Optimal Reserve Prices in Upstream Auctions: Empirical

Application on Online Video Advertising

Miguel Angel Alcobendas

Sheide Chammas

Yahoo! Inc.

Yahoo! Inc.

lisbona@yahoo-inc.com

chammas@yahooinc.com

ABSTRACT

We consider optimal reserve prices in BrightRoll Video Exchange when the inventory opportunity comes from other

exchanges (downstream marketplaces). We show that the

existence of downstream auctions impacts the optimal floor.

Moreover, it renders the classical derivation of the floor

set by a monopolist inadequate and suboptimal. We derive the new downstream-corrected reserve price and compare its performance with respect to existing floors and the

classical optimal monopoly price. In our application, the

downstream-corrected reserve price proves superior to both.

The proposed model also deals with data challenges commonly faced by exchanges: limited number of logged bids in

an auction, and uncertainty regarding the bidding behavior

in other exchanges.

The relevance of this study transcends its particular context and is applicable to a wide range of scenarios where

sequential auctions exist, and where marketplaces interact

with each other.

1. INTRODUCTION

The importance of video advertising is growing. According to a PWC report 2015 [1], online video advertising revenue exhibits the fastest growth in internet advertising: rising from $6.32bn in 2014 to a forecasted revenue of $15.39bn

in 2019.

Using data from BrightRoll Video Exchange, we estimate

and test a structural model to compute optimal reserve prices.

A reserve price corresponds to the lowest bid that the seller

is willing to accept for his item. The novelty of this work

is that we set the optimal reserve price in a marketplace

(upstream) taking into account that, in order to deliver the

video advertisement, the winner of the exchange competes

against bidders in a second exchange, called downstream

marketplace. The use of several exchanges may help publishers to increase demand and competition for the inventory

opportunity, since different marketplaces may have different

demand partners. As the reader may anticipate, the inforPermission to make digital or hard copies of all or part of this work for personal or

classroom use is granted without fee provided that copies are not made or distributed

for profit or commercial advantage and that copies bear this notice and the full citation on the first page. Copyrights for components of this work owned by others than

ACM must be honored. Abstracting with credit is permitted. To copy otherwise, or republish, to post on servers or to redistribute to lists, requires prior specific permission

and/or a fee. Request permissions from permissions@acm.org.

KDD ’16, August 13-17, 2016, San Francisco, CA, USA

c 2016 ACM. ISBN 978-1-4503-4232-2/16/08. . . $15.00

DOI: http://dx.doi.org/10.1145/2939672.2939877

Kuang-chih Lee

Yahoo! Inc.

kclee@yahoo-inc.com

mation that an exchange has regarding other marketplaces

is limited. Our model accounts for that, as well as, partial

knowledge of bids submitted in the own exchange.

In this paper, we derive the reserve price, also called floor,

that BrightRoll Video Exchange should charge in order to

maximize its expected profits considering the existence of a

downstream auction. In our analysis, we will assume that

Brightroll conducts a second price auction and the downstream exchange uses a first price auction to allocate impressions.

From an exchange perspective, video advertising is not

very different from allocating static display advertising: the

publisher has an inventory opportunity that wants to monetize using an auction conducted by a marketplace. The

main difference between the classic banner and video ads is

the format: we may have a video ad playing before (pre-roll),

during (mid-roll), or after (post-roll) the streaming content.

The format affects the bidder’s valuation of the opportunity.

In the presence of downstream auctions, the publisher

sends an ad-request to a marketplace (downstream). Then,

the exchange will send a bid request to several real time

bidders (RTB), that may be, for instance, demand aggregators (DSP), advertisers, or other marketplaces (upstream).

The upstream marketplace will also auction the opportunity.

The winner of the latter exchange will then compete against

bids submitted downstream. Finally, the downstream winner will be the one delivering the advertisement.

We are not aware of any study quantifying the importance

of downstream auctions. However, at BrigthRoll a significant amount of inventory opportunities comes from other

exchanges. Given the relevant role of the company on video

advertising, we believe that their implications deserve to be

studied.

We show that, for a given inventory opportunity, the optimal upstream exchange floor is greater than the monopoly

reserve price developed by Myerson [8] and Riley and Samuelson [10]. The result is very intuitive: the existence of a downstream exchange makes harder to deliver the video ad, since

the upstream winner has to compete against downstream

bidders.

We use auction theory and statistical tools to overcome

data limitations. In particular, we only have information

about auctions with bids above the current reserve price,

which leads to a left-censored data problem. Moreover, conditional on auctions with bids above the floor, we only know

the identity of the winning bidder, its bid, the second highest

bid, and the current floor. We do not either have data about

auctions conducted downstream, except a dummy variable

�indicating that the upstream winner also won the downstream auction and delivered the video ad.

Due to the large amount of data and expensive computations, we decided to implement the algorithm using Apache

Spark, a general-purpose cluster computing system designed

to deal with this type of tasks.

We measure the impact of the aforementioned classical

optimal floors on inventory with and without a downstream

exchange. Then, we use experiment data to derive the expected performance of optimal floors with the downstream

correction.

Our test shows that implementing the classical monopoly

reserve price without a correction increases the overall generated revenue on inventory with and without a downstream

auction. In the particular case of inventory with BrightRoll

Video Exchange as a unique marketplace, the expected revenue lift equals 39%, with a observed revenue increase in 77%

of the different types of inventory, also called placements. If

we look at the effects of the classical optimal floor set by

a monopolist on inventory with downstream auctions, results are mixed: while the overall expected revenue lift with

respect to current floors equals 25%, our recommendations

only increased revenue in 67% of the analyzed placements.

Results improve when we use floors that account for the

existence of downstream auctions. In such a case, the expected revenue lift equals 29% and revenue increased in 77%

of placements, outperforming the results from the classical

optimal monopoly floor.

As expected, our recommendations work better when we

set floors above the current ones. As previously mentioned,

data is left-censored. As a result, we have to infer the distribution of bidders’ valuation using data that is only observed

when bids are above current floors.

The rest of the paper is organized as follows. Section 2

reviews previous work. Section 3 introduces general aspects

of the type of problems that we are trying to solve. Section

4 presents the model and optimality conditions for the reserve price. Section 5 outlines the estimation methodology.

Section 6 describes the data and estimate results. Section 7

presents the experiment results. Finally, section 8 concludes.

