Special issue article: Financialisation and the production of urban space

Financial markets, developers and

the geographies of housing in Brazil:

A supply-side account

Urban Studies

1–21

Ó Urban Studies Journal Limited 2015

Reprints and permissions:

sagepub.co.uk/journalsPermissions.nav

DOI: 10.1177/0042098015590981

usj.sagepub.com

Daniel Sanfelici

CAPES Foundation, Brazil

Ludovic Halbert

Université Paris-Est Latts, France

Abstract

Financialisation and housing are predominantly associated to mortgages for homeownership and

securitisation techniques. This paper looks at how financial markets influence the development

industry, its business strategies, and the nature and location of its products. Adopting a supplyside account, the paper inquires into the rising role of financial markets as a source of funding for

a consolidating development industry and its influence on the geography of housing in Brazilian

cities. It develops the concept of resonance by combining two yet unrelated strands of literature

on the study of financial markets (cultural economy and conventionalist economics). Narratives

co-authored by the stock market community and development firms management over each individual firm, and the discursively linked strategic moves of developers, are shown to resonate, at

the meso-level of the industry, into shared social representations (or conventions) on how to

best assess and interpret the value of development firms. Analysing the wave of Initial Public

Offerings occurring in the mid 2000s, the paper highlights that narratives of quick capital gains

associated with the removal of the land banking bottleneck faced by developers supported a convention giving priority to the growth in total output, and contributed to the observed changes in

the forms, scales and locations of housing projects in Brazilian cities. As discrepancies between

the promises of returns for shareholders and actual financial results emerged, the growth convention unravelled, making way for other narratives and strategic moves to resonate anew and possibly change again the geographies of housing.

Keywords

Brazil, developers, financialisation, geography of housing, stock market

Received August 2013; accepted May 2015

Introduction

The literature dealing with the financialisation of the urban built environment devotes

Corresponding author:

Daniel Sanfelici, CAPES Foundation, Ministry of Education

of Brazil, Brasilia DF-70040020, Brazil.

Email: danielsanfelici@gmail.com

Downloaded from usj.sagepub.com by guest on June 20, 2015

�2

Urban Studies

attention to the pervasiveness of financial

markets and how it affects access to homeownership, household indebtedness, housing

prices and the geographical patterns of mortgage lending. However, this focus on access

to homeownership and its social and spatial

implications overlooks how financial markets influence the supply side of the housing

sector – that is, the development industry, its

business strategies and the nature and location of its products. Following this research

agenda, the paper aims to analyse the evolving interrelations between financial markets

and the development industry, and how

these interrelations contribute to redefining

the geographies of housing production in

Brazilian cities.

Contrasting with a ‘mechanic, relational

concept of the economy’ (Froud et al., 2006:

69), the paper questions a view where developers’ strategies and the resulting geographies

of housing would be a straightforward

embodiment of the ‘logics’ of shareholder

value. Rather, combining two strands of yet

unrelated approaches to financial markets

(cultural economy and conventionalist economics), the paper develops the concept of

resonance to grasp the interactions between a

given industry (housing development in this

case) and financial markets. Considering

with Froud et al.’s cultural economy perspective that the shareholder value theory is

a ‘pliable rhetoric’ (2006), the paper pays

attention to the narratives on individual

firms that are co-authored by the stock market community (investors, analysts, the business press, etc.) and firm managers. While

such narratives are performative in the sense

that company managers have to make strategic moves, there is nothing predetermined in

the content of such moves. Thus, developers’

managers are given back the agency they lost

in more mechanistic accounts. Yet to understand how the fragmented narratives and

strategic moves relating to each individual

firm may contribute to reshaping the

geographies of housing, one has to look at

their aggregated outputs. This calls for a

complementary perspective at a meso-level

that stresses how shared social representations (or conventions) support the coordination of financial actors. Conventionalist

economics helps to move from the description of the idiosyncratic narratives on individual organisations and to analyse how

financial markets adopt dominant valuation

and interpretation conventions that affect a

group of firms considered to share similar

characteristics (such as belonging to the

same industry). There is however a need for

a unifying concept to reconcile both strands

of literature. The paper brings forward the

concept of resonance to explain the interactions whereby (1) fragmented narratives on

individual firms, and their related strategic

moves, eventually vibrate in unison and stabilise into a shared representation on an

industry’s fate, and reciprocally, (2) how

conventions evolve as financial results

diverge from dominant narratives and call

for alternative strategic moves by managers.

Resonance does not only ground the analysis

in actual economic practices, in contrast to

macro-political economy accounts, it also

contributes to a literature that attempts to

go beyond restrictive binary distinctions

(between micro- and meso-levels, between

stock market communities and company’s

management). It constitutes, therefore, a

heuristic tool to analyse the interactions

between financial markets and developers,

the related changes in Brazil’s housing industry, and their potential impacts on the urban

built environment and its geography.

Focusing on Brazil provides a unique

vantage point for clarifying such relation. If

the housing sector was mostly made up of

small-scale family-owned firms, a wave of

initial public offerings (IPOs) in the mid

2000s brought a group of developers under

the pressure of the stock market community.

Relying on a qualitative analysis, the paper

Downloaded from usj.sagepub.com by guest on June 20, 2015

�3

Sanfelici and Halbert

explores (1) how a convention centred on

growth (of outputs and revenue) took shape

as these firms went public between 2005 and

2007; (2) how this convention unravelled

between 2010 and 2011 as financial results

diverged from shared expectations, leading

to mounting tensions between the actors

involved; and, finally, (3) what consequences

the emergence and dissolution of this convention centred on growth had on the geographies of housing provision in Brazil.

Financialisation, housing and

developers: The case for a supplyside analysis

‘Centring housing in political economy’,

authors such as Aalbers and Christophers

(2014) or Schwartz and Seabrooke (2008),

have stressed how housing finance systems

are key in understanding today’s political

economy, if only because homes are a major

financial asset in most economies (Schwartz

and Seabrooke, 2008: 238). With the rising

importance of mortgages, and, in ‘liberal’

residential systems, the securitisation of such

mortgages (Rolnik, 2013; Schwartz and

Seabrooke, 2008), housing and financialisation are said to be intrinsically linked,

households and their homes becoming financialised subjects (Forrest, 2015; Langley,

2007). The genesis, politics, modus operandi

and resulting spatial, social and racial consequences of subprime lending offers a vivid

illustration of such growing interdependencies between finance and housing (see the

contributions to Aalbers, 2012, as well as

Ashton, 2009; Carruthers and Stinchcombe,

1999; Poon, 2009).

Yet, financial markets also connect to

housing through the development industry,

i.e. not only via homeownership by households, but also through the production of

housing by development firms. While taking

into account this supply-side perspective is

important in all countries, it is of particular

interest for the Global South where the

influence of mortgages and their securitisation remain limited. In so-called ‘emerging’

countries that adopted neoliberal reforms,

the role of financial markets in the financing

of firms increased, while, at the same time,

global capital availability has escalated,

especially in the 2000s. The development

industry is no exception: cash-consuming

developers are eager to resort to

private equity funds and stock markets to

boost their growth (Rouanet and Halbert,

2015).

For research focusing on the supply-side,

there is a tradition concerned with how debt

lavishly provided by financial institutions to

property developers leads to boom-and-bust

cycles (from Haussmann’s Paris through

1980–1990s London’s Docklands to 2000s

Halifax, Canada: Fainstein, 1994; Harvey,

2003; Rutland, 2010). However, only a handful of work has touched upon how finance

capital transforms housing provision by

investing equity into development firms. Ball

(1983) observed, for instance, how Initial

Public Offerings (IPOs) could alter development companies by providing the means to

increase their total volume of production,

and to rescale country-wide. However, it was

only recently that this initial probing was

revived by works exploring how finance capital flows are ‘anchored’ in urban spaces

(David and Halbert, 2014a; Theurillat and

Crevoisier, 2014), making a case for a systematic analysis of the interrelations between

financial markets and the development

industry.

