Journal of Banking & Finance 30 (2006) 1309–1332

www.elsevier.com/locate/jbf

Spanish Treasury bond market liquidity

and volatility pre- and post-European

Monetary Union q

Antonio Dı́az a, John J. Merrick Jr.

a

b,*

, Eliseo Navarro

a

Universidad de Castilla-La Mancha, Facultad de C. Económicas y Empresariales, 02071 – Albacete, Spain

b

School of Business, College of William and Mary, P.O. Box 8795, Williamsburg,

VA 23187-8795, United States

Received 19 April 2004; accepted 12 April 2005

Available online 27 June 2005

Abstract

Spain enacted a number of important debt management initiatives in 1997 to prepare its

Treasury bond market for European Monetary Union. We interpret the impacts of these

changes through shifts in a bond liquidity ‘‘life cycle’’ function. Furthermore, we highlight

the importance of expected average future liquidity in explaining Spanish bond liquidity premiums. We also uncover pricing biases that support the Spanish TreasuryÕs tactical decision to

target high-coupon, premium bonds in its pre-EMU debt exchanges. Finally, we show that

EMU has been associated with both a decrease in bond yield volatility and an increase in pricing efficiency.

� 2005 Elsevier B.V. All rights reserved.

q

This project developed while Merrick was at Baruch College. The authors acknowledge useful

comments from participants in BaruchÕs Brown Bag Seminar series. Furthermore, Dı́az and Navarro

acknowledge the financial support provided by Junta de Comunidades de Castilla-La Mancha grant

PAC2002/01 and by Ministerio de Ciencia y Tecnologı́a grant BEC 2001-1599.

*

Corresponding author. Address: School of Business, College of William and Mary, P.O. Box 8795,

Williamsburg, VA 23187-8795, United States. Tel.: +1 757 221 2891; fax: +1 757 221 2937.

E-mail addresses: antonio.diaz@uclm.es (A. Dı́az), john.merrick@business.wm.edu (J.J. Merrick Jr.),

eliseo.navarro@uclm.es (E. Navarro).

0378-4266/$ - see front matter � 2005 Elsevier B.V. All rights reserved.

doi:10.1016/j.jbankfin.2005.05.009

�1310

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

JEL classification: G12; G15

Keywords: Bonds; Liquidity; Spanish public debt; European Monetary Union

1. Introduction

This paper examines liquidity and volatility in the Spanish Treasury bond market

within the context of debt policy shifts engineered by the Spanish government in

preparation for entrance into European Monetary Union.1 The TreasuryÕs mid1997 debt management innovations were designed to make Spanish debt more

attractive to the new class of Pan-European government bond investors created

under European Monetary Union. These measures included (1) increases in the size

of new issues, (2) increases in the time between bond issuance tranches, (3) development of a strips market and (4) institution of a new aggressive exchange policy to

replace certain seasoned issues. A key purpose of this paper is to investigate the impact of SpainÕs debt management initiatives on both trading activity and valuation in

its debt market. As it happens, SpainÕs concerns over properly preparing its markets

for dramatic shifts in the relevant investor class under EMU turned out to be quite

prescient. The share of Spanish government debt held by non-resident investors

climbed from 25% in 1996 to 47% by February 2003.2

Analysis of SpainÕs actions and experiences during these special circumstances

provides a number of specific insights on market structure and policy impacts of

interest to both policymakers and academic researchers. To facilitate these insights,

we estimate a model that relates individual Treasury issue market share of overall

trading volume to a bondÕs age (the time since its initial auction) in a fashion best

described as a liquidity life cycle. We then test for shifts in this liquidity life cycle

function as a result of the TreasuryÕs debt policy innovations. We also estimate

the structure of liquidity premiums in the different maturity sectors within the Spanish bond market and quantify the impacts of SpainÕs EMU-related debt management

policy shifts on Spanish Treasury bond valuation. We conclude by examining the impacts of European Monetary Union on volatility and pricing efficiency in the Spanish Treasury market.

1

In general, prudent debt management by any sovereign requires attention to market structure and

trading costs. Indeed, one of the three debt management goals espoused by the US Treasury is to

‘‘promote efficient markets’’ (see the US Treasury website). Likewise, the joint International Monetary

Fund-World Bank guidelines for developing country debt management list an entire menu of regulatory

and market infrastructure conditions designed to enhance debt market efficiency (see Box 5, ‘‘Relevant

Conditions for Developing an Efficient Government Securities Market’’, in International Monetary Fund/

World Bank (2001)).

2

Source: Spanish Treasury (Tesoro Público). In contrast, during the transition to EMU, trading volume

in the MEFFÕs (Mercado Español de Futuros Financieros) Spanish 10-year government bond future

contract withered away.

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1311

1.1. Bond market liquidity proxies and model specification

Liquidity is the somewhat amorphous financial market concept that embodies the

ease with which a security can be traded within a short period of time without causing significant impacts on prices. Liquidity is valuable because of the associated savings of both trading costs and trading time. Theoretically, investors should require

lower returns on assets with relatively high degrees of liquidity. The difference between the required return on liquid versus less liquid assets is called a liquidity premium. Issuers whose securities trade in liquid secondary markets should benefit

through lower costs of capital. This effect should hold for both debt and equity securities and for both private and sovereign issuers.3

Operationally, analysis of potential liquidity effects in the cash bond markets involves choosing both a specific observable proxy for liquidity and a security valuation

model. In this paper, we feature issue-specific trading volume market share and ‘‘auction status’’ proxies for liquidity. We test for the importance of liquidity effects by

using these liquidity proxies to explain the valuation residuals from a standard term

structure model. Our auction status approach attempts to follow the lead of the

empirical literature for the US Treasury market, where the most recently auctioned

or ‘‘on-the-run’’ issue in each maturity sector is distinguished from all other ‘‘offthe-run’’ issues. However, due to the special issuance system employed by the Spanish

Treasury, we propose the need for three different status stages: ‘‘pre-benchmark’’,

‘‘benchmark’’ and ‘‘seasoned’’.4 Furthermore, following Goldreich et al. (2005),

our empirical specifications stress the importance of distinguishing between current

and expected future liquidity. As it happens, this distinction is critically important

for understanding liquidity in the Spanish market. In particular, the pre-benchmark

Spanish Treasury bond has a low share of overall trading volume at issue, but carries

an expectation of a sharply increasing future market share. In contrast, the current

benchmark bond has a high current share of market trading volume, but carries an

expectation of a decreasing future share of market trading volume.

Our main results regarding the impacts of SpainÕs debt policy changes concern both

the liquidity life cycle of the typical bond and the value of liquidity. First, we show that

a specific continuous, highly non-linear function of bond age explains the typical

bondÕs changing market share of trading volume quite well. Moreover, we confirm that

important structural changes took place in the Spanish market during the approach to

monetary union. In particular, shifts in the liquidity life cycle modelÕs key parameters

after 1997 show that Spanish debt market trading activity became more concentrated

in benchmark bonds and reveal that the benchmark status period lengthened.