2. RELATED WORK

Reserve prices have been largely studied in auction theory. However, empirical literature is scarce. One of the

rare studies was conducted by Ostrovsky and Schwarz [4].

Their paper is one of the first large scale experiments measuring the impact of setting reserve prices for online advertisement. They combine previous work in auction theory

by Myerson [8], Riley and Samuelson [10] and Varian [12]

to derive optimal floors for sponsored search. Their experiment shows that revenue substantially increases as a result

of implementing optimal reserve prices. While they have

full information about advertisers bids, we have to face the

problem of limited data and sequential auctions.

Yuan et al. [13] empirically test several algorithms to set

reserve prices. They propose a real-time control function

approach to correct reserve prices by using the highest bid.

They also test the classical derivation of the optimal monopoly

price based on the aforementioned work by Myerson [8] and

Riley and Samuelson [10], and two other algorithms based

on the regression of the two highest bids. Based on results

from their experiment, the proposed control function approach works better than the optimal monopoly floor ap-

proach. Due to system requirements, we are not allowed

to change the reserve price at impression level, preventing

us to test the Yuan et al. [13] approach. In any case, we

are concerned about the longterm effects of their proposed

algorithm. Having a reserve price that directly depends on

the highest bid may give bidders incentives to shade their

bids as in first price auctions (see V. Krishna [6]). Authors

are aware of this possibility, but due to confounding factors

(e.g. holidays at the beginning of the experiment, bidders

being not aware of the experiment, ...) they could not show

that bidding behavior were not affected by the algorithm.

We could neither use the regression based models since we

do not observe auction data when the highest bid is below

the reserve price.

From a theoretical perspective, our paper is related to sequential auctions and auctions with intermediaries. The existing theoretical work assumes that the distribution of the

bidders’ valuation and the number of competitors is known

at each round of auctions. This is not our case since we do

not have much information about what is happening downstream. For instance, McAfee and Vincent [7] derive optimal

floors when the auctioneer is able to resell the object in a new

auction round if bids are lower than the set floors. Other

theoretical studies like Feldman, et al. [5], and Stavrogiannis et al. [11] characterize the equilibrium behavior of the

players in an auction with intermediaries. In their models,

there exists an exchange (downstream) that sends the bid request to other upstream exchanges (intermediaries). Given

a predefined auction mechanism, Feldman et al. [5] focus

on the derivation of the profit maximizing reserve price set

by the downstream and upstream exchanges, and the optimal fee charged by the intermediary. On the other hand,

Stavrogiannis, et al. [11] study the optimal reserve price set

by the downstream exchange and the intermediary profits

depending on the auction design.

3. BACKGROUND

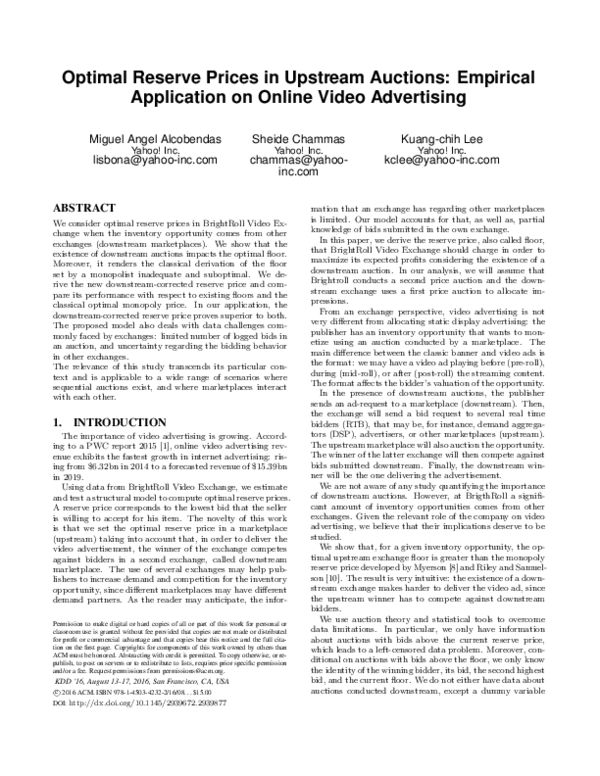

Figure 1 displays the analyzed business model. When a

publisher has an inventory opportunity, it sends an advertisement request to a marketplace denoted as Downstream

M arketplace, which conducts an auction to allocate the opportunity. Then, the downstream marketplace will send a

bid request to several real time bidders (RTB), that may

be demand aggregators (DSP), advertisers, or other marketplaces. In Figure 1, we have two real time bidders: dsp1

and an exchange denoted as U pstream M arketplace. Similarly, the upstream marketplace will also conduct an auction

to determine the winner and the bid passed to the downstream exchange. In our application the upstream exchange

corresponds to BrightRoll Video Exchange.

The upstream marketplace is assumed to conduct a second price auction, and the downstream exchange uses a first

price auction mechanism to allocate impressions. Both exchanges are able to set reserve prices in order to maximize

their expected revenue. In this paper, we focus on the optimal floors set by the upstream exchange.

Only if the advertisement is delivered, the winner of the

downstream marketplace pays the transaction price, and the

exchange and publisher split the generated revenue. As we

will see later, the optimality condition to set the upstream

reserve price does not depend on fees charged by exchanges.

For that reason, we will assume that the downstream marketplace does not charge any fee for conducting the auction.

�Publisher

Inventory

Opportunity

{dsp3,$6}

Downstream

MarketPlace

{dsp3,$6} = {dsp3,$8*(1-0.25)}

{dsp1,$5}

Upstream

MarketPlace

dsp1

{dsp2,$8}

{dsp3,$9}

dsp3

dsp2

Floor = $4.7

Revenue Share = 25%

{dsp4,$4}

dsp4

Figure 1: Marketplace Design

for a particular inventory opportunity. For each risk neutral bidder i, the valuation of the inventory opportunity,

denoted as vi , is assumed to be an independent and identically distributed realization of the random variable V over

the interval [0, v̄], which has a cumulative distribution function FV (v) and probability density function fV (v). While

the value of the inventory for each potential buyer is private

information, the distributions FV (v) and fV (v) are publicly

known by participants. For simplicity, we also assume that

bidders are not able to switch between marketplaces.