In this light, some recent contributions

have considered how their ties with financial

markets can transform not only developers’

strategies but also the resulting geographies

of the built environment. It is demonstrated

how in India, developers are among the

intermediaries of the ‘transcalar territorial

network’ that channels foreign and domestic

finance capital into metropolises (Halbert

Downloaded from usj.sagepub.com by guest on June 20, 2015

�4

Urban Studies

and Rouanet, 2014). These developers leverage such capital flows to increase their market share over a wider number of regional

markets. Consequently, they gain political

agency in the making of contemporary

Indian metropolises (Rouanet and Halbert,

2015). In Mexico, David (2013) analysed

how small local developers changed

their organisation, business model and

reporting practices to meet foreign financial

investors’ expectations. Already dominant

developers, having access to alternative

sources of funding, nonetheless managed to

shut out global financial investors from central markets of the Mexico city-region

(David and Halbert, 2014b). This hints at

recognising the agency of developers that

pursue their own agenda and interests

(Searle, 2014).

In spite of this growing number of empirical accounts on the interactions between two

parallel processes (increasing presence of

finance capital in the development sector, on

the one hand, and changing business strategies of developers that impact the geographies of the urban built environment, on the

other), more work is needed to formulate a

conceptual framework to explain such

interactions.

Financial markets and corporate

management: Towards a theory of

resonance

Froud et al. (2006) discusses existing conceptual frameworks that theorise the relations

between financial markets and the corporate

economy. For them, mainstream financial

economics, in the form of agency theory, as

well as its political economy opponents (such

as the regulation school or the varieties of

capitalism approach) share a unidirectional,

arrow-to-box understanding (Froud et al.,

2006: 130) where financial markets act as the

driving force behind the evolutions in a

given industry. Consequently, it is

shareholders’ capital accumulation strategy

that would impose itself onto development

firms and be reflected in the evolving geographies of housing provision. However, by

claiming the efficiency of financial markets

in the allocation of capital, or by criticising

the hegemony of shareholders, both

accounts dismiss the agency of firms’ management. This results in downplaying the

interactions between financial actors and

development firms, two sets of organisations

whose interests, values and views have

empirically been observed to diverge at times

(David and Halbert, 2014b; Searle, 2014).

To move beyond such ‘mechanistic’ thinking

(Froud et al., 2006: 69), two yet unrelated

fields in the studies of financial markets, i.e.

cultural economy and conventionalist economics, can fruitfully be combined.

Considering that economics – i.e. discourses and representations on the economy

– formats economic objects rather than the

other way round (Pryke and Du Gay, 2007),

Froud et al. (2006) pursue a cultural economy perspective to reconsider the dominant

representation in financial markets known

as the shareholder value theory (SVT) from

the 1980s onwards. For them, SVT is a

highly ‘pliable rhetoric which can be borrowed, used and influenced ‘ (Froud et al.,

2006: 38). If its bottom line focuses on

potential pecuniary returns for shareholders,

it is enacted through the daily interactions

between the stock market community and

company managers. The analysis of these

interactions reveals how a company’s strategy is thus the subject of multiple narratives

co-authored by fund managers, analysts, the

business media but also by firms’ managers,

and borrowing from different discursive levels (company-, industry- and grand macroeconomic narratives). Following the cultural

economy approach, narratives are performative: they constrain corporate managers

to demonstrate that they act accordingly.

Yet, under a British intellectual tradition

Downloaded from usj.sagepub.com by guest on June 20, 2015

�5

Sanfelici and Halbert

revolving around MacKenzie’s works, performativity remains for Froud et al. (2006)

essentially open in the forms it effectively

takes. Managers devise the ‘strategic moves’

they see fit as long as they remain discursively tied to the shareholder value rhetoric.

Yet, claiming that financial returns are redistributed to consumers rather than to shareholders because of the intense price

competition in present-days’ product markets, Froud et al. observe that numbers, read

financial results, may frequently not corroborate the narratives. These discrepancies

lead to a new round of narratives and ‘strategic moves’ that might equally prove financially unfruitful, and so on.

This conceptual framework that holds

together narratives, strategic moves and

numbers, is particularly fit for analysing

individual firms through thick historical case

studies (see examples on GE or Ford, Froud

et al., 2006). However, since the work is

rooted in management studies, and because

of the reticence, in contrast with political

economy works, to engage in any totalising

account, the priority is given to the description of idiosyncratic interactions between the

stock market community and the managers

of a given firm, i.e. at micro-level. It does not

recognise that the myriads of narratives and

strategic moves may converge across firms

of a given sector, as if vibrating in unison. It

consequently weakens any attempt to examine how idiosyncratic interactions relate to

the meso-level, and how their convergence

can influence, in our case, the evolving geographies of housing.

While not considering micro-level interactions between financial actors and corporate

management, the conventionalist approach

to finance provides elements to explore such

a meso-level. Extending the interest paid by

conventionalists to the coordination of economic agents, this approach insists on the

role of shared social representations (also

known as conventions) in the valuation of

firms and the on interpretation of their outlook by financial actors. Orléan’s seminal

work (1999) discusses how shared ‘interpretation conventions’ (Orléan, 1999: 145) gain

legitimacy among financial actors, possibly

leading to boom-and-bust cycles, as more

investors abide by the dominant convention.

Other authors have complemented this

approach by stressing how ‘valuation convention’ are key to their coordination

(Lavigne, 2002; Tadjeddine, 2006: 195):

financial actors share similar interpretations

not only of the future values of companies,

but also on the elements that need to be

looked at to value companies (such as preference for EBITDA multipliers over Price/

Earning Ratios). The attention paid to the

mechanisms by which financial actors coordinate their investment decisions through

shared social representations goes beyond

the fragmented analyses at micro-level. But

only as long as one does not fall into the

trap that, akin to mechanistic accounts,

would consider the predominance of financial markets as inevitable, or at least, unmediated by company managers. Influenced by

a proclaimed Marxist approach (Orléan,

2004: 17), the conventionalist approach of

finance may be inclined to adopt such an

assumption, so that conventions are often

depicted as endogenous to the stock market

community, paying little if any attention to

the agency of management firms. Using a

conventionalist perspective, D Lorrain’s

analysis of the French electricity sector

demonstrates however that in their interactions with financial intermediaries, ‘managers find some room for manoeuvre, allowing

them to negotiate with ‘‘what the [financial]

market says’’’ (Lorrain, 2009: 62).

It is pressing to reconcile both perspectives to analyse how firms’ business strategies respond to the pressure of financial

markets, and, in our case, how the production of housing by developers may be

affected. To do this, we consider how the

Downloaded from usj.sagepub.com by guest on June 20, 2015

�6

Urban Studies

narratives co-authored by the stock market

community and developers’ managers over

individual firms resonate into financial

valuation and interpretation conventions on

the wider housing development industry. By

resonance, we point to how the multiple

interactions happening between corporate

managers and shareholders around each

individual organisation mutually influence

those occurring around other firms, and

temporarily stabilise, as if progressively

vibrating in unison, into a dominant convention applied to a subset of firms considered

by the actors to be part of an industry. In

this light, the circulation of industry-wide

and grand economic narratives is key in putting individual company narratives in resonance (arguably irrespective of the fact that

organisations do effectively share common

elements or not, as evoked by Froud et al.,

2006). Resonance thus provides a dynamic

understanding of how conventions are made

and remade over time as an interactive process between the stock market community

and developers’ management. As discrepancies between narratives and numbers are

repeatedly observed at micro-level, dissonances in the dominant convention occur,

leading to another round of narratives and

performative actions which will resonate

anew, at least until another wave of disappointment crashes against the (renewed) promises of pecuniary returns for shareholders.