3

Sarig and Warga (1989), Amihud and Mendelson (1991), Warga (1992), Kamara (1994), Carayannopoulos (1996), Duffee (1998), Elton and Green (1998), Fleming (2001), Strebulaev (2001), Krishnamurthy (2002) and Goldreich et al. (2005) analyze liquidity in the US government debt markets. The

liquidity of Spanish government debt has been studied by Alonso et al. (2004), who apply the Elton and

Green (1998) methodology, and by Dı́az and Navarro (2002).

4

Alonso et al. (2004) propose similar stages for Spanish bonds.

�1312

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

We also present a number of interesting results concerning liquidity value in the

Spanish bond market. We show that our explicit life cycle function adds significant

explanatory power to the literatureÕs standard bond auction status dummy variable

approach. In particular, we use our estimated market share life cycle functions to

project each issueÕs future liquidity. This allows us to test for an empirical relation

between bond values and liquidity, while specifically distinguishing between the impacts of current versus expected future liquidity. Our results reveal that expected

future liquidity is much more important than current liquidity for explaining relative

Spanish Treasury bond values.

In addition, we examine the valuation impacts of bond-specific characteristics

such as the coupon rate and price premiums and discounts versus par. Our results

for the 1993–1997 sample period detect statistically significant valuation biases confirming that Spanish investors favored discount bonds over premium bonds. These

results lend support to the Spanish TreasuryÕs tactical decision to target high-coupon, premium bonds in its debt exchanges. Interestingly, we find that the impact

of such bond-specific characteristics on value in the Spanish market decreased after

European Monetary Union.

Finally, we examine the impacts of European Monetary Union on the volatility of

yields in the Spanish Treasury market. As anticipated by its early proponents, European Monetary Union led to dramatic falls in both yield levels and yield volatility for

‘‘Club Med’’ members such as Spain and Italy. For these countries, European Monetary Union membership decreased the relevant currency translation risks as well as

the perceived bond default probabilities. Formal tests here based on the first-differences of yields strongly reject the null hypothesis of equal yield variances in our preand post-EMU periods. Such an impact on volatility is generally acknowledged (see

Codogno et al., 2003). It is less widely recognized that European Monetary Union

has also led to more efficient relative pricing in the Spanish Treasury bond market.

Our results reveal that the residual variance of our liquidity and bond characteristicaugmented yield regressions fell sharply between our pre-EMU and post-EMU samples. Such improved pricing efficiency may be attributed to an important byproduct

of European Monetary Union: the creation of a much larger universe of euro-based

fixed income investors willing to focus attention on trading opportunities in any

member market without the hindrance of currency risk.

2. Institutional features of the Spanish Treasury debt markets

With total domestic Treasury debt of approximately €315 billion as of year-end

2002, Spain is the fourth largest euro zone sovereign debt market, trailing only Italy

(€1061 billion), Germany (€745 billion) and France (€732 billion) in total par

amount outstanding.5 Spanish Treasury debt consists of both bills and coupon-

5

Source: Security statistics, Bank for International Settlements, September 2003.

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1313

bearing notes and bonds. Letras del Tesoro (Treasury bills) are issued at discount

with 6-, 12- and 18-month maturities. Bonos and Obligaciones del Estado (Treasury

bonds and notes) bear annual coupon payments and have been issued for 3-, 5-, 10-,

15- and 30-year maturities. Letras del Tesoro and, since 1999, Bonos and Obligaciones have been traded free of withholding tax for non-residents and institutional

investors.

All Spanish Treasury debt is issued via competitive auction. However, the Spanish

Treasury traditionally has built up the total par amount of each new security by

keeping the same issue open over several (at least three) consecutive auctions. The

securities issued through each tranche were fully fungible since they shared the same

nominal coupon, interest payment and redemption dates, and security code. When

the total nominal amount issued reached the appropriate target size, the corresponding security code was closed, and any further issuance took place using a new security. The secondary market for Spanish Treasury debt is known as Mercado de

Deuda Pública Anotada or MDPA.6

Current practices in the Spanish market are the result of changes made by Spain

as it prepared for entry into European Monetary Union. Under EMU, the Spanish

Treasury recognized that it would have to compete directly with other euro zone sovereign debt issuers. Thus, beginning in mid-1997, the Spanish Treasury ‘‘prioritized

the achievement of a more liquid and efficient public debt market’’.7 In practical

terms, this meant undertaking a set of initiatives aimed to attract investor savings

within the new single capital market. Among these initiatives, we highlight the following measures designed to increase the depth and liquidity of the market:

1. Reform of the Treasury market makers regime adapting it to the EMU rules and

modifying the rights and obligations of public debt market makers and recognized

dealers;

2. Enlargement of Spanish public debt trading platforms through ‘‘the advance in

the blind segment of the Spanish market centred on the roll-out of a fully electronic trading system supporting automatic posting of public debt prices’’;

3. A change of the tax regime of the public debt;

4. An increase in the size of bond issues to total par amounts in the €11 billion to €12

billion range;

5. Organization of a Treasury strips market;

6. An increase in the range of issued Treasury maturities to include a 30-year bond;

6

The MDPA conducts trading through three systems. The first two are reserved for market members,

while the third is for transactions between market members and their clients. The first member system is a

‘‘blind market’’ electronic trading system conducted without knowledge of the counterpartyÕs identity,

while the second system channels all the remaining transactions between market members. The structure of

the Spanish market is quite similar to the US Treasury market (see Fleming and Remolona, 1999 for

details about the US Treasury market).

7

See ‘‘Memoria 2000’’ of Tesoro Público (http://www.mineco.es/tesoro/htm/deuda/Memorias/

indice_i.htm).

�1314

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

7. A new government debt exchange policy designed to replace certain seasoned, low

liquidity, high-coupon issues with new strippable, close-to-market coupon rate

bonds.

The debt exchanges provided a crucial mechanism through which to build par

amount size in new issues with current market coupon levels that would be priced

near 100% of par. This shift was designed to increase market liquidity and depth

through two channels. First, the exchange policy ensured an adequate tradable supply of bonds priced near par (at the expense of premium bonds that some classes of

investors avoid). Second, the debt exchanges produced the larger outstanding

amounts of strippable bonds that were critical in supporting bond dealer stripping

and reconstitution operations in the new strips market.8

3. Liquidity in the Spanish public debt market

In this section, we first describe our database and discuss alternative proxies for

liquidity in the Spanish Treasury bond market. We then analyze the impact of the

new EMU-related debt management policy shifts on bond trading activity and bond

liquidity.