In second price auctions with reserve prices, it is a weakly

dominant strategy for bidders to bid their own value. The

existence of a downstream first-price auction does not change

the bidding strategy of participants in the upstream exchange. As a result, truth-telling continues being a dominant strategy. That is,

bi = vi for r ≤ vi

This is the case where publishers manage the allocation of

their inventory using their own marketplace (e.g. Yahoo!,

Facebook,...). On the other hand, the upstream marketplace

will keep a percentage of the clearing price of the winning

bid. As we will explain in detail later on, to ensure that the

upstream exchange gets paid, it will keep the corresponding

fee before passing the bid to the downstream auction.

As an illustration, imagine the scenario depicted in Figure 1. The publisher has an inventory opportunity and sends

an ad request to the downstream marketplace. The exchange will send a bid request to the upstream marketplace

and dsp1. Then, the upstream marketplace will ask DSPs 2,

3 and 4 to submit a bid for the inventory opportunity. Assume that dsp2 submits a bid that equals 8 dollars eCPM,

dsp3 bids 9, and dsp4 bids 4. Only bids above the floor are

considered. In this example, the upstream floor is set to $4.7.

As a result, the bid submitted by dsp4 is discarded. Among

the remaining bids, the winner of the upstream marketplace

is dsp3. Since the exchange employs a second price auction

mechanism, we use the bid submitted by dsp2, the set floor

and the revenue kept by the marketplace to compute the

bid passed to the downstream marketplace. The upstream

transition price equals $8 and corresponds to the maximum

of dsp2 and the floor set at $4.7. Assume that the upstream

exchange keeps 25% of the transaction price if bidder dsp3 is

able to deliver the advertisement. Given the revenue share,

the bid submitted to the downstream marketplace equals

$6, which is the result of subtracting 25% from the dsp2 bid

(i.e. 6 = 8 ∗ (1 − 0.25)). Consequently, the potential revenue

for the upstream marketplace is $2 eCPM. The bid passed

to the downstream auction, the tuple {dsp3, $6}, competes

with dsp1. Assume that the downstream marketplace sets

a floor that is equal to zero and runs a first price auction.

Given the auction design and bid submitted by dsp1, dsp3

wins the auction and pays $8. The publisher will keep $6

and the remaining $2 corresponds to the fees charged by the

upstream exchange.

4. MODEL

In this section we develop the model to estimate the optimal floor that the upstream marketplace should set in order

to maximize its expected revenues taking into account the

existence of a downstream exchange. In the upstream marketplace, we assume that there exist N potential bidders

where bi corresponds to the bid made by i, vi equals the

aforementioned valuation of the inventory, and r denotes

the reserve price.

The proof is very intuitive. Assume that in the upstream

marketplace a potential buyer i bids less than his valuation

vi . Given such a choice, the bidder would risk losing the

inventory opportunity to another interested buyer who bids

higher than him, but who has lower valuation. Note that

the price paid by the winner is not determined by its own

bid but the bid of the nearest opponent. So bidding below

vi is not optimal in the upstream auction. This result is

reinforced by the existence of a downstream exchange, since

bidding below bidder’s valuation increases the probability

that a downstream bidder, who values the inventory less

than vi , bids slightly higher than the upstream potential

buyer. On the other hand, bidding more than bidder’s own

valuation increases the chances of winning the upstream and

downstream auctions. However, using a similar argument,

if the upstream bidder i bids more than vi , he may pay

more than the inventory opportunity is worth to him. Since

we have ruled out bids both above and below vi , the only

option is to bid his own valuation vi . In the presence of a

downstream auction, there is no benefit from deviating from

truth-telling.

Given the ordered bidder’s valuations in the upstream

auction v1 > v2 > · · · > vN and knowing that truth-telling

is an equilibrium, the bidder with highest valuation v1 wins

the upstream auction, and pays, conditional on winning the

downstream auction, the maximum between what his nearest opponent is willing to pay v2 and the reserve price r.

That is bidder 1 pays

w = max{v2 , r}

Note that the actual payment is only made if the winner of

the upstream auction delivers the advertisement.

In order to derive the reserve price, we extend the general formulation proposed by Riley and Samuelson [10] by

capturing the effects of introducing a downstream auction.

We will follow a similar approach to derive the optimality

condition for the reserve price.

Since bidders are assumed to be symmetric, we just need

to study one buyer (bidder i) to derive his expected payment and the expected revenue of the exchange. Bidder i’s

expected profit from participating in the upstream market-

�Given the upstream marketplace expected profits, in order to find the optimality condition for r to be optimal, we

compute the derivative of Πups with respect to r. That is,

place equals

Π(x, vi ) = vi FV (x)N −1 PD (w̄T (r)) − S(x)

where vi is the value of the inventory opportunity for bidder

i, x corresponds to bidder i’s bid, and FV (x)N −1 is the probability that bidder i wins the upstream auction (i.e. everybody else bids less than bidder i). PD (w̄T (r)) corresponds

to the probability of winning the downstream auction. It depends on w̄T (·) that equals the expected transaction price

conditional on having at least one bidder above the reserve

price r. As we will discuss in detail later on, w̄T (·) does

not directly depend on the reported value but on the known

distributions fV and FV . This simplifies the optimization

problem. Finally, S(x) is the expected payment given bid x.

Since truth-telling is a dominant strategy. The following

first-order condition must be satisfied if the bidder wants to

maximize his expected gain,

i

∂Π(x, vi )

d h

FV (x)N −1 PD (w̄T (r)) − S ′ (x) = 0 (1)

= vi

∂x

dx

at x = vi .

If the bidder has a valuation equal to the reserve price r,

he expects to pay

S(r) = rFV (r)N −1 PD (w̄T (r))

(2)

Given conditions 1 and 2, bidder i’s expected payment is

Z vi

S ′ (u)du

S(vi ) = rFV (r)N −1 PD (w̄T (r)) +

r

Z vi

i

d h

= rFV (r)N −1 PD (w̄T (r))+ u

FV (u)N −1 PD (w̄T (r)) du

du

r

This expression can be further simplified by integrating by

parts as follows,

N −1

S(vi ) = vi FV (vi )

PD (w̄T (r))

Z vi

N −1

FV (u)

PD (w̄T (r))du

−

r

Given bidder i’s expected payment and assuming that

there exist N symmetric bidders, we can derive the expected revenue of the upstream exchange and the floor that

it should charge in order to maximize its profits. The upstream marketplace expects to receive a percentage of what

bidders expect to pay. This revenue share is denoted as rev

and treated as given. Since there are N symmetric bidders, the expected revenue of the upstream exchange (Πups )

equals N times the revenue share times the expected payment of each potential buyer (S(·)). That is,

Z v̄

S(u)fV (u)du

(3)

Πups = rev N

r

Z v̄ h

uFV (u)N −1 PD (w̄(r))

= rev N

r

�

Z u

N −1

FV (µ)

PD (w̄T (r))dµ fV (u)du

−

r

Note that in 3 we compute the expected value of S(·) because the exchange does not know how much each potential

buyer values the inventory. It only has information about

the distribution of bidders’ valuation.