Resonance is thus a concept that brings

back the question of power relations into

economic activity and of their effects. On the

one hand, the process of resonance may

encourage convergence in management

initiatives. As such, it constitutes an important but still overlooked factor to explain the

transformation in the provision and geographies of housing by developers. On the other

hand, it may also not go unchallenged: some

actors, such as corporate managers in firms

whose capital is still partially controlled by

founding families and individuals, can raise

diverging views, and offer resistance to the

adoption of the ‘strategic moves’ accompanying dominant narratives (David and

Halbert, 2014b for empirical illustrations;

Searle, 2014) as will demonstrate the casestudy of housing production in Brazilian

cities.

To fruitfully analyse this process of resonance, the research protocol seeks to go past

binary distinctions (between micro- and

meso-levels, as well as between the financial

market community and its object, i.e. firms’

management). Thus the research collected

evidence that clarifies (1) the business strategies of listed developers and how they affect

the provision of housing in Brazilian cities,

and (2) the narratives shared by the stock

market community, and occasionally contested by other actors, concerning the adequate evaluation of the housing industry.

This material consists of secondary sources

including selected business press material

(media outlets such as Exame, Valor

Econômico, Construcxão Mercado, Istoé

Dinheiro, etc.), periodical reports issued by

developers to shareholders containing operational and financial information, as well as

transcripts of teleconferences between managers and shareholders. This documentary

corpus was triangulated with primary data

from 15 interviews with development firms’

managers and business analysts conducted

between August 2011 and May 2012 in the

cities of São Paulo and Porto Alegre.

Fifty years of housing finance in

Brazil

To understand the interactions between

financial markets and developers in the

2000s, one first needs to see how growing

demand for housing challenged the existing

housing finance system in Brazil.

Residential development activity took

shape as a distinctive sector in Brazil in the

1960s (Fix, 2011; Ribeiro, 1996). Previously,

Downloaded from usj.sagepub.com by guest on June 20, 2015

�7

Sanfelici and Halbert

lack of a national mortgage finance system

had restricted homeownership to higherincome households. The Housing Finance

System (HFS), tightly regulated by a

National Housing Bank, was introduced in

1964. The HFS encompassed a marketoriented development sector, under which

savings deposits made by households provided mortgages for middle-income buyers

with interest rates defined by the central

government, and a social sector which used

compulsory savings (deposits made by

employers on behalf of employees) to

develop lower-income housing projects, most

of them managed by municipal governmentcontrolled housing cooperatives (Arretche,

1990; Maricato, 1987; Valenc

xa, 1999).

Combined with an accelerating pace of economic and demographic growth, as well as

rapid urbanisation, the new availability of

housing finance supported strong demand

for housing in the 1970s (Maricato, 2011;

Royer, 2009). This opened up opportunities

for development firms to grow (Farah, 1985;

Fix, 2011). Yet, the sector remained predominantly composed of small and mediumsized family-controlled firms operating in

their hometown markets. This was due in

part to the hurdles that managing a nationwide business in a large territory with limited

transportation and communication infrastructure presented. Additionally, and of

central importance to subsequent events, was

that the HFS restricted development finance

solely to the covering of construction costs.

As the capital markets of Brazil were still

weak in the 1960s, finance to scale up activity through land banking was scarce.

Brazil’s economic growth stalled in the

1980s as the Latin American foreign debt crisis unfolded. Mortgage lending plummeted

as a result of rising default rates among borrowers, and the National Housing Bank was

dissolved in 1986. During most of the 1990s,

faltering growth, rising unemployment, monetary austerity and poor coordination

among the agencies managing the HFS system further sapped mortgage lending and

construction finance (Azevedo, 1996; Royer,

2009; Valenc

xa, 1999; Valenc

xa and Bonates,

2010). Development firms were forced to

adapt by directly financing homebuyers

through off-plan sales or through housing

co-operative schemes, often on five- or tenyear loan contracts (Castro, 1999). By immobilising capital in such loans, firms lacked

the resources to expand their businesses.

Developers thus remained small and

medium-sized firms, controlled by their

founding owners, with a strong specialisation both in terms of geographical reach (targeting a single regional market) and of

segment (catering for middle and upper

income households who could afford shortterm loans).

A new scenario began to emerge at the

beginning of the 2000s. Brazil’s economic

outlook improved as a result of higher

growth rates, falling unemployment and rising incomes. Furthermore, a series of regulatory changes and new tax incentives

enhanced support for mortgage lending. In

order to introduce mortgage securitisation

in Brazil, deeds of trust were permitted on

mortgage contracts (Law of Sistema de

Financiamento Imobiliário – SFI, 1997). It

was argued that these would improve security for lenders who had long complained

about the obstructions posed by the judicial

system on foreclosures (Royer, 2009). While

mortgage securitisation did not subsequently

grow as expected,1 deeds of trust nevertheless helped to boost conventional mortgage

lending through the HFS, especially when

interest rates started to fall in 2005: the number of households annually financed

increased from 200,000 before 2005 to more

than 1 million in 2010.

Development firms responded to this surging demand in different ways. Some opted

for organic growth, eschewing radical

changes in managerial and organisational

Downloaded from usj.sagepub.com by guest on June 20, 2015

�8

Urban Studies

structures. Others embraced more radical

expansion plans, but lack of finance for land

banking remained an obstacle. The solution

found was to team up with local and international financial actors. This was facilitated

by a sudden abundance of liquidity which

resulted from the combination of (1) incentives and regulatory changes from the

government to make investing in Brazil’s

stock exchange more attractive (Paulani,

2008), and (2) growing numbers of foreign

investors seeking to boost their portfolio

performance via investments in supposedly

higher-yield ‘emerging’ markets. Between

2003 and 2007, developers were thus able to

tap into the financial markets to acquire

land and expand their businesses.

Financial markets as growth

accelerator

The first movers were developers such as

Gafisa and Even, who partnered with private

equity firms. The former received an initial

investment in 1997 from GP Investimentos,

a Brazilian private equity fund that would

take full control of the firm in 2004. In 2005,

the US-based Equity International made an

additional BRL135 million investment in

exchange for a 32% stake in the same Gafisa

(Mandl, 2006). Similarly, in 2006 Even set

up a partnership with London-based

Spinnaker Capital, a private equity fund that

brought BRL 72 million (Aranha, 2011).

More common, however, was the case of

developers that attracted financial investors

by issuing stocks and bonds between 2005

and 2007 with the aid of underwriters such

as Credit Suisse, UBS Pactual, Merryl

Linch, Banco Votorantim and Deutsche

Bank. With the exception of Rossi, which

moved from a lower listing segment to the

newly created Novo Mercado segment of the

Bovespa Stock Exchange2 in 2006, the other

16 residential developers that issued stocks

in this period were not publicly listed

previously. It should be noted, however, that

differences in terms of ownership structure

persisted, depending on how influential

founding members remained after dilution.

Partnering with financial actors had

transformative effects on the housing development industry. First, while small, familybased local firms still populated the sector,

access to finance capital supported the concentration of development activity, especially in metropolitan areas. While data on

the extent of concentration are scarce, our

own empirical estimate is that in 2010, four

developers were responsible for one-quarter

of all new housing launchings in the metropolitan area of São Paulo. This is consistent

with Ball’s observation (1983): when developers issue stocks, the influx of capital allows

them to grow their market share because of

rising total output.