3.1. The data

The original database consists of 65,135 observations derived from actual transactions in all Spanish Treasury bills and bonds traded in MDPA (obtained from annual files made available by the Banco de España) over the period from January 1993

to December 2002. For each issue, the Banco de España database reports daily information on the number of transactions and both the nominal and effective trading

volumes. The database also reports the maximum price, the minimum price and

the average price for each issue computed from all MDPA transactions over each

day in the sample. We match this information with each issueÕs coupon rate, maturity date, issue date and remaining coupon payment dates. We also track the par

amount outstanding of each issue at the end of each month. Table 1 gives a brief

overview of the average trading volume and par amounts outstanding where bonds

are grouped by original issuance date term-to-maturity. The 10-year sector is the

most actively traded maturity sector and accounts for about 41% of overall Treasury

market trading. In this paper, we focus on trading activity in the three most active

sectors: 10-, 5- and 3-years.

8

Government debt exchanges were conducted via competitive auction, in which the Treasury reserved

the right to decide the cut-off price. (Also, in 2001 and 2002, exchange transactions were substituted by

direct repurchases of the targeted high-coupon issues using the TreasuryÕs cash surpluses.)

�1315

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

Table 1

Spanish Treasury market database summary for the 1993–1997 and 1998–2002 sample periods

Bills

3-year

bonds

5-year

bonds

1993–1997

Daily data

Average volume per traded issuea

Average volume per sector

# Traded issues per day

# Observations

26.84

184.99

6.9

8539

94.26

440.49

4.7

5809

77.22

504.29

6.5

8117

Monthly data

% Days traded per issue

Average amount outstanding per issue

Average market share per issue

Average market share per sector

Average # outstanding issues

22.9%

74.6%

78.5%

1548

4265

4490

0.2%

3.7%

3.2%

10.1%

23.5%

27.1%

38.12

6.3

8.3

Global information

Total # issues in subsample

1998–2002

Daily information

Average volume per traded issuea

Average volume per sector

# Traded issues per day

# Observations

Monthly information

% Days traded per issue

Average

Average

Average

Average

amount outstanding per issue

market share per issue

market share per sector

# outstanding issues

Global information

Total # issues in subsample

255

18.33

97.53

5.3

6604

14.5%

16

136.23

485.81

3.6

4511

71.3%

12

9

99.50

708.73

7.1

8837

77.7%

13

15-year

bonds

30-year

bonds

24.94

34.05

1.4

1301

–

–

–

–

95.2%

87.0%

5022

5695

5.1%

1.0%

38.0%

1.3%

7.5

1.5

10

126.38

136.76

641.86

542.14

5.1

8.1

6430

10,256

1194

6986

7409

0.1%

4.0%

3.9%

4.6%

20.1%

25.4%

43.2

5.0

6.6

203

10-year

bonds

63.7%

3

37.63

93.64

2.5

3113

61.6%

–

–

–

–

–

–

61.71

84.47

1.4

1677

95.1%

6737

6262

6714

3.4%

1.0%

2.2%

43.2%

3.8%

3.0%

12.7

4.0

1.4

15

5

2

Average volume and amounts outstanding expressed in million € of par value. Issues are sorted by

maturity sector of original issue.

a

Average calculated after excluding sample points for issues with zero volume on the given day.

3.2. Empirical liquidity proxies in the previous literature

The literature recognizes a wide range of market condition variables and securityspecific characteristics related to bond liquidity. In the US Treasury market, a common liquidity proxy is a bondÕs bid–ask spread.9 Elton and Green (1998) suggest that

the best proxy for liquidity is trading volume, though Fleming (2001) finds improved

9

See, for example, Shen and Starr (1998), Chakravarty and Sarkar (1999), Hong and Warga (2000),

Chen and Wei (2001), Fleming, 2001), Gwilym et al. (2002) and Goldreich et al. (2005).

�1316

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

performance using the number of trades instead.10 The literature also promotes bond

age, auction status and issue size as relevant explanatory variables.11 For example,

Fisher (1959) uses the amount of bonds outstanding on the basis of the potential correlation between the existing stock of a particular bond and the flow of trade in the

bond. Sarig and Warga (1989) and Warga (1992) suggest that younger bonds are

usually traded more frequently. Warga (1992) uses an auction status dummy variable

that indicates whether or not an issue is ‘‘on-the-run’’ (i.e., the most recently issued

security of a particular maturity). Amihud and Mendelson (1991) observe that bonds

approaching maturity are significantly less liquid since they are ‘‘locked away’’ in

investorsÕ portfolios. Importantly, Goldreich et al. (2005) emphasize expected liquidity over the full life of the issue – not just the current level of any liquidity measure –

as the most relevant theoretical constructs for valuing bond liquidity.

Here, we analyze the evolution of Spanish Treasury bond liquidity with respect to

auction status and bond age. We argue that the two-stage (on-the-run/off-the-run)

division traditionally used for US Treasury debt is not the most suitable choice

for Spanish Treasury assets over our sample period since the Spanish Treasury built

up its issues through a series of issuance tranches. Thus, the most recently issued

security (the on-the-run) might have been only one-fourth or one-third of the size

of the first off-the-run issue. This important relative issue size difference suggests that

the on-the-run issue need not have the highest current liquidity.12 Moreover, detailed

analysis of the data motivates a more sophisticated approach to modeling the evolution of a typical bondÕs trading activity over its life cycle. As it happens, this approach also allows us to build appropriate measures of expected average future

liquidity to maturity for any issue on any trading date. Thus, this approach is particularly convenient for distinguishing between the values of current and future

liquidity for Spanish Treasury bonds in the spirit of Goldreich et al. (2005).

We use individual issue market share of total trading activity as the measurable

proxy for relative liquidity.13 Many previous studies of bond market liquidity analyze raw trading volume (see, for example, Elton and Green, 1998; Fleming,

2001). We prefer the market share measure to raw volume measure since Spanish

Treasury bond trading volumes trended higher over the 1993 to 2002 sample period.

Scaling these individual issue volumes by total market volume both detrends these

data and controls for week-to-week volume fluctuations that are unrelated to relative

liquidity. Let the market share measure MSit for security i during week t be calculated as the ratio of the par value traded in bond i to the total par value traded

10

Shulman et al. (1993) uses trading frequency and Houweling et al. (2002) use the number and

dispersion of quotes per day.

11

Other variables that have been used include the volatility of interest rates (Kamara, 1994) and the

percentage growth of mutual funds (Fridson and Jónsson, 1995).

12

As it happens, in mid-2002 (near the end of our sample) Spain ultimately became confident enough to

approach the market with large enough initial tranches such that new issues immediately become

benchmarks.

13

We choose among volume-based measures since the Banco de España database does not include bid–

ask quotes.

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1317

by all outstanding issues. The MSit variable allows us to compare the degree of

liquidity among issues and to monitor the evolution of the liquidity of a given issue

throughout its life.

We divide the life of a Spanish Treasury bond issue into three status stages. We

term the first stage to be the ‘‘pre-benchmark’’ period – beginning at the issue of a

new bondÕs initial tranche (the bond is also by definition the ‘‘on-the-run’’ issue at

this time). This pre-benchmark period covers the time during which the issueÕs market share increases with age, but still lies below the market share of the former onthe-run bond. The second stage is the ‘‘benchmark’’ period. This stage corresponds

to the period during which the issue has the highest market share among all outstanding issues of the same original maturity. The last stage is the ‘‘seasoned’’

(post-benchmark) period. The seasoned stage corresponds to the period beginning

the week that the particular bondÕs market share is eclipsed (by a newer and now sufficiently liquid issue) and ends at the bondÕs maturity.

