctuates through long-term period.

And it causes shocks, crises and many economic

problems for OPEC countries.

2. The necessity of oil price in economies of oil generates

to make prediction for oil prices in order to subjugate

that in planning to avoid the economic problems.

3. The famous and the best method or forecasting is time

series, that it plays important role for this purpose.

4. The estimated model, (Moving average, exponential

smoothing, and Holt winter) suffer from Autocorrelation

problem, so we must to overcome this problem.

5. By using (Box and Jenkins) models we proved that

ARIMA (0,1,2) is the best estimated model which

become greater stationary and has less Mean squared

Error (M.S.E).

6. The range predicted (oil –prices) of OPEC for next six

months approximately between 31 $ to 33 $ for barrel.

7. Any change upper or down the range above is affected

by exogenous variables.

229

IJSTR©2016

www.ijstr.org

�INTERNATIONAL JOURNAL OF SCIENTIFIC & TECHNOLOGY RESEARCH VOLUME 5, ISSUE 06, JUNE 2016

5. REFERENCES

5.1 Books and Researches:

[1] Abraham, B. and LEDOTER, J. 1983, ―Statistical methods for

forecasting‖, Johan Wiley, NEWYORK.

[2] Al-HEETY, A., 2000, ―Economies of petrol, Mosel University

Pub., Mosel (Arabic Reference).

[3] Al-MAZINI, E., 2013, ―The factors affect the fluctuations in

world oil prices (2000-2010)‖, Al-AZHAR University Journal –

Gaza, human sciences, vol. 15, Nov.

[4] Anderson, T.W, 1971, ―The statistical analysis of Time series,

John Wiley, NEWYORK.

[5] Anderson, D., Sweeney, D., 2015, ―Modern Business statistic

with Microsoft Excel‖, CENGAGE learning Pub., NEWYORK.

ISSN 2277-8616

[17] TSAY, R.S., and TIAO, G.C., 1948, ―Consistent estimates

Autoregressive Parameters and extended sample

Autocorrelation function for stationary and non-stationary

ARIMA models‖, JASA, Vol.79, No.384.

[18] WEI, w.w.s.1990, ―Time series methods‖.

[19] ZAIONTS, C., 2015, ―Statistics using EXCIL Succinctly, Sync

fusion Inc.

5.2 Electronic Websites:

[20] www.marketoracle.co.uk

[21] www.opec.org

[22] www.otexts.org/fpp/7/5

[6] Anderson, D., Sweeney, D., Williams, T., 2011, ―Statistics for

Business and Economics‖, Eleventh Edition, CENGAGE

Learning pub., NEWYORK.

[7] Box, G.E.P. and Jenkins, G.M., 1976, ―Time series analysis

Forecasting and control, Holden-Day Inc., San Francisco.

[8] El-DABAGH, M., 2010, ―Design of Instant-Mail System using

infrastructure of information and communication technology‖,

Higher Diploma thesis, Mosul University – college of

Administration and Economic, (Arabic Reference).

[9] ESMAEEL, N., 1981, ―Determine the Arabian Crude oil

Prices in the world Market‖, AL-RASHID Pub., Baghdad

(Arabic reference).

[10] JAWAD, B., 2013, ―Wide Preaching and Information

Technology and their Impact on Achieving customers

satisfaction‖, Master thesis, Karbala University – college of

Administration and Economic, (Arabic Reference).

[11] MONEM M.A. 2011, ―The analysis and Forecasting in Time

series‖, SULIMANI University Pub., SULIMANI. (Arabic

reference).

[12] PADHY, N., and PANIGRAHI, R., 2012, ―Engineering

information Technology, International Journal of computer,

Vol.2, NO.5, Oct.

[13] RAJARAMAN, V., 2013, ―Introduction to Information

Technology‖, second edition, PHI learning Private Limited.

[14] SIM, C.H., 1978, ―AMIXED GAMMA ARAMA (1, 1) Model for

river flow Time Series‖, Water resources research, Vol.23,

NO.1.

[15] SPYROS, M., Steven, C., and ROB, J., 1998, ―Forecasting

methods and applications‖.

[16] SULTAN, S., 2005, ―Health information technology and its

impact on job satisfaction – a study on opinions of sample of

health technologies users in Ibn Sina & El-Khansa

educational Hospital‖, Master thesis, University of MosulCollege of Administration and Economic, (Arabic Reference).

230

IJSTR©2016

www.ijstr.org

�

mohammad E.

mohammad E.