Alongside concentration through growing

output, what made possible this rapid gain

in market share was a wave of mergers,

acquisitions and partnerships that followed

the IPOs (Cichinelli, 2008a). By means of

this wave of activity, developers, hoping to

capitalise on expertise embedded within the

partnering or acquired firms, began to

develop for new market ‘segments’ and to

enter unfamiliar regional markets. PDG’s

chairman explained the thinking thus:

Where were the good professionals [in this market], which were few? The good professionals

were the owners of the firms that had managed

to survive in the 80s, 90s. These guys are not

available [for hiring] in the market. The only

way to get them to work for you is to acquire a

stake in their firms. This strategy has become

widespread in the sector. (Blanco, 2008)

Between 2007 and 2010, acquisitions grew

substantially. They involved large developers, as in the case of Gafisa’s acquisition of

the low-income segment specialist Tenda, or

PDG’s acquisition of Agre (Canc

xado, 2010).

However, joint ventures were more frequent,

Downloaded from usj.sagepub.com by guest on June 20, 2015

�9

Sanfelici and Halbert

associating listed developers with smaller

local developers and builders, especially

when entering a new regional market

(Rufino, 2012). Parallel to tighter horizontal

interactions between development firms,

denser vertical linkages were also established

between large developers and a range of real

estate organisations, such as business consultancies, architects, brokers and banks.

A second transformative effect concerned

the business organisation and governance of

developers. A clearer distinction was drawn

between owners and management teams,

even in cases where members of the owning

family continued to perform managerial

functions. This also involved attracting managers with professional careers in other sectors to positions that were either previously

filled by family members, such as financial

management, or that were created after the

IPOs, such as investor relations (Lindemann,

2008). The effects of these organisational

changes, perceived as beneficial by many,

were not limited to listed companies:

I believe it was good for shaking up the market, for improving governance [.].

Development activity had been going on since

1964 [.] but I believe it was upgraded with

[.] new funding, with regulatory improvements, and with the IPOs, [all of which] qualified governance in real estate development.

This is the role they [listed firms] had.

Competition with them was healthy for

smaller and medium-sized firms. (Interview

no. 3, Analyst, Sinduscon, November 2011)

Alongside the organisational dimension, to

attract private equity funds or as a prerequisite for taking part in Bovespa’s Novo

Mercado, developers had to demonstrate a

stronger commitment to transparency and

improved public relations with shareholders.

This involved the release of quarterly reports

with detailed operational and financial

results, holding teleconferences with investors and analysts, adoption of international

standards-based accounting procedures,

having balance sheets audited by one of the

‘big four’ multinationals, and arranging key

information releases in the business press

(Oliveira, 2008a).

Lastly, access to finance capital had a

transformative effect via the industrialisation

of developers’ business models. Developers

embraced project management technologies

and introduced information technology to

improve information exchange and enhance

cost control in the construction process

(Shimbo, 2012). Projects and product design

became standardised (Fix, 2011; Shimbo,

2012). Economies of scales were sought via

larger projects to reduce the marginal costs

(of land, project approvals, marketing .)

(Sanfelici, 2013; Sigolo, 2014). Lastly, most

firms embraced nationwide (as opposed to

local and regional) strategies of growth, as well

as segment diversification across income strata

(Olivion, 2010; Rufino, 2012; Sanfelici, 2013).

Concomitant to the access to financial

markets, developers grew significantly, as

demonstrated by both output trends

(Figure 1) and the evolution of their land

banks. For instance, Cyrela’s land bank

grew from 3 million m2 in 2005 to 13.6 million m2 in 2010 and the value of Gafisa’s

land bank rose from BRL3 billion in 2006 to

BRL18 billion in 2010.

In sum, the housing development industry

evolved rapidly in the course of the 2000s,

with a group of developers asserting dominance in larger geographical markets. Even

though such changes did not affect all markets equally, the restructuring had a distinctive impact on the urban built environment

in many Brazilian cities, both directly and

indirectly.

Changing the geographies of

housing provision

As developers expanded into new regions

and pushed for scale economies, their

Downloaded from usj.sagepub.com by guest on June 20, 2015

�10

Urban Studies

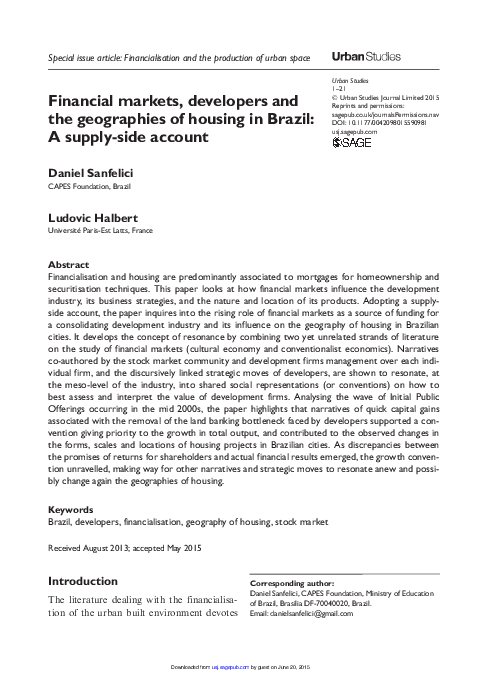

Figure 1. Housing starts by the seven largest listed developers (2004–2011).

Source: Firms’ quarterly reports.

activity left an imprint on major cities.

While large-scale projects were not a

novelty, they became more widespread as

these firms made headway in the market.

Apart from conventional apartment buildings, which continue to dominate densely

built-up areas where land is scarce, three

types of projects prevailed. Products for the

so-called lower-income ‘segments’ consisted

of highly standardised apartment blocks

(usually five-storey buildings with no elevator) and a few amenities, such as sports

courts. For middle- and upper-income ‘segments’, two types of projects became more

common: large-scale land developments and

mixed-use projects. The former includes

gated communities where land plots or

houses are sold to homeowners as well as

high-rise condos with in-house amenities

and some common infrastructure (streets,

lighting, parks) provided by the developer in

co-operation with local governments.3

Mixed-use projects usually group office, residential and retail functions in a single land

plot.

The spread of such projects have transformed the geographies of housing, especially in large cities (see Figure 2). Whereas

new developments had generally been concentrated in inner city, higher-income neighbourhoods throughout the 1990s and much

of the 2000s, they now spring up more and

more outside this core area (see Figure 3).

Because they require larger and cheaper land

plots to exploit economies of scale, lowerincome projects have been generally provided in the outskirts of urban areas, contributing to urban sprawl in cities that lack

efficient transit systems (Ferreira, 2012;

Klink and Denaldi, 2014; Maricato, 2011;

Cichinelli, 2008b). Middle- and upperincome land developments, although generally located outside denser, higher-value

neighbourhoods, are either near the city

core or within easy access of it through

major thoroughfares. Developers built

mixed-use projects on higher-value land,

catering to young professionals believed to

prefer areas of the city where cultural activities and entertainment are within easy reach

Downloaded from usj.sagepub.com by guest on June 20, 2015

�11

Sanfelici and Halbert

Figure 2. Large-scale projects in Porto Alegre: two higher-income land development projects (top) and

two lower middle-income condominiums (bottom).

Source: Photos taken in 2012, D Sanfelici.

(see Figure 3). As already suggested

(Ferreira, 2012; Maricato, 2011; Rufino,

2012; Volochko, 2012), these projects have

generally reinforced fragmented patterns of

land use. Many are inward-oriented as a

result inter alia of their combining different

functions, the availability of amenities that

act as a substitute for public space (parks,

sports courts, pools, etc.) and the security

apparatuses that inhibit or prevent circulation of outsiders.

The expansion of development firm activities into new regional markets has resulted

in the wider spatial circulation of these products into second-tier cities, a process supported by the subsidies included in Brazil’s

lower-income housing programme for

homeownership.4

There is thus strong evidence of systemic

relations between three processes: (1) the

growing role played by the stock market in

the ownership of housing development

firms; (2) changing business strategies of

these firms; and (3) redefinition of the geographies of housing in Brazil. It remains to

be explained how such interdependences

have occurred, by inquiring into the interactions between the stock market communities

and development firm managers.