Integrating expression 3 by parts,

Z v̄

Πups= rev N PD (w̄T (r)) [uf (u) − 1 + FV (u)] FV (u)N −1 du (4)

r

∂Πups

=0

∂r

(5)

Using equations 4 and 5, the optimality condition is characterized by

[rfV (r) − 1 + FV (r)] FV (r)N −1 PD (r) =

(6)

Z

∂PD (w̄T (r)) v̄

[uf (u) − 1 + F (u)] FV (u)N −1 du

∂r

r

where the probability of winning in the downstream exchange is assumed to be increasing in r on the support

interval [0, v̄]. Using the chain rule, the derivative of the

probability of winning the downstream auction with respect

to the reserve price equals

∂PD (w̄T ) ∂ w̄T (r)

∂PD (w̄T (r))

=

≥0

∂r

∂ w̄T

∂r

(7)

Looking at equation 7, assuming that PD (w̄T (r)) is increasing in r is equivalent to assume that PD (w̄T (r)) is increasing

in w̄T , since by definition w̄T increases with r.

The reserve price that follows from equation 6 leads to the

optimal reserve price and it is denoted as ρ∗c .

The following proposition summarizes previous results.

Proposition 1: Under the assumptions that bidders’ valuation of the inventory opportunity is an i.i.d. realization of

the random variable V , and bidders are risk neutral, the reserve price that maximizes the upstream exchange expected

revenue ρ∗c satisfies

[ρ∗c fV (ρ∗c ) − 1 + FV (ρ∗c )] FV (ρ∗c )N −1 PD (ρ∗c ) =

(8)

Z v̄

∗

∂PD (w̄T (ρc ))

[ufV (u) − 1 + F (u)] FV (u)N −1 du

∂ρ∗c

ρ∗

c

Note that without downstream auctions, the optimality condition for the monopoly reserve price equals (see Riley and

Samuelson [10])

[ρ∗u fV (ρ∗u ) − 1 + FV (ρ∗u )] = 0

(9)

where ρ∗u corresponds to the optimal reserve price without

downstream correction. Note that, contrary to expression 9,

equation 8 depends on the number of competitors and probability of winning the downstream auction. On the other

hand, the revenue share kept by the upstream exchange

(rev) does not have any impact on the optimal reserve price.

Proposition 2: Under the assumptions that bidders’ valuation of the inventory opportunity is an i.i.d. realization

of the random variable V , bidders are risk neutral, and the

probability of winning the downstream auction is increasing

in the reserve price, the reserve price that maximizes the

upstream exchange expected revenue ρ∗c is greater than the

uncorrected optimal floor ρ∗u .

The proof is straightforward. Under the stablished assumptions, the payment of upstream bidders is increasing

in r, and the optimal reserve price that maximizes the upstream expected revenue in the presence of a downstream

exchange is ρ∗c . As a result, using ρ∗u in equation 6 is not optimal, lowering the expected revenue. Proposition 2 states

�that, for a given inventory, the corrected optimal floor (ρ∗c ) is

greater than the uncorrected one (ρ∗u ). This result is very intuitive: the existence of a downstream auction makes harder

to show an impression since the winner of the upstream marketplace has to compete against downstream bidders. As

a result, the upstream floor is increasing with downstream

competition. That explains why ρ∗c is greater than a reserve

price that does not account for the existence of downstream

exchanges (ρ∗u ).

As we will discuss in detail later on, we will analyze the

impact of ρ∗c and ρ∗u using data from BrightRoll Video Exchange.

The last part of this section is devoted to further develop

the term w̄T , that corresponds to the expected transaction

price conditional on having, at least, one bidder above the

reserve price.

By definition, w̄T equals

Z v̄

(10)

ufWT (u, r)du

w̄T (r) = rPWT (w = r) +

r

where the first component on the right hand side is the expected payment when there is a single bidder above the reserve price, and the second term equals the expected payment when two or more bids are above the reserve price r.

PWT (w = r) corresponds to the probability that the transaction price w is equal to the reserve price r, and fWT (u, r) is

the probability distribution function of the transaction price

when there exist more than one bid above the reserve price.

Both probabilities are conditional on having, at least, one

bid above r. That is, the conditional probability for w = r

corresponds to

�

�

N FV (r)N −1 [1 − FV (r)]

PWT (w = r) =

1 − FV (r)N

where the numerator indicates the probability that there is

a single bid above the reserve price, and the denominator

equals the probability that someone bids above the reserve

price.

As previously discussed, for a particular auction we do

not observe all bids. We only have information regarding

the highest and the second highest bid as long as they are

above the reserve price. As a result, we will use the density

function of the second highest bid to compute fWT . That is,

the density function of the transaction price conditional on

having two or more bidders above the reserve price equals

�

�

N (N − 1)FV (u)N −2 [1 − FV (u)]fV (u)

fWT (u, r) =

(11)

1 − FV (r)N

The numerator in 11 corresponds to the density function

of the transaction price w when it is equal to the second

highest bid. Consequently, it follows the distribution of the

second-highest-order statistic from an i.i.d. sample of size

N and distribution fV (see Arnold, Balakrishnan, and Nagaraja (1992) [3]). Once again, the denominator equals the

probability that there exists at least one bid above the reserve price.

After some algebra, it is easy to show that the corresponding derivative with respect to the reserve price equals

Z v̄

∂ w̄T (r)

∂

∂

ufWT (u, r)du

=

rPWT (w = r) +

∂r

∂r

∂r r

Z v̄

∂fWT (u, r)

∂PWT (w = r)

+ u

du

= PWT (w = r) + r

∂r

∂r

r

This derivative will be used to compute the optimal reserve

price (ρ∗c ) in equation 8.

In the next section we discuss how to implement the previous results to get the optimal floor using data from BrightRoll

Video Exchange.