3.3. The impact of EMU preparations on liquidity

SpainÕs debt management policy changes generated important shifts in issuance

tranches, outstanding issue sizes and the evolution of bond auction status stages.

Panel A of Table 2 reports two sets of summary statistics on issue par amounts for

both individual tranches and total issue sizes for each of the three main bond maturity

sectors: 10-, 5- and 3-years. The 1993–1997 and 1998–2002 sample splits were chosen

to reflect the two different Spanish issuance policy regimes. The latter subsample begins after the 1997 shift toward larger issue sizes. Note that tranche sizes were reasonably similar across the two regimes. However, the number of tranches increased so

that the par amounts outstanding after the last tranche essentially doubled across

board. The shifts in issuance policy also had an important effect on bond status. Panel

B of Table 2 presents summary statistics on the evolution of the lengths of the crucial

pre-benchmark and benchmark stages in a bondÕs life cycle. The average length of the

pre-benchmark stage is similar across issuance regimes, but the length of the benchmark stage is considerably larger during the post-1997 period.

3.4. Modeling the market share function

So far, we have classified bond liquidity using three discrete status categories.

However, individual bond market shares of trading may be more generally modeled

as smooth, non-linear functions of bond age. Here, we posit a parsimonious function

to describe the behavior of individual bond market share (MSit) as a function of

bond age (Ageit):14

14

Eq. (1) is inspired by forms arising from actuarial research on human mortality (see Heligman and

Pollard, 1980). That literature uses this functionÕs ‘‘hump’’ to capture the impact of traffic accidents on

mortality rates of 15–25-year-olds within a general mortality-versus-age relationship.

�1318

Table 2

Effects of Spanish debt management changes on issuance and bond benchmark status

Years to maturity in each tranche

Minimum

Maximum

Amount outstanding

after the first tranche

Amount outstanding

after the last tranche

Panel A: Evolution of the issuance tranches and amounts outstanding (million € par value) by sector

1993–1997

3-year bond

2.21

3.54

3.09

900

5-year bond

4.21

5.54

5.00

934

10-year bond

9.42

10.54

10.01

890

15-year bond

12.71

15.63

14.20

245

30-year bond

–

–

–

–

1075

1285

1198

676

–

–

1998–2002

3-year bond

5-year bond

10-year bond

15-year bond

30-year bond

1350

1686

2371

1691

2128

10,769

11,152

13,737

10,599

7532

2.22

4.29

8.96

12.64

28.24

Number

of new

issues

3.98

5.98

11.06

15.65

31.54

3.14

5.12

10.21

14.65

30.06

824

881

1031

575

620

Weeks between adjacent auctions

Weeks that a bond keeps

pre-benchmark status

Minimum

Weeks that a bond keeps

benchmark status

Average

Minimum

Maximum

Average

Minimum

Maximum

Average

Panel B: Evolution of bond auction status by sector

1993–1997

10-year bond

8

13

43

5-year bond

8

6

82

3-year bond

9

6

69

33

30

26

3

5

1

28

81

67

16

27

17

12

2

4

49

87

92

33

41

37

1998–2002

10-year bond

5-year bond

3-year bond

50

54

38

3

0

0

34

21

27

16

16

17

31

32

32

58

75

68

40

53

53

5

5

4

38

31

4

Maximum

5385

6076

5830

4171

71

74

56

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

Average amount

per auction

(million €)

Average

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

2

Ageit

MSit ¼ b1 exp½�b2 ðAgeit � b3 Þ � þ b4 � b5

þ uit .

1319

ð1Þ

The first term allows for a hump in the liquidity profile during the first few years

of bond life. The second term is a decreasing exponential function that describes the

declining trading activity of the bond as it approaches maturity. The third term is a

random error.

The parameters in Eq. (1), with expected signs given in parentheses, can be interpreted as follows:

1. b1 measures the degree of concentration of trading activity in the benchmark

bond, i.e., the size of the hump (b1 > 0);

2. b2 is inversely related to the length of the period over which a bond keeps the

benchmark status, i.e., the width of the hump (b2 > 0);

3. b3 is the bond age at which the functionÕs first term (the liquidity hump) has the

highest amplitude (b3 > 0);

4. b4 is the initial value for the exponential function component (b4 > 0);

5. b5 relates to the speed at which a seasoned bondÕs trading activity changes with

time (1 P b5 > 0).

For positive values of all parameters, the MS(Æ) function is also positive.

We apply equation (1) to weekly data on individual bond issue shares of trading

volume for all original-issue 10-, 5- and 3-year bonds in our database.15 Table 3 presents the parameter estimates for Eq. (1) for the two subsamples suggested by the

changes in Spanish Treasury issuance policy. All reported individual t-statistics embody the Newey–West correction. Consider first the estimates for 10-year bonds over

the 1993–1997 period presented in Panel A. The regressionÕs adjusted R-square of

71.2% reveals that, through the functional form given by Eq. (1), bond age does a

very good job of explaining market share in the 10-year sector. As expected, all five

coefficient estimates are positive in sign and significantly different from zero (all individual coefficient t-statistics have p-values of 0.00). The most interesting individual

^ ¼ 0.67 and b

^ ¼ 18.47. The b

^ estimate reveals that the peak in a

estimates are b

3

1

3

typical 10-year bondÕs market share occurs two-thirds of a year after its first issue

^ implies that the shift in the 10-year bondÕs market share

date. The estimate for b

1

versus its baseline value at this peak point is about 18.5%.16

The 10-year sectorÕs results for the 1998–2002 period are qualitatively similar.

However, the key coefficients exhibit very interesting quantitative shifts. The

new estimate for b1 implies that the peak shift in the 10-year bondÕs market share

is now 23.5% (about 5% higher versus the earlier period) indicating that trading

15

While we prefer the market share measure, the results from using raw volume as the dependent variable

were qualitatively similar. However, see Footnote 16 below.

16

Some experimentation showed that the reported parameter estimates are robust to the choice of

specific starting values in the non-linear least squares estimation procedure. Ironically, the estimates

generated when using raw volume as the dependent variable are highly sensitive to the initial set of

parameters.