The growth narrative

Following the cultural economy assumption

that discourses and representations on the

economy format economic objects, we can

observe how, in the 2005–2010 period, a

Downloaded from usj.sagepub.com by guest on June 20, 2015

�12

Urban Studies

Figure 3. Types of large-scale projects by selected developers in Porto Alegre (2007–2011) .

Source: D Sanfelici, based on developers’ quarterly reports.

narrative in favour of growth was coauthored by four main groups: developers,

underwriters, financial analysts and fund

managers. This narrative emerged with the

first IPOs of 2005 and encouraged the view

that development firms should be valued on

Downloaded from usj.sagepub.com by guest on June 20, 2015

�13

Sanfelici and Halbert

the basis of their ability to grow quickly.

The faster a firm grows, it was assumed, the

higher its turnover, and the higher capital

gains for shareholders thanks to rising stock

prices.

It was developers who originally devised

this narrative. Because, as noted in section

‘Fifty years of housing finance in Brazil’,

conventional bank lending could only be

used to cover construction costs, developers

turned to financial markets in order to facilitate land acquisition. In doing so, developers

argued that, by solving the land bank bottleneck, financial actors could legitimately

expect a strong growth in market capitalisation, reflecting soaring levels of housing production (Amato, 2008).

This was the key insight of firms in tapping

into capital markets: the business is too intensive in resource consumption. So firms saw it

in this way: ‘my turnover cannot be accelerated if I’ve got no money to invest [in land

acquisition, approval, etc]. How can I speed

up turnover? By getting access to investors’.

Thus the motivation behind IPOs was to

obtain land. They [developers] saw an opportunity [in the improving economic environment]. But then they’d say: ‘[.] I have all I

need except for money for buying land’. This

was their motivation [.]. They called investors and said: ‘Look, Brazil is doing well, this

is the economic outlook, from now on we have

a strong growth potential, but I need you as

my partner [.]’. Most developers pay only

the minimum [required by law] in dividends,

because all investors made a bet on growth.

(Interview no. 5, Analyst, Banco do Brasil,

November 2011).

Underwriters also endorsed this emphasis on

future growth since their fee-based revenue

model encouraged them to boost firms’ capital values at the date of IPO launch (Lima,

2007). Analysts corroborated development

firms’ narrative, first by espousing a broader

macro-economic forecast of strong growth

for the Brazilian economy as a whole,

second by mobilising industry-wide narratives ranging from government incentives

for the sector to promises of efficiency gains

associated to larger firms. Lastly, as excess

liquidity in the mid 2000s drove down interest rates in ‘developed’ economies, fund managers were eager to reap the benefits of

Brazil’s growth. The capital that flowed in

from the Global North was looking for

high-risk high-return investments to complement lower-return assets in their home

economies. In other words, investors were

looking for a scenario of quick capital gains

(through share price increase) rather than

long-term growth (and returns based on

dividends).

These narratives, which were elaborated

investment decision after investment decision, i.e. at the micro-level of each individual

developer, circulated within and across the

development and stock market communities

that were both mainly concentrated within

the city of São Paulo. Developers were forming an increasingly tightly bound community, based on similar professional interests

and interpersonal acquaintances. Interviews

reveal how the narrative based on the land

bank bottleneck was circulated among this

community as a way of attracting investors:

The idea of [emphasising] land bank appeared

in [.] 2005 when Cyrela went public and had

to show to investors [that] [.] [it] could grow

in the future. That’s how Cyrela managed [to

go public]. Until then no developer in Brazil

had had this idea of going to the stock

exchange. And this turned into a frenzy.

(Interview no. 3, Analyst, Sinduscon,

November 2011)

According to a manager at Cyrela, the

exchange of information between developers

at the IPO moment was key in shaping their

strategies:

The strategy [on IPOs] was one of growth. If

you look at all [firms’] reports, they sort of say

Downloaded from usj.sagepub.com by guest on June 20, 2015

�14

Urban Studies

the same thing, because firms copy each other.

There’s something called IPO prospectus. I

myself received calls from people of [other

firms] asking, ‘how should I do this or that’.

He [.] was preparing a prospectus. So all

firms followed [similar strategies]. (Interview

no. 2, Project manager, Cyrela, March 2012)

This narrative was taken up by the stock

market community, which progressively

expanded the idea of a growth scenario to

the entire development industry, thus seeing

in developers’ ‘investment thesis’ (Interview

no. 5, Analyst, Banco do Brasil, November

2011) an opportunity for profit. Through

the interactions within and across these two

communities, these narratives started to

resonate, culminating in the IPOs ‘window’,

which was concentrated between 2005 and

2007. All in all, the ‘land bank bottleneck’

provided a convenient story with its focus

on fast growth: under conditions of strong

housing demand and government incentives;

if the bottleneck could be removed, the turnover would quickly soar, giving a pecuniary

return to shareholders because of the resulting market capitalisation increase.

This dominant narrative supported – and

was enacted through – a valuation convention that spread across the stock market

community. The focus being on the capital

gains that could be derived from soaring

share prices, developers were valued on the

basis of elements that could signal future

growth in product output. Yet, the stock

market community (investors, analysts, business media) was uncertain as to what indicator should be given priority in assessing

prices, bringing evolutions in the valuation

convention.

Part of the impact of the markets on large cities [came from] this need for generating results.

Investors didn’t know where to look. There

was a history of analyzing firms [.] in manufacturing, in services, but the construction sector was [.] new to the stock exchange. What

criteria [should investors] use? In this uncertainty, one of the criteria they began using was

land bank. If you had a good land bank, it

meant you’d launch more, and at this point

developers rushed to build up their land banks,

causing land prices to rise. (Interview no. 4,

Analyst, Fundac

xão Getúlio Vargas, October

2011)

This initial emphasis on land banks was also

supported by IPO underwriters. Considering

the stock of land as an indicator of future

margins, they valued land not at current purchase value but at the Potential Sales Value

(PSV – i.e. as the value when entirely developed). Furthermore, they speculatively bet

on stability of construction costs and on

ever-increasing housing demand (Lima,

2007, 2012). However, recognising that

development would take time, and that land

banks could not be directly transformed into

next year’s turnover, the stock market community shifted from gross land banks to estimates of launches such as guidance value at

one- or two-year terms. Likewise, mergers

and acquisitions were also a positive indicator later encouraged by stock markets, as

with the praises received by Gafisa’s management when they bought Tenda. In other

words, all throughout the 2005–2010 period

the focus remained on the growth of firms’

total profits, as illustrated by the fund managers’ use of EBITDA multipliers (Gregorio,

2010; Huerta and Motta, 2011; Lima, 2012).

When the promises of capital gains were not

corroborated by end-of-year financial

results, adaptations in the valuation convention (from land bank to launches and M&A)

were necessary to preserve the dominant

narrative for growth.

This was also accompanied by a shift in

power relations. As concern grew with disappointing financial results, fund managers

and analysts increasingly pressed managers

to take a series of strategic initiatives to

ensure stronger growth. Pressure was exerted

through specialists’ reports, during quarterly

Downloaded from usj.sagepub.com by guest on June 20, 2015

�15

Sanfelici and Halbert

teleconferences, and through business media

interviews. It was enacted through more benevolent pricing of shares for developers that

most eagerly complied with the proposed

managerial evolutions, whereas the shares of

more conservative firms were underpriced:

at the time of the IPOs, [.] investors wanted

everyone to spread, to diversify [investment]

across the country, to raise launching projections, and we had a more conservative profile.

We even believe our stocks have a [.] lower

valuation [than our competitors] due to our

management’s more conservative strategy.