5. ESTIMATION

In order to compute the optimal floor in equation 8 we

need the distribution of bidders’ valuation of the inventory

opportunity (fV , FV ), and the expected probability of winning the downstream auction (PD ). This section outlines

the procedure to estimate the aforementioned distributions.

The BrightRoll Video Exchange data set only contains

information about auctions with the highest bid above the

reserve price. Consequently, we do not have data about upstream auctions where all bids are below the set floor. The

data set includes details about the type of inventory (also

called placement), the identity and the bid of the winner in

the upstream auction, the transaction price (w) and the current reserve price (r). Regarding downstream marketplaces,

we only know which upstream auctions led to an impression

in the downstream exchange.

Our algorithm takes into account the available information in order to compute the optimal reserve price in the upstream auction when inventory comes from other exchanges.

We use a two-step approach to estimate the floor price:

firstly, we characterize the distribution of the buyers’ valuation of the inventory (fV and FV ), and estimate the parameters capturing the relationship between the probability

of wining downstream and the expected transaction price.

In step two, we will use the estimates and expression 8 to

compute the optimal reserve price.

In step 1, we follow Paarsch and Hong [9] and estimate

the parameters of the model using the likelihood function of

the transaction price (w). As previously stated, given the

ordered bidder’s valuations in the upstream auction v1 >

v2 > · · · > vN , w equals

w = max{v2 , r}

Once again, the actual payment is only made if the winner

of the upstream auction delivers the advertisement.

When the upstream exchange conducts an auction we may

have three possible scenarios: one where all bids are below

the reserve price, the case where only one bidder is willing

to pay more than the reserve price, and the outcome where

two or more bidders submit a bid above the floor. We will

combine the probability of each event to construct the probability density function of the transaction price w.

The probability that all bidders bid below the reserve price

equals

P r(w = 0) = FV (r; θ)N

where θ corresponds to the vector of parameters defining the

shape and scale of the parametric distribution of the bidders’

value of the inventory.

When only one potential buyer bids above the reserve

price and the rest N − 1 bidders have valuations below it,

the probability is equal to

P r(w = r) = N FV (r; θ)N −1 [1 − FV (r; θ)]

Finally, the corresponding probability density when two

or more bidders value the inventory more than the reserve

�Given the probability density function defined in 13, we

can construct the likelihood function as follows

L=

Q

Y

fW (wt ; θ|zt )

(14)

q=1

Figure 2: Truncated Probability Distribution of W

price is

fˆW (w, n > 2; θ) = N (N − 1)FV (w; θ)N −2

fV (v; θ) = exp(θ1 )θ2 v θ2 −1 exp(−exp(θ1 )v θ2 )

×[1 − FV (w; θ)]fV (w; θ)

where n is the number of bids above the reserve price. This

expression corresponds to the distribution of the transaction

price when it is equal to the second highest bid, and it follows

the distribution of the second-highest-order statistic from

an i.i.d. sample of size N and distribution fV (see Arnold,

Balakrishnan, and Nagaraja [3]).

Figure 2 displays the truncated density function of the

transaction price in the upstream exchange. As previously

mentioned, the distribution has three parts: the transaction

price w equals zero when the inventory is not allocated, w

equals the reserve price when only one potential bidder bids

above r, and w follows the distribution fˆW when more than

one bidder values the opportunity above r.

As a result, the probability density function of w in the

presence of a reserve price is:

�

� D0

∗

fW

(w; θ) = FV (r; θ)N

(12)

�

� D1

N FV (r; θ)N −1 [1 − FV (r; θ)]

�

�1−D0 −D1

N (N − 1)FV (w; θ)N −2 [1 − FV (w; θ)]fV (w; θ)

where D0 and D1 are indicator variables. D0 = 1 if all bids

are below the reserve price and 0 otherwise. On the other

hand, D1 = 1 if and only if one of the bids is above the

reserve price.

Since the dataset does not contain information about auctions with the highest bid below r, we use the truncated

version of equation 12 (see Amemiya 1985 [2]),

fW (w; θ) =

N FV (r; θ)N −1 [1 − FV (r; θ)]

1 − FV (r; θ)N

!D1

N (N − 1)FV (w; θ)N −2 [1 − FV (w; θ)]fV (w; θ)

1 − FV (r; θ)N

where Q corresponds to the total number of auctions conducted for a particular type of inventory.

Remember that θ corresponds to the vector of parameters characterizing distributions FV and fV . Since we do

not have information about auctions with the highest bid

below the current floor, we need a parametric distribution

to make out of sample predictions. That is, to obtain the

optimal reserve price, we need to evaluate the expected revenues when floors are below the current one. This type of

inference cannot be done using nonparametric approaches.

However, choosing a parametric form has some risks linked

to misspecification that can lead to poor results. We can

assume different parametric forms as long as they have positive support. In our application, we use the Weibull family

with density function defined as

(13)

!1−D1

Note that fW does not depend on the probability of winning

the downstream auction. This is because upstream bidders

have incentive to report their true valuation independently

of winning in the downstream exchange.

Given the likelihood function in 14, we can estimate the

vector of parameters θ by minimizing the negative log likelihood. That is,

θ∗ = arg min -log(L)

θ

(15)

In order to compute optimal reserve prices in equation 8,

we also need to estimate the relationship between the probability of winning the downstream auction PD , and the expected conditional transaction price w̄T . In this paper, we

assume a simple linear relationship between both variables,

PD (w̄T ) = γ0 + γ1 w̄T (r) + ǫ

(16)

where γ0 and γ1 correspond to the intercept and slope respectively. ǫ captures possible measurement errors and unobserved factors for the upstream auction designer. Assuming that ǫ is i.i.d. and it is neither correlated with w̄ nor

r, we estimate the parameters using ordinary least squares.

If the assumptions hold, the resulting estimates of γ0 and

γ1 are unbiased. However, we are aware that some correlation between w̄ and the unobserved part may exists. For

instance, the value of the inventory opportunity may depend

on the hour of the day or type of user, affecting the probability of winning the downstream auction and the expected

upstream transaction price. This omitted variable problem

may be solved by using instrumental variables. Further research should be devoted to avoid this confounding problem.

Given the parameter estimates, we use the optimality condition 8 to compute the upstream optimal reserve price when

we account for the existence of a downstream exchange (ρ∗c ).

Similarly, we will use condition 9 when we do not account

for the existence of downstream auctions (ρ∗u ).