�1320

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

Table 3

Estimates of the market share life cycle function

Sample period: 1993–1997

Sample period: 1998–2002

Coefficients

t-Statistics

Coefficients

t-Statistics

Panel A: 10-year bonds

b1

b2

b3

b4

b5

Adjusted R2 (%)

# Observations

18.47

4.16

0.67

2.16

0.89

71.2

1686

(34.11)

(12.00)

(37.96)

(6.80)

(22.95)

23.50

2.43

0.83

4.85

0.69

76.3

3193

(24.88)

(8.75)

(35.68)

(4.03)

(16.65)

Panel B: 5-year bonds

b1

b2

b3

b4

b5

Adjusted R2 (%)

# Observations

5.95

0.56

0.64

1.76

0.86

36.2

2020

(3.64)

(2.52)

(3.75)

(0.81)

(3.14)

10.43

3.00

0.89

4.69

0.75

63.6

1700

(15.74)

(5.85)

(32.27)

(5.46)

(20.54)

Panel C: 3-year bonds

b1

b2

b3

b4

b5

Adjusted R2 (%)

# Observations

7.87

0.67

0.53

0.16

1.15

38.9

1502

(5.53)

(2.78)

(6.39)

(0.10)

(0.31)

11.11

1.83

0.88

1.06

1.10

60.5

1102

(18.75)

(6.84)

(32.65)

(1.43)

(4.35)

Non-linear least squares regressions of the market share (MSit) of the bond i during week t on Ageit of the

bond for two sample periods: 1993–1997 and 1998–2002. MSit is the trading volume of bond i during week

t divided by total trading volume of all Treasuries during week t. The regression equation is

Ageit

MSit ¼ b1 exp½�b2 ðAgeit � b3 Þ2 � þ b4 � b5

þ uit .

Newey–West adjusted t-statistics are in parenthesis.

activity became more concentrated in the benchmark bond in this later period.

Moreover, the market share peak in the later period comes later (0.83 years versus

^ is shorter in the second period, suggesting that the

0.67 years). Furthermore, b

2

^ is lower in the second

benchmark bond tends to keep this status longer. Finally, b

5

period, indicating that the liquidity of seasoned bonds decays even faster than in the

earlier period.

Panels B and C of Table 3 present corresponding results for the original-issue

5-year and original-issue 3-year bond sectors, respectively. The adjusted R-square

for each of the regressions reveals that bond age also provides important explanatory

power for market share in these maturity sectors. The explanatory power is much

larger in the later 1998–2002 sample. Moreover, as in the 10-year sector, the estimates for b1 imply that trading activity for both the 5- and 3-year sectors became

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1321

more concentrated in the benchmark bond in the later period. Moreover, in the later

period, the market share peaks appear later in bond life as well. However, the estimates for b1 show that the magnitudes of the benchmark effects for 5- and 3-year

bonds in both periods are less than one-half of the corresponding values for 10-year

bonds.17

The point estimates presented in Table 3 suggest increases in both the height and

width of the liquidity functionÕs ‘‘hump’’ in each sector in the later period. To examine whether the issuance policy shifts in mid-1997 had any effect on the structure of

Spanish Treasury bond liquidity, we apply the Chow test for structural change to the

coefficients in Eq. (1) after December 1997. The p-values for the Chow test statistics

are 0.00 in all three sectors. Schmidt and Sickles (1977) argue that the Chow statistic

may overstate the true test size in the presence of heteroscedastic residuals. Thus, we

also review the results for the individual equation coefficient estimates b1 through b5

and their reported Newey–West corrected estimated coefficient standard errors. For

each sector and subsample, consider the two standard error bounds around the estimated equation coefficients. For each sector there is at least one b estimate for which

the two standard error bounds do not overlap across subsamples.18 Taken together,

these results are consistent with the hypothesis that the mid-1997 changes in issuance

policy induced significant shifts in the liquidity structure of the Spanish Treasury

market.

4. Liquidity premiums and the impact of EMU

In the search for liquidity premiums in bond pricing, care must be taken to control for other determinants of bond value. Previous researchers have used a variety

of methods to isolate the value impacts of liquidity on bond pricing. For US bond

markets, Amihud and Mendelson (1991), Kamara (1994) and Strebulaev (2001) have

used the yield spread between a bill and a bond with similar term to maturity as the

appropriate variable to be explained. Warga (1992) uses the mean return difference

between a portfolio of seasoned bonds and a portfolio of the most recently issued

securities with similar duration. Goldreich et al. (2005) study on-the-run versus

off-the-run yield spreads adjusted for coupon and yield curve effects. Dı́az and Skinner (2001) use the differences between the yield-to-maturity of a bond and its theoretical yield as given by an explicit term structure model. Fleming (2001) also

examines a yield spread calculated as the difference between the observed yield of

17

The point estimate of b5 for the 3-year note sector is greater than 1.0 in each subsample. Given the

other parameter estimates, this value implies that a 3-year bondÕs market share would be greater than

100% if bond age were extrapolated over horizons greater than 4 years. Of course, original issue 3-year

bonds would be ‘‘dead’’ by this time. Moreover, in either subsample, the hypothesis that b5 = 1.0 cannot

be rejected at standard significance levels and, if we impose the constraint that b5 = 1.0, the re-estimated

values of b1 through b4 are very close to the original values.

18

Specifically, the two standard error bounds do not overlap in four of five parameter cases for the 10year; one of five for the 5-year; and two of five for the 3-year.

�1322

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

the on-the-run security and that predicted by a term structure model estimated with

off-the-run bond prices. He finds that this yield differential is consistently correlated

with a number of other liquidity proxies widely used in the literature.

We begin our study of the yield impact of liquidity by estimating a daily term

structure of interest rates using actual mean daily MDPA Treasury transactions

prices. We include all the spot transactions that took place with Treasury bills

and bonds during the day for all issues with a daily trading volume of at least than

€3 million (500 million pesetas) and terms to maturity between 15 days and 15 years.

We also include the one-week general collateral repo market interest rate to provide

a liquid point at the very front of yield curve. We employ Nelson and SiegelÕs (1987)

exponential model to fit the daily term structures. These daily term structure estimates do not incorporate any specific liquidity effects. Thus, the theoretical values

for all bonds generated from these estimations are those produced by discounting

coupon and principal payments according to fitted term structures that reflect an

average liquidity level. The differences between actual bond yields and the theoretical ones can be understood as a liquidity effect plus an error term due to other

factors.

4.1. Liquidity value versus current and expected future market share and auction status

As recently emphasized by Goldreich et al. (2005), the price of a security depends

on the flow of liquidity services generated over its entire life. Lifetime liquidity involves not only a securityÕs current of liquidity, but also the expected future path

of liquidity. We continue to use a bondÕs share of trading volume as the relevant

index of liquidity. Conveniently, the liquidity function of the previous section relates

a bondÕs market share of trading volume to bond age, a deterministic variable. Thus,

at any point in time, this function can be used to project the future path of liquidity

of any individual bond. In turn, this approach permits identification of both current

and expected future lifetime liquidity, and subsequently allows analysis of their separate impacts on bond valuation.

Specifically, we define Et[MSi,t+j] as the week t conditional expectation of the market share of bond i during some future week t + j. Using Eq. (1), Et[MSi,t+j] can be

expressed as

^ expb�b

^ ðAge

^ 2

^ ^Agei;tþj .