(Interview no. 1, Investor relations manager,

Even, November 2011)

If initially housing developers and underwriters attempted to lure investors into an interpretation convention revolving around the

land bottleneck problem, the interactions

evolved with the stock market community

progressively exerting a stronger grip on

developers, disciplining them through the

use of a valuation convention focusing on

profits (Oliveira, 2008b).

Promises and numbers

By 2010–2011, with developer financial performance numbers stubbornly continuing to

diverge from the promises underlying narratives for growth, the optimistic assumptions

on which share prices had been originally

estimated were becoming increasingly discredited. Multiple reasons explain why profitability for shareholders turned out to be

weaker than expected. First, construction

costs that had been accounted at current

value by underwriters rose because of an

increase in labour costs, itself an outcome of

diminishing unemployment rates resulting

from economic growth:

firms [.] launched a lot, and because they

have a turnover of 3 years, in general they

build in the last two [.]. The problem is that,

[.] by the time firms had to build [.] in 2009,

2010, 2011, input prices were much higher,

with a labor shortage. [.] So in the projects

we sold, the margin we’d expected to be 36%

or 38%, dropped to 28%. [.] And there are

firms that had worse results [.]. Investors got

angry with firms. (Interview no. 2, Project

manager, Cyrela, March 2012)

Second, confounding business media and

analysts expectations, business strategies did

not yield improved margins as the increased

number of partners pushed coordination

costs up; economies of scale were disappointing because of the learning curve, especially

in new ‘segments’ and markets; poor execution is said to have resulted in multiple delays,

which, in turn, increased financing costs:

[firms’] focus in the first years was on scaling

up. Investors began putting a premium on [.]

rising projections of Potential Sales Value

(PSV), which indicate the potential of new

projects in terms of revenue generation. ‘Since

[the stock] market was buying launches, many

partnerships were hastily set up’, says

Christian Faricelli, equity manager at

Capitânia. According to the expert, [firms’]

aim was to diversify regionally, but they lost

control [of the operation]. ‘There was a very

fast and a bit haphazard growth by most

firms’, says Faricelli. (Tauhata, 2012)

Disappointing financial figures led to dissonant views over responsibilities. Developers

(particularly those reluctant to adopt aggressive growth strategies and those that stayed

away from the stock market) became more

vocal at denouncing the gregarious investors

and analysts that forced them to pursue misguided objectives while also being volatile in

their expectations and eager to follow ‘fads’

(Investor

Relations

manager,

Even,

November 2011). In an interview for Exame,

Cyrela’s chairman Ellie Horn was asked

how he felt about the stock market’s negative reactions to the firm’s recent report in

2009:

Downloaded from usj.sagepub.com by guest on June 20, 2015

�16

Urban Studies

[.] The first time they [analysts] talk about

your firm you follow them. Today I don’t pay

much attention, because otherwise I’d destroy

the firm. We need to look at the [stock] market’s reactions with sound judgment so that

the company is preserved. (Correa, 2009)

Some analysts, probably reflecting investors’

views, blamed instead developers on their

inability to properly execute their projects.

Thus Marcelo Motta, an analyst for JP

Morgan, declared that:

Many firms ended up focusing only on growth

and paid no attention to the matter of profitability. [.] Most of the firms [.] with falling

profits suffered due to a lack of planning.

Cost overruns, penalties incurred on projects,

allowances [for bad debts] in balance sheets

and other factors drove down profits in 2011.

(Corsini, 2012)

Other analysts struck a more balanced tone,

relating developers’ rash moves to the use of

inadequate criteria for assessing firms by

fund managers. A Banco do Brasil analyst

confided that investors had, until 2011,

failed to understand the cycles of building

and their impact on the funding needs of

firms, while acknowledging that as investors

learned how the sector works, the focus on

growth alone was gradually changing

(Corsini, 2012).

Such dissonances led to general disenchantment and to the unravelling of the prevailing convention around which these

actors had initially coalesced. This unravelling made way for new competing narratives

that progressively started to vibrate in unison again and to resonate into an interpretation convention where quality and

profitability substitutes quantity and turnover. Concomitantly, and mutually reinforcing each other, this led to an evolution in

the valuation convention as well, with fund

managers and analysts seeking different

variables to assess the value of firms:

Given the difficulties experienced by most

firms, investors and analysts shifted focus of

their demands. It is no longer expected a high

volume of launchings, but instead priority is

given to projects that are more profitable.

Positive cash flow and enhanced profitability

now dominate teleconferences. (Corsini, 2013)

Illustrative of this shift in focus, the business

press has thrown a spotlight on firms whose

strategies have been based on slower-paced

expansion through organic growth, be they

listed on the stock exchange, such as Eztec

(Barra, 2014), or not, such as CFL (Bueno,

2013).

As in the 2005–2010 period, this evolution

in stock market assessment had performative

effects upon developers. If Brookfield

bought back its shares to remove itself from

the grip of financial markets (Rostas, 2014),

other developers remained in the game by

claiming in their reports and in public

announcements to be taking strong actions

to enhance profitability. These include cutting back on new projects to better control

costs and construction schedules (Quintão,

2012); reducing the number of partnerships;

retreating from some regional markets

(Pereira, 2012); and abandoning ‘segments’

where firms had less expertise, such as

lower-income housing (Fernandes, 2012).

[the company has decided to] slow down. We

are not going to grow as much as we did [in

the past]. Our pace of growth was reduced. So

Cyrela informed the [stock] market in March

2011 that growth would not be at 30% a year,

but 10–15%. [.]. We [also] reviewed [our

plans for regional expansion]. We always

sought to expand where incomes are, in cities

with at least 500,000 inhabitants, etc. In 2008,

we had 14 partnerships. Today we have [only]

4. In 2010 and 2011 we limited [these partnerships]. When construction costs went up, we

thought: where did it happen? [It’d happened]

where we had the least control, [.] [that is]

with partners outside São Paulo, Rio, and the

South. [.] So we decided to strengthen our

Downloaded from usj.sagepub.com by guest on June 20, 2015

�17

Sanfelici and Halbert

activity where our execution is better. [.] This

all [aimed at improving] cash flow. (Interview

no. 2, Project manager, Cyrela, March 2012)

With such evolutions, a new round of spatial

consequences is likely to occur in the production of housing in Brazilian cities. As

developers seek to improve profitability,

their concentration in selected metropolitan

areas in the Southeast and South will rise,

leaving the other markets again for smaller,

family-owned firms. For the same reason,

their projects are likely to be more focused

on middle- and higher-income groups. There

are also signs that firms will concentrate

their efforts in large and very large projects

as a way of enhancing margins through scale

economies (Gazzoni, 2013) and, maybe, to

increase the profitability of their land bank.

This approach will prove sustainable as long

as the financial outputs corroborate their

strategies, or until other narratives resonate

into another convention on how best to satisfy financial markets’ pecuniary return

expectations through the production of

homes for Brazilian households.

Conclusion

Amid the multifarious factors at play in

shaping the geographies of housing, the

paper set out to take stock of the recent evolutions affecting the development industry,

especially in ‘emerging’ countries. With neoliberal reforms, alongside, and more often

than not, above the growing importance of

mortgage and of mortgage securitisation, the

provision of housing and their associated

geographies is transformed with the rising

importance of financial investors in the

development sector. This paper claims that,

in order to understand the geographies of

housing production in Brazilian cities, it is

necessary to analyse the interactions between

financial markets and development firms.

This is done by an empirical analysis of

Brazil’s housing sector between the mid

2000s and 2012.

The paper combines two strands of literature applied to the study of financial markets

(cultural economy and conventionalist economics) by developing the concept of resonance. This concept permits to recognise the

pressure exerted by financial market players,

but also the agency of development firms’

management. It also enables us to straddle

the micro- and meso-levels by dynamically

linking the interactions happening around

each individual organisation with the conventions that are made and remade on the

development industry.