6. DATA AND ESTIMATE RESULTS

We use data provided by BrightRoll Video Exchange and

estimate the optimal reserve price for inventory with and

without a downstream marketplace. In the case where there

is only one exchange managing the ad-request, BrightRoll is

the only one deciding which bidder will deliver the advertisement. On the other hand, when there exists a downstream

�valuation of inventory A (F̆V ) with the Weibull parametric

approximation (FV ). Given the aforementioned limitations

of the nonparametric approach, the comparison is only possible for the range of observed data. In this particular example, the nonparametric representation is limited to values

above the current reserve price set at 2.67 dollars eCPM.

In order to compute the nonparametric distribution, we

use the definition of cumulative distribution function of the

second order statistic F̆W ,

Placement A

Cumulative Distribution Function - Fv

1

ML-Estimated CDF

Nonparametric CDF

0.95

0.9

0.85

0.8

F̆W = N ∗ F̆v(N −1) − (N − 1) ∗ F̆vN

0.75

where N is assumed to be known.2 F̆W can be constructed

using observed data. Given this information, we just need to

find F̆V such that the equality in 17 holds. In the particular

case of A, the Weibull and the nonparametric distributions

are pretty close. This is not always the case.

Given the estimates of the density and cumulative distribution functions, we use ordinary least squares to estimate

the parameters that define the relationship between PD and

w̄T (equation 16). Further details about how we estimate

the equation can be found in Appendix 1.

Once all the parameters of the model are estimated, computing reserve prices ρ∗c and ρ∗u follows from equations 8

and 9 respectively.

0.7

0

10

20

30

40

50

Valuation - v

Figure 3: Inventory A: ML vs Nonparametric CDF

marketplace, we will estimate the reserve price taking into

account that the winner of the BrightRoll exchange will compete against other bids in a downstream auction. In such

a case, the BrightRoll Exchange will be considered the upstream marketplace.

We used 2 weeks data and experimented with inventory

with and without downstream auctions. Such an inventory captures a significant amount of revenue for BrightRoll.

We studied 71 placements for the case where we only have

one exchange, and 30 placements with a downstream marketplace. Due to the large amount of data and expensive

computations, we decided to implement the algorithm using

Apache Spark, a general-purpose cluster computing system

designed to deal with this type of tasks.

We estimated the optimal floor for each placement during

the first 3 days of the experiment. Then we computed the

average of the daily results weighted by the number of adrequests. The resulting inventory floors were used in the

A|B test during the remaining days of the experiment.

In this paper, we assume that in our training set all downstream exchanges conduct a first price auction and upstream

marketplaces use a second price auction. In reality, this is

not always the case. For some placements, exchanges work

in the opposite way: the downstream uses a second price

and the upstream marketplace a first price auction. For

this type of inventory, our results can be interpreted as a

simulation exercise of the consequences of applying optimal

floors if placements used the business model considered in

the paper.1

For each of placement, we estimate the distribution of bidders’ valuation using expression 15. As previously discussed,

the use of a parametric distribution may have misspecification problems. However, in our application this approach

is necessary in order to deal with data limitations. We

could test how close the parametric approach is from the

nonparametric model, and compare the behavior of different parametric families. However, in this paper we will use

the expected lift of our recommended floors with respect to

the currently implemented ones in order to asses the success of our model. As an illustration, Figure 3 compares the

nonparametric cumulative distribution function of bidder’s

1

We are aware that some bias may exist in the estimates

linked to the downstream correction term (PD ).

(17)

7. A|B TEST RESULTS

We conducted an A|B test in order to assess the impact of

recommended floors. For each placement, we randomly split

the ad-request traffic in two: 5% of the traffic is randomly

selected to be part of the group with the recommended floor

(test group), and the rest of the traffic will belong to the

control group and use the current reserve price.

In order for the reader to understand how we measure

the effectiveness of floor recommendations, Table 1 displays

two types of inventory which are denoted B and C. While

inventory B does not face a downstream auction, the upstream winner of C has to compete against bids from other

bidders in the downstream exchange. The F loor column in

Table 1 shows the implemented reserve price for the test

and control groups, and it is measured in dollars eCPM.

The variable Exp indicates if the row corresponds to the

test (Exp = 1) or control group (Exp = 0). N b Auctions

denotes the number of ad-requests for that particular type

of inventory. N b Successf ul indicates the number of adrequests that ends up with a winner in the upstream auction.

Column 6 corresponds to the ratio of successful auctions to

the total number of ad-requests. As the name indicates, column N b Impressions denotes the total number of shown

ads. The difference between the number of impressions and

successful auctions is displayed in column 8. Several reasons

explain why the number of impressions is different from the

number of successful auctions: first, having a winner in the

upstream exchange does not guarantee that the bidder is

going to win the auction conducted downstream. Second,

video advertisement is characterized by having a high fallout

rate. That happens when the winner of the ad-request is not

able to deliver the advertisement (e.g. due to creative errors

or latency problems loading the video). For simplicity, we

assume that the fallout rate is independent of the bid made

2

Since we know the identities of the upstream winners, we

use the inverse of the Herfindahl index to compute the number of effective competitors N .

�Inventory

B

C

Floor

($eCPM)

13.41

2.00

7.69

13.33

Exp

1

0

1

0

Nb

Auctions

68,872

1,308,445

1,770,254

33,613,967

Nb

Successful

60,151

1,194,116

281,262

844,257

Nb Successful /

Nb Auctions

87%

91%

16%

2%

Nb

Impressions

24,021

467,240

18,704

119,933

Nb Impressions/

Nb Successful

40%

39%

7%

14%

Revenue

Lift

8%

101%

Table 1: A|B Output

by potential buyers. Finally, the Revenue Lif t denotes the

expected revenue lift as a result of implementing the recommended floor. Note that the test and control groups are not

directly comparable, since the test group only corresponds

to 5% of all ad-requests. For that reason, we standardize the

amount using the total number of ad-requests in the test and

control groups.

If we look at inventory B in Table 1, we propose a 13.41

dollars eCPM reserve price instead of the current one set at

$2. As previously noted, the number of auctions assigned

to the test group is 5% of the total number of ad-requests.