Et ½MSi;tþj � ¼ b

1

2

i;tþj � b3 Þ c þ b4 � b5

ð2Þ

Furthermore, we define MSi;t;tþmit as the average lifetime expected market share

for bond i from week t+1 through maturity week t + mit

mit

�

�

1 X

MSi;t;tþmit ¼

Et MSi;tþj ;

ð3Þ

mit j¼1

where mit is the number of weeks remaining until maturity for bond i as of the current week t.

We invoke rational expectations on the part of investors and interpret equation

(3) to incorporate the expected future market share function (2). Furthermore, based

�1323

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

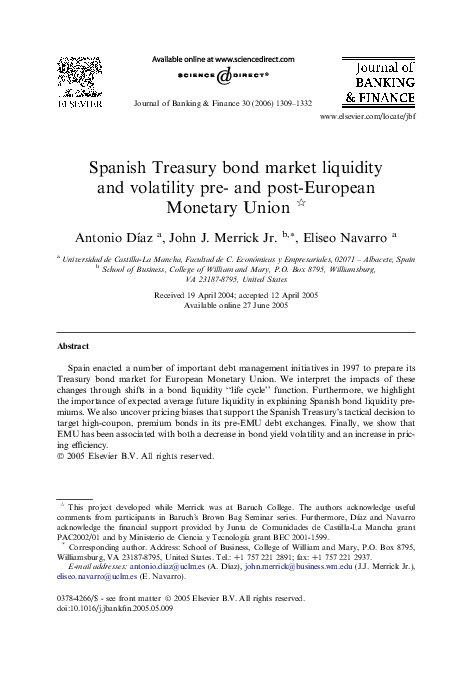

Market share of trading volume (%)

30

Current MS (1998–2002)

25

20

Current MS (1993–1997)

15

Avg. MS to maturity (1993–1997)

10

Avg. MS to maturity (1998–2002)

5

0

0.0

0.6 1.2 1.8 2.5 3.1 3.7 4.3 4.9 5.5 6.2 6.8

Bond Age (years)

7.4 8.0

8.6 9.2

9.8

Fig. 1. Average expected market share to maturity versus current market share for 10-years bonds based

upon parameter estimates for the market share equations reported in Table 3.

on the evidence of a regime shift in 1997, we match the appropriate set of parameters

for the market share function from each subsample presented in Table 3 to generate

the corresponding MSi;t;tþmit for that same subsample for use in our valuation equations below. In the spirit of a rational expectations model, this choice presumes that

investors understood the nature and consequences of the shifts in SpainÕs debt management policies at the time they were publicly announced in 1997. Fig. 1 provides

some insight into the MSi;t;tþmit variable for a newly issued 10-year-to-maturity bond.

Fig. 1 plots two fitted series from the market share regressions for Eq. (1) generated

using the parameter estimates for both the 1993–1997 and 1998–2002 sample periods. These series correspond to Et[MSi,t+j] of Eq. (2) for each subsample. Fig. 1 also

plots the expected market share to maturity variable (i.e., MSi;t;tþmit ) generated for

each subsample by Eq. (3) using the corresponding Et[MSi,t+j] profile. For each subsample, note the clearly defined differences between a 10-year bondÕs current market

share and its average expected future market share to maturity, especially over the

first year after initial issuance.

Table 4 presents estimates of the following regressions for weekly data in both of

our subsamples for 10-year sector issues with at least one year still remaining until

maturity:

Y dit ¼ /0 þ c1 OTRDoit þ /1 MSoit þ /2 MSi;t;tþmit þ mit ;

Y dit

¼ /0 þ

c2 PreBDoit

þ

c3 BDoit

þ

/1 MSoit

Y dit ¼ /0 þ /1 MSoit þ /2 MSi;t;tþmit þ mit ;

þ /2 MSi;t;tþmit þ mit ;

ð4Þ

ð5Þ

ð6Þ

where Y dit is the weekly average of daily differences between the actual and theoretical

yields to maturity of bond i during week t; MSi;t;tþmit is defined as above; MSoit is an

�1324

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

Table 4

Liquidity value impacts of current 10-year bond market share (MSoit ) and expected average future market

share (MSi;t;tþmit ) with and without on-the-run auction status (OTRDoit ), pre-benchmark status (PreBDoit )

and benchmark status (BDoit ) dummy variables

Sample period: 1993–1997

Sample period: 1998–2002

2

Coefficients

t-Statistics

Adjusted R (%)

Coefficients

t-Statistics

Adjusted R2 (%)

Constant

OTRDit

MSit

MSi;t;tþmit

3.08

�6.77

0.00

�1.86

(15.90)

(�12.33)

(�0.10)

(�12.24)

20.43

3.12

�0.18

�0.06

�2.30

(30.29)

(�0.50)

(�7.22)

(�25.87)

24.94

Constant

PreBDit

BDit

MSit

MSi;t;tþmit

3.08

�8.39

�5.81

0.00

�1.86

(16.45)

(�9.66)

(�7.60)

(�0.09)

(�12.22)

18.76

3.12

�1.79

0.87

�0.06

�2.30

(30.36)

(�2.50)

(1.69)

(�6.81)

(�26.21)

25.42

Constant

MSit

MSi;t;tþmit

3.08

0.00

�1.86

(13.89)

(�0.09)

(�11.01)

9.71

3.12

�0.06

�2.30

(30.28)

(�7.17)

(�25.80)

24.96

OLS regressions of the week t average difference between the actual and Nelson–Siegel theoretical yields to

maturity for bond i (Y dit ) on the various defined variables for two sample periods: 1993–1997 and 1998–

2002. The regression equations are

Y dit ¼ /0 þ c1 OTRDoit þ /1 MSoit þ /2 MSi;t;tþmit þ mit ;

ð4Þ

Y dit ¼ /0 þ c2 PreBDoit þ c3 BDoit þ /1 MSoit þ /2 MSi;t;tþmit þ mit ;

ð5Þ

Y dit ¼ /0 þ /1 MSoit þ /2 MSi;t;tþmit þ mit .

ð6Þ

Newey–West adjusted t-statistics are in parentheses and o superscript indicates an orthogonalized variable.

orthogonalized version of MSit;19 OTRDoit is an orthogonalized version of a dummy

variable set equal to 1.0 if bond i is the current on-the-run issue and zero otherwise;

PreBDoit , is an orthogonalized version of dummy variable set equal to 1.0 if bond i is

currently in its pre-benchmark stage and zero otherwise; and BDoit is an orthogonalized version of dummy variable set equal to 1.0 if bond i is currently in its benchmark

stage and zero otherwise.20 These regressions explicitly distinguish between the contributions of the current versus expected future market share variables for relative

bond value and permit tests of the marginal contributions of these market share variables to both 2-stage and 3-stage auction status dummy variables. Orthogonalized

variables are used to control for the correlation among the candidate explanatory

Thus, MSoit in (4) through (6) is the residual eit from the regression MSit = a0 + a1 + MSi;t;tþmit + eit.

The OTRD0it variable is the residual eOTRDit from the regression OTRD i t = b 1 +

b2MSit + b3MSi;t;tþmit þ eOTRDit ; and the other two orthogonalized dummy variables are defined in

analogous fashion.