This heuristic demonstrates that there is

no straightforward, unidirectional relation

leading from the expectations of financial

markets to the actually existing geographies

of housing. Instead it argues for an in-depth

analysis of the narratives co-authored by

developers and the stock market community

(investors, analysts, business media, etc.) as

well as the related strategic moves that transform the business practices of developers

and, arguably, the geographies of housing

provision. Indeed, when idiosyncratic interactions between shareholders and firm managers start vibrating in unison, interpretation

and valuation conventions contribute to converging business strategies that have consequences on the production of housing. This

is illustrated by the 2005–2010 period, in

which a dominant narrative around growth

stimulated firms to pursue more aggressive

development plans. Throughout this period,

developers prioritised large-scale projects,

targeted a wider range of income groups,

and replicated such developments across a

larger number of cities. This resulted in a

more fragmented pattern of housing production, as many such projects assumed the

form of urban enclaves.

This offers two insights into the relations

between financial markets and developers.

First, financial market conventions are not

Downloaded from usj.sagepub.com by guest on June 20, 2015

�18

Urban Studies

predetermined but vary over time in

response to observed financial results.

Disappointing numbers are accommodated

through evolutions in the dominant convention, especially as investors are discovering a

new sector, as was the case with the development industry. Yet, these adaptations occur

only up to a point: dissonant narratives may

break up the harmony, with actors blaming

each other. Second, and relatedly, power

relations between actors evolve over time. If

developers initially transformed their land

bank bottleneck into an investment opportunity, the stock market community, and in

particular fund managers, gradually tightened their grip on developers, attempting to

force them into business strategies and

rewarding – or sanctioning them – through

share pricing. Interactions are thus often

fraught with frictions, which are particularly

heated when discrepancies between the

expectations that the convention originally

embodied and the actual results arise.

Additionally, as a new convention progressively substitutes the other, the repercussions

on developers’ business strategies are likely

to once again transform the geographies of

housing.

At a more theoretical level, and without

opposing the financing of homeownership

(namely through mortgages and their securitisation) and the financing of development

activity, we have argued a need to more

directly take into account how financialisation

affects the provision of housing by developers.

This is important both in countries of the

Global South and Global North, since the

development industry entertains multiple ties

with financial markets. As we have seen in

this paper, financial markets directly provide

equity and debt to developers at corporate

level. But they are also increasingly involved

in the direct ownership of properties (see

Fields and Uffer, 2014; Guironnet et al.,

2015; Halbert et al., 2014) and in the

financing of development operations (direct

investment at project level). These evolutions

press for further analyses on the relation

between financialisation and the production

of the urban built environment from the perspective of the supply-side.

Acknowledgements

Previous versions of this paper have been presented at the LATTS seminar in Paris and at the

2015 AAG Annual Meeting in Chicago. We

would like to thank all comments made by colleagues in these occasions. We wish to thank as

well Antoine Guironnet and Félix Adisson (both

at LATTS) for their helpful comments on the latest version of the paper; three anonymous

reviewers for their constructive criticisms and

suggestions; and the Urban Studies editor for

helpful comments and suggestions.

Funding

This research was supported by grants from

Coordenacxão de Aperfeicxoamento de Pessoal de

Nı́vel Superior (grant number 99999.001546/

2014-07) and Fundac

xão de Amparo à Pesquisa

do Estado de São Paulo (grant number 2009/

14613-9).

Notes

1. Policymakers involved in the approval of the

SFI law, and the financial institutions that

lobbied them, took inspiration from other

countries, including the USA. Yet mortgagebacked securities (MBS), often issued by

developers themselves, were used to support

the buy-and-hold strategies of banks which

are required by the Housing Finance System

(HFS) to channel at least 65% of their balances to mortgage finance (Royer, 2009). This

consequently reduced both the size and the

liquidity of MBS available for financial investors, thus strongly limiting the extent of the

financialisation of homeownership in Brazil

through the securitisation of mortgages.

2. Novo Mercado is a listing segment that

requests more corporate governance and

Downloaded from usj.sagepub.com by guest on June 20, 2015

�19

Sanfelici and Halbert

transparency requirements than is required

by Brazil’s legislation.

3. These are marketed as ‘planned neighbourhoods’ and their full development often takes

5 to 10 years (Gazzoni, 2013).

4. The extent to which cities operate as platforms for further expansion varies according

to firm strategies and to the region’s average

income. The North and Northeast, where

average incomes are much lower than in the

South and Southeast, saw developers focus

on the metropolitan areas.

References

Aalbers MB (ed.) (2012) Subprime Cities and the

Twin Crises. London: Wiley & Blackwell.

Aalbers MB and Christophers B (2014) Centring

housing in political economy. Housing, Theory

and Society 31(4): 373–394

Amato FB (2008) Private equity e a consolidacxão

do mercado. Construc

xão Mercado, June.

Aranha C (2011) Um degrau de cada vez na Even.

Revista Exame, 11 December.

Arretche M (1990) Intervencxão do Estado e setor

privado: O modelo brasileiro de polı́tica habitacional. Espac

xo e debates 31: 21–36.

Ashton P (2009) An appetite for yield: The anatomy of the subprime mortgage crisis. Environment and Planning A 41(6): 1420.

Azevedo S (1996) A crise da polı́tica habitacional:

Dilemas e perspectivas para o final dos anos

90. In: Ribeiro LCQ (ed.) A crise da moradia

nas grandes cidades: Da questão da habitac

xão á

reforma urbana. Rio de Janeiro: Editora

UFRJ, pp. 73–104.

Ball M (1983) Housing Policy and Economic

Power: The Political Economy of Owner Occupation. London: Routledge.

Barra P (2014) Por que a melhor construtora

pode dobrar de valor nos próximos anos? Infomoney, 17 December.

Blanco M (2008) Entrevista com José Antonio

Garbowsky. Construc

xão Mercado, April.

Bueno S (2013) CFL cresce com operacxão regionalizada. Valor Econômico, 1 July.

Canc

xado P (2010) PDG compra a Agre. O Estado

de S. Paulo, 4 May.

Carruthers BG and Stinchcombe AL (1999) The

social structure of liquidity: Flexibility,

markets, and states. Theory and Society 28(3):

353–382.

Castro CMP (1999) A explosão do autofinanciamento na producxão da moradia em São Paulo

nos anos 1990. São Paulo: FAU/USP, 1999

(unpublished PhD dissertation).

Cichinelli G (2008a) Efeitos do boom: Consolidac

xão do setor. Construc

xão Mercado, August.

Cichinelli G (2008b) Efeitos do boom – Crescimento urbano desordenado. Construc

xão Mercado, August.

Correa C (2009) Sobreviva – E ganhe depois, diz

Elie Horn. Revista Exame, 19 March.

Corsini R (2012) O tombo das grandes. Construc

xão Mercado, May.

Corsini R (2013) A origem dos prejuı́zos. Construc

xão Mercado, May.

David L (2013) La production urbaine de Mexico:

Entre financiarisation et construction territoriale. Université Paris-Est (unpublished PhD

thesis).

David L and Halbert L (2014a) Constructing

‘world-class’ cities. Dialogues in Urban and

Regional Planning 5: 99–114.

David L and Halbert L (2014b) Finance capital,

actor-network theory and the struggle over

calculative agencies in the business property

markets of Mexico City Metropolitan Region.

Regional Studies 48(3): 516–529.

Fainstein S (1994) The City Builders: Property,

Politics and Planning in London and New York.

Lawrence, KS: University Press of Kansas.

Farah MFS (1985) Estado e Habitac

xão no Brasil:

O caso dos Institutos de Previdência. Espac

xo &

Debates, São Paulo 16: 73–81.

Fernandes A (2012) Construtoras mudam estratégia de expansão geográfica e por renda. Valor

Econômico, 21 September.