Among these ad-requests, 87% of auctions in the test group

are successful. The percentage is lower than the one in the

control group (91%). This result is expected, since increasing the floor decreases the probability that an auction clears

(i.e. auction with at least one bidder above the floor). If

we look at the ratio of impressions to the number of successful auctions, around 40% of successful auctions led to

an impression in both groups. After standardizing the revenue, the expected revenue lift as a result of implementing

the recommended floor equals 8%.

Similar analysis can be done for inventory type C. In this

case, we recommend a floor below the current one (7.69 dollars eCPM instead of $13.33). Lowering the floor, the ratio

successful to total auctions in the upstream marketplace increases from 2% to 16%. Once again, this result is expected

since lowering floors rises the probability that at least one

bidder bids higher than the reserve price. In contrast to

inventory B, in C the ratio of impressions to number of successful auctions in the test group is half of the control. This

is consistent with the existence of downstream auctions. As

previously noted, the upstream winner of inventory C has

to face the competition from other bids submitted in the

downstream auction. Decreasing the reserve price, increases

the number of auctions that clears upstream. However, it

decreases the bid passed to the downstream exchange, decreasing the probability of winning the downstream auction.

This is not the case in auctions of type B, where the ratio of

impressions to number of successful auctions is the same for

the control and test groups. In placements without downstream exchanges, like inventory B, winners do not face competition from other marketplaces. If this is the case, the only

reason that explains that the ratio is lower than one is fully

attributed to fallout, that is assumed to be independent of

the transaction price.

We computed and tested the impact of optimal floors on

inventory with and without downstream auctions. Due to

business requirements, in the A|B experiment we applied

the floor resulting from expression 9 and denoted as ρ∗u . We

did not directly applied the correction for the existence of

a downstream exchange as appearing in equation 8 (ρ∗c ).

Instead, we use the data resulting from the experiment and

the predicted downstream winning probability to evaluate

the optimal floor with the downstream correction. Further

details about how we evaluate the effects of the corrected

optimal floors can be found in Appendix 2.

Table 2 displays the impact of implementing the new floors.

Results are aggregated for confidentiality reasons. The first

column describes the type of inventory: the first row corresponds to auctions without a downstream exchange. The

second row describes the impact of implementing uncorrected optimal floors on inventory with downstream auctions

(ρ∗u ). Finally, the third row describes auctions with a downstream marketplace and corrected optimal reserve price ρ∗c .

Column N b P lacements captures the number of placements

in the experiment. We tested optimal floors in 71 placements

without downstream auctions. Similarly, we studied the impact of changing floors in 30 placements with a downstream

marketplace. The third column describes the percentage of

placements that lead to a lift in revenues. This is one of the

main indicators to assess the validity of our predictions. For

the case of placements without downstream auctions, 77% of

our recommended floors (one for each placement) led to an

increase in revenue. Performance decreases when applying

the uncorrected optimal floor ρ∗u to placements with downstream auctions. In this case, 67% of the recommendations

led to an increase in revenues. The last row displays the effects of using ρ∗c . In this situation, 77% of the recommended

floors led to an increase in revenue. The latter result indicates that the corrected floor ρ∗c outperforms the standard

formulation of optimal monopoly floors without the correction (ρ∗u ).

Placements are very heterogeneous. They may differ in

terms of publisher, targeted device, number of ad-requests,

etc. Consequently, the effects of implementing optimal floors

at placement level can be very different. For that reason, we

decided to report the overall revenue lift and not the average across placements. The last column in Table 2 shows

the expected revenue lift as a result of the recommendations.

This indicator is computed using the total revenue generated

across all analyzed placements in the control group and the

standardized revenue of the test group. Implementing optimal reserve prices increases revenue. In the case of placements without downstream marketplaces, the expected revenue lift equals 39%. Consistent with the theoretical findings, the optimal reserve price with downstream correction

outperforms the uncorrected monopoly price: 29% revenue

lift when using ρ∗c vs 25% when testing ρ∗u . Note that the

revenue lift as a result of new floors is lower in exchanges

with downstream auctions than without. Differences between both types of inventory may be one of the reasons

that explains such as discrepancy. As discussed in the introduction, the use of several exchanges may help publishers to

increase competition for the inventory, decreasing the effectiveness of floors.

Table 3 disaggregates previous results by type of recom-

�Type of Placement

Nb Placements

No Downstream Auction (ρ∗u )

Downstream Auction: No Correction (ρ∗u )

Downstream Auction: Correction (ρ∗c )

71

30

30

Placements

with Positive Revenue Lift (%)

77%

67%

77%

Expected Revenue Lift (%)

39%

25%

29%

Table 2: Aggregated A|B Test Results

Type of Placement

No Downstream Auction (ρ∗u )

- Above Current Floor

- Below Current Floor

Downstream Auction: No Correction (ρ∗u )

- Above Current Floor

- Below Current Floor

Downstream Auction: Correction (ρ∗c )

- Above Current Floor

- Below Current Floor

Nb Placements

Placements

with Positive Revenue Lift (%)

Expected Revenue Lift (%)

24

47

88%

72%

38%

40%

9

21

100%

52%

92%

11%

13

17

100%

71%

88%

22%

Table 3: A|B Test Results by Recommendation Type

mendation: above and below the current reserve price. For

inventory without downstream auctions, 24 out of 71 placements have a recommended floor above the current one, and

47 out of 71 have a lower recommendation. The performance of the recommended floors is linked to the available

data. Remember that we only have data about auctions

where the highest bid is above the reserve price. As a result, we have to infer the shape of the distribution of buyers’

valuation for values below the current floor, decreasing the

performance of recommendations. As expected, the model

behaves better when we recommend above: 88% of recommendations above the current floor led to a positive revenue

lift, and 72% for recommendations below the current reserve

price. When analyzing the impact of uncorrected floors (ρ∗u )

on inventory with a downstream auction, all recommended

floors above the current ones led to an increase in revenue.

On the other hand, only 52% of recommendations below the

current floor led to a rise in revenue. Finally, the last three

rows in Table 3 displays the performance of recommended

floors when we correct for the existence of a downstream

auction (ρ∗c ). We can see that we improved revenue in 100%

of placements where we make recommendations above the

current reserve price. On the other hand, effectiveness decreases to 71% when we recommend below. Once again, in

the presence of other exchanges ρ∗c performs better than ρ∗u .