19

20

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1325

variables. We expect the signs of /1 and /2 to be negative: the larger a bondÕs market

share, the higher its liquidity, and so the lower its yield.

Table 4 reports estimates of regressions (4) through (6) for original issue 10-year

bonds. Here, incorporating the full explicit life cycle function adds significant explanatory power to the bond status dummies for most cases. Our results also reveal that

expected future liquidity is much more important – in both magnitude and statistical

significance – than current liquidity for explaining Spanish Treasury bond values.

These patterns are most easily seen in regression (6), where only the market share

variables appear. The explanatory power of Eq. (6) is quite high even though it excludes both forms of status dummy variables. However, note that in regressions (4)

and (5), the new market share variables do not completely eliminate the contribution

of the status dummy variables to overall explanatory power. Nevertheless, the contributions of the dummy variables are inconsistent across subsamples in sign and/or

significance. In contrast, the key MSi;t;tþmit variableÕs coefficient estimates are always

properly signed and highly significant.21

4.2. Impacts of other bond-specific characteristics

As discussed in Section 2, a key component of the Spanish TreasuryÕs preparations for European Monetary Union was a series of exchange auctions designed to

help quickly build large-sized benchmark issues. These exchange auctions replaced

seasoned premium, high-coupon issues with new market-coupon bonds. Targeting

premium, high-coupon issues as candidates for these exchanges would have been a

sensible choice if such bonds traded cheaply in the market because of tax or other

reasons. Here we investigate whether discounts and premiums from par had discernable impacts on Spanish Treasury bond pricing. We use Dit = Max(0, 100 � Vit) and

Pit = Max(0, Vit � 100) to measure bond discounts and premiums, respectively,

where Vit is the ‘‘clean’’ price of the ith bond. We also use C oit , an orthogonalized

measure of the coupon rate (CRit) of the ith bond, to pick up any coupon-related

21

For original issue 5-year bonds (results not shown here for space reasons), the explanatory power of

Eq. (6) is reasonably high even though it excludes both forms of status dummy variables. Again, expected

future market share has a significantly more powerful impact on liquidity value than does current market

share. In fact, in the first subsample, the current market share variable is wrongly signed and not

significantly different from zero. Again, the results for regressions (4) and (5) suggest that the new market

share variables do not completely eliminate the contribution of the status dummy variables to overall

explanatory power. For original issue 3-year bonds (not shown here), term structure deviations are harder

to explain using our set of liquidity proxies. At least for the 1993–1997, the impact of MSi;t;tþmit is properly

signed and highly significant. (However, the coefficient for current market share is perversely signed and

significant.) The results for the 1998–2002 subsample are disappointing since the overall explanatory

power is low and the coefficient on MSi;t;tþmit in all three specifications is wrongly signed, though not

statistically different from zero. The puzzles for the 3-year sector are not confined to the market share

variables. The traditional status dummy approach also leads to wrongly signed and insignificant

coefficients in the 1998–2002 subsample.

�1326

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

Table 5

Value impacts of bond characteristics on 10-year bonds: price discount versus par (Dit); price premium

versus par (Pit); coupon rate (C oit ); and strippable issue dummy variable (S oit )

Sample period: 1993–1997

Sample period: 1998–2002

Coefficients

t-Statistics

Adjusted

R2 (%)

Coefficients

t-Statistics

Adjusted

R2 (%)

Constant

OTRDit

MSit

MSi;t;tþmit

Couponi ðC oit Þ

Discountit (Dit)

Premiumit (Pit)

Strippableit ðS oit Þ

3.28

�6.30

�0.01

�0.99

1.04

�0.29

�0.05

(10.77)

(�11.97)

(�0.38)

(�4.68)

(9.80)

(�12.37)

(�3.90)

34.24

1.71

�0.36

�0.02

�1.52

0.18

�0.27

0.08

�0.04

(12.79)

(�0.85)

(�2.45)

(�19.02)

(2.47)

(�11.61)

(10.66)

(�0.19)

31.02

Constant

PreBDit

BDit

MSit

MSi;t;tþmit

Couponi ðC oit Þ

Discountit (Dit)

Premiumit (Pit)

Strippableit ðS oit Þ

3.47

�6.30

�3.47

0.00

�1.14

0.88

�0.29

�0.05

(10.57)

(�6.52)

(�4.84)

(�0.13)

(�5.35)

(9.20)

(�9.09)

(�3.85)

29.59

1.68

�2.17

�0.82

�0.02

�1.50

0.22

�0.26

0.08

0.01

(12.72)

(�3.17)

(�1.69)

(�2.41)

(�19.18)

(3.04)

(�11.43)

(10.59)

(0.02)

31.26

Constant

MSit

MSi;t;tþmit

Couponi ðC oit Þ

Discountit (Dit)

Premiumit (Pit)

Strippableit ðS oit Þ

3.89

0.00

�1.18

0.84

�0.37

�0.07

(11.79)

(0.24)

(�5.63)

(8.79)

(�12.36)

(�5.72)

25.68

1.73

�0.02

�1.53

0.17

�0.27

0.08

�0.02

(13.69)

(�2.50)

(�19.77)

(2.51)

(�12.88)

(10.70)

(�0.10)

31.03

OLS regressions of the week t average difference between the actual and Nelson–Siegel theoretical yields to

maturity for bond i (Y dit ) on the various defined variables for two sample periods: 1993–1997 and 1998–

2002. The regression equations are

Y dit ¼ /0 þ c1 OTRDoit þ /1 MSoit þ /2 MSi;t;tþmit þ w1 C oit þ w2 Dit þ w3 P it þ w4 S oit þ mit ;

Y dit ¼ /0 þ c2 PreBDoit þ c3 BDoit þ /1 MSoit þ /2 MSi;t;tþmit þ w1 C oit þ w2 Dit þ w3 P it þ w4 S oit þ mit ;

Y dit ¼ /0 þ /1 MSoit þ /2 MSi;t;tþmit þ w1 C oit þ w2 Dit þ w3 P it þ w4 S oit þ mit .

Newey–West adjusted t-statistics are in parentheses. The o superscript indicates an orthogonalized variable. (See notes to Table 4 for additional variable definitions.)

effects not captured by Dit and Pit.22 Finally, the introduction of the Spanish strips

market in January 1998 may have caused strippable bonds to trade at higher values

than non-strippable issues. To investigate whether strip-related effects on value exist,

we define the dummy variable Sit equal to +1 if the ith bond is strip market eligible

22

Thus, C oit is the residual eCit from the regression CRit ¼ c0 þ c1 Dit þ c2 P it þ eC it .