Ferreira JSW (ed.) (2012) Produzir casas ou construir cidades? Desafios para um novo Brasil

urbano. São Paulo: LABHAB.

Fields D and Uffer S (2014) The financialisation

of rental housing: A comparative analysis of

New York City and Berlin. Urban Studies.

DOI: 10.1177/0042098014543704.

Fix M (2011) Financeirizac

xão e transformac

xões

recentes no circuito imobiliário no Brasil. Campinas: Instituto de Economia/Unicamp

(unpublished PhD Dissertation).

Downloaded from usj.sagepub.com by guest on June 20, 2015

�20

Urban Studies

Forrest R (2015) The ongoing financialisation of

home ownership – New times, new contexts. International Journal of Housing Policy 15(1): 1–5.

Froud J, Johal S, Leaver A, et al. (2006) Financialization and Strategy: Narrative and Numbers.

London: Routledge.

Gazzoni M (2013) Construtoras buscam nova

fonte de receita com os bairros planejados. O

Estado de S. Paulo, 13 February.

Gregorio CAG (2010) Entenda como os precxos

das ac

xões das incorporadoras inflaram artificialmente. Construc

xão Mercado, March.

Guironnet A, Attuyer K and Halbert L (2015)

Building cities on financial assets: The financialisation of property markets and its implications for city governments in the Paris cityregion. Urban Studies. DOI: 10.1177/004209

8015576474.

Halbert L and Rouanet H (2014). Filtering risk

away: Global finance capital, transcalar territorial networks and the (un) making of cityregions: An analysis of business property development in Bangalore, India. Regional Studies

48(3): 471–484.

Halbert L, Henneberry J and Mouzakis F (2014)

The financialization of business property and

what it means for cities and regions. Regional

Studies 48(3): 547–550.

Harvey D (2003) Paris, Capital of Modernity.

Abingdon: Routledge.

Huerta AE and Motta M (2011) Brazilian Homebuiders 101. São Paulo: JP Morgan, Latin

American Equity Research.

Klink J and Denaldi R (2014) On financialization

and state spatial fixes in Brazil. A geographical and historical interpretation of the housing

program My House My Life. Habitat International 44: 220–226.

Langley P (2007) Uncertain subjects of AngloAmerican financialization. Cultural Critique

65(1): 67–91.

Lavigne S (2002) Investisseurs financiers et convention d’évaluation des firmes: Une mode´lisation

de la diffusion institutionnelle de la convention.

Université Toulouse 1 (unpublished PhD

dissertation).

Lima JR Jr (2007) Landbank das empresas listadas

na Bovespa. Construc

xão Mercado, November.

Lima JR Jr (2012) Era possı́vel prever? Construc

xão Mercado, June.

Lindemann G (2008) Construtoras contratam

consultoria para atrair engenheiros para cargos

executivos. Construc

xão Mercado, 15 August.

Lorrain D (2009) Because the market says so:

Brokers and managers in the electricity industry. Sociologie du travail 51: e49–e66.

Mandl R (2006) Megainvestidor paga R$ 135 milhões por 32% da Gafisa. UOL Economia, 10

June.

Maricato E (1987) Polı´tica habitacional no regime

militar: Do milagre brasileiro à crise economica.

Petrópolis: Ed. Vozes.

Maricato E (2011) O impasse da polı´tica urbana

no Brasil. Petrópolis: Ed. Vozes.

Oliveira T (2008a) Efeitos do boom: Transparência na gestão. Construc

xão Mercado, August.

Oliveira T (2008b) Mercado de capitais. Construc

xão Mercado, December.

Olivion B (2010) Construtoras correm atrás da

baixa renda. Revista Exame, 10 April.

Orléan A (1999) Le pouvoir de la finance. Paris:

Odile Jacob.

Orléan A (2004) L’économie des conventions:

Définitions et résultats. In: Orléan A (ed.) Analyse économique des conventions. Paris: Presses

Universitaires de France, Coll. Quadrige, pp.

9–48.

Paulani L (2008) Brasil Delivery: A polı´tica econômica do governo Lula. São Paulo: Boitempo.

Pereira V (2012) Avessas a IPOs, construtoras

menores focam em nichos para crescer. 26

June. Brasil: Reuters.

Poon M (2009) From new deal institutions to capital markets: Commercial consumer risk scores

and the making of subprime mortgage finance.

Accounting, Organizations and Society 34(5):

654–674.

Pryke M and Du Gay P (2007) Take an issue:

Cultural economy and finance. Economy and

Society 36(3): 339–354.

Quintão C (2012) Incorporadoras estimam crescer

menos em 2012. Valor Econômico, 25 January.

Ribeiro LCQ (1996) Dos cortic

xos aos condomı´nios

fechados: As formas de produc

xão da moradia na

cidade do Rio de Janeiro. Rio de Janeiro: Editora Record.

Rolnik R (2013) Late neoliberalism: The financialization of homeownership and housing rights.

International Journal of Urban and Regional

Research 37(3): 1058–1066.

Downloaded from usj.sagepub.com by guest on June 20, 2015

�21

Sanfelici and Halbert

Rostas R (2014) Ac

xão da Brookfield sobe 19%

após confirmar oferta para fechar capital.

Valor Econômico, 17 February.

Rouanet H and Halbert L (2015) Leveraging

finance capital: Urban change and self

empowerment of real estate developers in

India. Urban Studies. DOI: 10.1177/0042098

015585917.

Royer LDO (2009) Financeirizacxão da polı´tica

habitacional: limites e perspectivas. São Paulo:

FFLCH/USP (Phd dissertation).

Rufino MBC (2012) Incorporac

xão da metrópole:

centralizacxão do capital no imobiliário e nova lógica

de produc

xão do espacxo de Fortaleza. São Paulo:

FAU/USP (unpublished Phd dissertation).

Rutland T (2010) The financialization of urban

redevelopment. Geography Compass 4(8):

1167–1178.

Sanfelici D (2013) Financeirizacxão e a produc

xão

do espac

xo urbano no Brasil: Uma contribuic

xão

ao debate. EURE (Santiago) 39(118): 27–46.

Schwartz H and Seabrooke L (2008) Varieties of

residential capitalism in the international political economy: Old welfare states and the new

politics of housing. Comparative European Politics 6(3): 237–261.

Searle LG (2014) Conflict and commensuration:

Contested market making in India’s private

real estate development sector. International

Journal of Urban and Regional Research 38(1):

60–78.

Shimbo LZ (2012) Habitac

xão social de mercado: A

conflueˆncia entre Estado, empresas construtoras

e capital financeiro. Belo Horizonte: C/Arte.

Sigolo L (2014) O boom imobiliário na metrópole

paulistana: O avanc

xo do mercado formal sobre

a periferia e a nova cartografia da segregac

xão

socioespacial. São Paulo, FAU/USP (unpublished PhD dissertation).

Tadjeddine Y (2006) Les gérants d’actifs en

action: L’importance des constructions

sociales dans la décision financière. In:

Eymard-Duvernay F (ed.) L’e´conomie des conventions, me´thodes et re´sultats (Tome 2). Paris:

La Découverte, pp. 193–207.

Tauhata S (2012) Rachaduras no concreto. Valor

Econômico, 11 September.

Theurillat T and Crevoisier O (2014) Sustainability and the anchoring of capital: Negotiations

surrounding two major urban projects in Switzerland. Regional Studies 48(3): 501–515.

Valenc

xa MM (1999) The closure of the Brazilian

Housing Bank and beyond. Urban Studies

36(10): 1747–1768.

Valenc

xa MM and Bonates MF (2010) The trajectory of social housing policy in Brazil: From

the National Housing Bank to the Ministry of

the Cities. Habitat International 34(2): 165–173.