8. CONCLUSION

In this paper, we derive the reserve price that BrightRoll

Video Exchange should charge in order to maximize its expected profits when inventory opportunities come from other

marketplaces. We prove that the classical approach to derive

the monopoly reserve price is suboptimal. Consistent with

the theoretical findings, in our application the downstreamcorrected reserve price increases the expected revenue of the

marketplace with respect to the current floor and the classical derivation of the optimal monopoly price. The proposed

algorithm also deals with data challenges commonly faced

by exchanges: limited number of logged bids per auction,

and limited information about inventory coming from other

exchanges.

The model can easily accommodate features. As a re-

sult, we can derive different floors depending on supply and

demand characteristics (e.g. hour of the day, user characteristics, video format,...). Moreover, the relevance of this

study transcends its particular context and is applicable to

a wide range of scenarios where sequential auctions exist

and where marketplaces interact with each other. Finally,

further research can be devoted to analyze the endogeneity

problem when deriving the relationship between the probability of winning downstream and the expected transaction

price.

9. REFERENCES

[1] Global entertainment and media outlook 2015-2019.

http://www.pwc.com/outlook.

[2] T. Amemiya. Advanced econometrics. In Cambridge,

Massachusetts: Harvard University Press, 1985.

[3] B. C. Arnold, N. Balakrishnan, and H. N. Nagaraja. A

first course in order statistics. In New York: John

Wiley & Sons, 1992.

[4] B. Edelman, M. Ostrovsky, and M. Schwarz. Internet

advertising and the generalized second price auction:

Selling billions of dollars worth of keywords. National

Bureau of Economic Research, 2005.

[5] J. Feldman, V. Mirrokni, S. Muthukrishnan, and

M. M. Pai. Auctions with intermediaries: extended

abstract. In the ACM EC, 2010.

[6] V. Krishna. Auction theory. In Massachusetts:

Elsevier Academic Press, 2nd edition, 2010.

[7] R. P. McAfee and D. Vincent. Sequentially optimal

auctions. Games and Economic Behavior,

18(2):246–276, 1997.

[8] R. B. Myerson. Optimal auction design. Mathematics

of operations research, 6(1):58–73, 1981.

[9] H. J. Paarsch and H. Hong. An introduction to the

structural econometrics of auction data. In Cambridge,

Massachusetts: MIT Press, 1st edition, 2006.

[10] J. G. Riley and W. F. Samuelson. Optimal auctions.

The American Economic Review, pages 381–392, 1981.

[11] L. C. Stavrogiannis, E. H. Gerding, and M. Polukarov.

Auction mechanisms for demand-side intermediaries in

online advertising exchanges. In the 13th international

�conference on autonomous agents and multiagent

systems. AAMAS, 2014.

[12] H. R. Varian. Position auctions. International Journal

of Industrial Organization, 25(6):1163–1178, 2007.

[13] S. Yuan, J. Wang, B. Chen, P. Mason, and S. Seljan.

An empirical study of reserve price optimisation in

real-time bidding. In Proceedings of the 20th ACM

SIGKDD international conference on Knowledge

discovery and data mining. ACM, 2014.

10.

10.1

APPENDIX

Appendix 1: Estimation of the Winning

Downstream Auction Probability

This section includes further details about the estimation

of PD (w̄T ) in equation 16. In order to estimate δ0 and δ1

we first need to construct the dependent variable PD and

the covariate w̄T (r). We trim the dataset discarding auctions within the 4th quantile ordered by the highest bid.

As a result, the remaining data set only contains auctions

with a highest bid between the reserve price and the 3rd

quantile. Then we select twenty equidistant cutoff points.

For each cutoff, we compute the revenue and the ratio of

impressions to number of successful auctions resulting from

auctions with a highest bid greater than the cutoff point.

Each cutoff point is like imposing a reserve price, since auctions below each point do not clear. As a result, we will have

twenty {PD (w̄T )l , w̄T l } for l ∈ {1, ..., 20} pairs. Given the

resulting pairs, we will use ordinary least squares to have an

estimate of δ0 and δ1 .

10.2

Appendix 2: Estimation of the Winning

Downstream Auction Probability Evaluated at the Optimal Floor

For each tested inventory with downstream auctions, we

use equations 8 and 16 to compute the optimal reserve price

ρ∗c and the predicted probability of showing the impression

evaluated at the optimal floor (PD (ρ∗c )). For a given inventory, the corrected optimal floor ρ∗c is greater than the

uncorrected one ρ∗u . This result allows us to use data from

the test group to evaluate the performance of PD (ρ∗c ). We

have information about all auctions that successfully cleared

even the ones that did not lead to an impression. From the

model, we are able to compute the floor with downstream

correction ρ∗c and estimate the probability of winning the

downstream auction for that particular floor PD (w̄T (ρ∗c )).

In order to compute the expected revenue as a result of

imposing the corrected optimal floor ρ∗c , we use the expression 6, the parameter estimates resulting from minimizing

equation 15, and estimates from equation 16.

We also need to estimate the number of impressions resulting from increasing the probability of winning the downstream auction. Using the test group data, we remove successful auctions with the highest bid below ρ∗c (Successf ulc ).

We sum the total number of impressions from the trimmed

dataset (Impressionsc ). Using expression 10 we compute

the expected transaction price given ρ∗c . Given w̄T (ρ∗c ) and

using equation 16 and its corresponding estimates, we compute the expected probability of winning the downstream

auction P̂D (w̄T (ρ∗c )).

We use P̂D (w̄(ρ∗c )), Impressionsc , and successf ulc , to

find the extra number of impressions x resulting from increasing the probability of winning downstream as follows,

P̂D (w̄(ρ∗c )) =

Impressionsc + x

Successf ulc

(18)

Once we obtain x, we can compute the corresponding revenue. While the revenue generated from Impressionsc is

easy to compute, the revenue from the new impressions (x)

is trickier. The transaction price for impressions x will be

equal to the floor with correction ρ∗c . The argument here

is as follows: if the new x impressions clear, it must be

as a result of increasing the floor. So the clearing price

will be ρ∗c . For instance, imagine that the ratio of impressions to number of successful auctions for the corrected floor

equals 0.14 (i.e. P̂D (w̄(ρ∗c )) = 0.14). We know that we

have 1,000 successful auctions (i.e. successf ulc = 1000),

and 100 impressions that qualify with the new floor (i.e.

Impressionsc = 100). Then the number of new impressions

(x) clearing at the new floor is 40, and the transaction price

of each of these extra impressions equals the aforementioned

corrected floor ρ∗c .