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1327

and zero otherwise. We include S oit , an orthogonalized measure of the strip eligibility

dummy variable for the ith bond, in the 1998–2002 sample period regressions.23

Table 5 reports estimates of the following regressions for 10-year sector bonds in

each of our subsamples:

Y dit ¼ /0 þ c1 OTRDoit þ /1 MSoit þ /2 MSi;t;tþmit þ w1 C oit þ w2 Dit þ w3 P it

þ w4 S oit þ mit ;

ð7Þ

Y dit ¼ /0 þ c2 PreBDoit þ c3 BDoit þ /1 MSoit þ /2 MSi;t;tþmit þ w1 C oit þ w2 Dit

þ w3 P it þ w4 S oit þ mit ;

Y dit ¼ /0 þ /1 MSoit þ /2 MSi;t;tþmit þ w1 C oit þ w2 Dit þ w3 P it þ w4 S oit þ mit .

ð8Þ

ð9Þ

Generally, the results point to statistically significant differences in the valuation

of discount versus premium bonds. Note especially the results for the 1993–1997

sample period that reflect the recent experience observed by the Spanish Treasury

at the time of its exchange auction decision-making. The Dit variable is highly significant and indicates that investors favored bonds priced below par. Surprisingly, the

coefficient for Pit is negative and significantly different from zero; but it is small in

magnitude (about one-sixth the size of the coefficient on Dit). The coefficient on

C oit is positive and highly significant, indicating an additional pricing bias against

high-coupon bonds. These results confirm that discount bonds were favored over

high-coupon, premium bonds.24 Thus, the estimates lend support to the Spanish

TreasuryÕs decision to target high-coupon, premium bonds in its debt exchanges.

Moreover, some changes in the magnitude, sign and significance of the Dit, Pit and

C oit variables from the 1993–1997 sample to the 1998–2002 sample are quite interesting. For the 10-year bonds, both the magnitude and significance of the C oit fall precipitously, and the impact of Pit, while turning positive, remains small in

magnitude.25 These patterns may indicate that market impacts of such bond-specific

characteristics on value in the Spanish market have decreased since European Monetary Union ushered in a broader class of euro-based fixed income investors.26

23

Thus, S oit is the residual eS it from the regression S it ¼ d 0 þ d 1 Dit þ d 2 P it þ eS it .

The results for the 5-year bond sector for this same 1993–1997 sample period reveal investor biases

favoring discount bonds over high-coupon, premium bonds. Here, the estimated coefficients on the Dit and

C oit variables are each statistically significant. The Pit variable is statistically insignificant. In the 1993–1997

sample, the results for the 3-year bond sector show that investors favored discount bonds (i.e., a

statistically significant negative impact for Dit on bond yields) versus high-coupon, premium bonds (both

C oit and Pit have statistically significant positive slope coefficients).

25

For the 5-year bonds, the coefficients on the Dit, and C oit variables switch signs and lose some

significance. For 3-year bonds, the Dit variableÕs effect switches sign. Finally, for 3-year bonds, the

estimated coefficient on S oit is both negatively signed and statistically significant, indicating a value

premium for the strip feature. Evidence on the impact of the strip feature in the other sectors is mixed. The

S oit variable is marginally significant for 5-year bonds and statistically insignificant for 10-year bonds.

26

Recall from Section 2 that bond trades for non-residents and institutional investors have been settled

free of withholding tax for since 1999.

24

�1328

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

4.3. The impact of EMU on Spanish bond market volatility

Table 6 presents an expanded analysis of European Monetary UnionÕs effects on

Spanish bond market pricing along two distinct dimensions regarding market volatility. We first quantify the impact of European Monetary Union on Spanish bond

market yield volatility. Clearly, one major projected benefit for Spain under EMU

was to be a dampening of market yield volatility in light of the elimination of currency crisis risk from bond pricing. Our sample of daily fitted term structures provides a particularly clean way in which to measure the volatility impact of EMU

at different points along the zero coupon yield curve. Specifically, we create a daily

time series of fitted zero coupon bond yields for annual maturities between 2 and 10

years. We then compute subsample means and standard deviations of these yield series and test for equality of yield variances across the two subsamples. While European Monetary Union actually officially began on January 1, 1999, market

participants are widely viewed to have priced this merger as a fait accomplie before

this date. We have kept the same two sample splits used before, interpreting that the

market had fully priced in SpainÕs entry into EMU 1 year ahead of schedule.27

Panel A of Table 6 presents our yield volatility results based upon daily data for

the 1993–1997 and 1998–2002 sample periods. The columns report estimated sample

means and standard deviations of both yield levels (expressed in percentage points)

and first-differences in yields. A profound downward shift in average yield levels and

standard deviations across the zero coupon yield curve can be observed in the latter

periods. Formal tests based upon the first-differenced data confirm that the hypothesis of equal variances in the 1993–1997 and 1998–2002 periods is easily rejected for

all terms to maturity.28 For example, the standard deviation of yield first-differences

for 5-year zero coupon bonds nearly halved. Clearly, as was anticipated by the planÕs

early proponents, European Monetary Union has led to a dramatic fall in Spanish

bond market yield volatility.

Our second volatility investigation examines whether European Monetary Union

has led to more efficient relative pricing. We gauge relative pricing efficiency through

the residual variance of the Spanish bond yield regression equation (8). In particular,

we examine the residuals from the estimated Y dit regressions (8) of Table 5 and test for

equality of residual variances across the two subsamples. The null hypothesis is that

the residual variances from the Y dit regressions (8) in the 1993–1997 and 1998–2002

subsamples are equal. We interpret this null hypothesis to mean that European Mon-

27

On March 25, 1998, the European Commission had recommended that 11 countries – Austria,

Belgium, Finland, France, Germany, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain –

met the necessary conditions to adopt the single currency. On May 2, 1998, EU finance ministers officially

announced the bilateral parities between the currencies of the euro zone. Of course, reasonable arguments

exist for dating the sample split even before the start of 1998. The convergence of forward deposit interest

rates between Spain and Germany was nearly complete by mid-1997.

28

Identical inferences come from other versions of tests for equality of variances in two samples (e.g., the

standard F-test, BartlettÕs test, Siegel–TukeyÕs test and LeveneÕs test).

�Table 6

Impacts of European Monetary Union on Spanish Treasury market yield volatility and bond relative pricing efficiency

Tests of equality of variances in the two sample periods for first-differences of daily fitted zero

coupon yields

Term

Panel A

2

3

4

5

6

7

8

9

10

First sample

period: 1993–1997

Second sample

period: 1998–2002

First sample

period: 1993–1997

Second sample period:

1998–2002

Mean

Standard

deviation

Mean

Standard

deviation

Mean · 102

Standard

deviation

Mean · 102

Standard

deviation

7.72

7.90

8.09

8.26

8.39

8.50

8.59

8.66

8.72

2.68

2.69

2.67

2.63

2.59

2.54

2.49

2.45

2.40

4.03

4.24

4.43

4.60

4.75

4.88

4.99

5.09

5.17

0.68

0.64

0.60

0.57

0.53

0.50

0.48

0.45

0.44

�0.74

�0.70

�0.67

�0.64

�0.61

�0.58

�0.56

�0.55

�0.53

0.0859

0.0819

0.0807

0.0816

0.0811

0.0787

0.0760

0.0755

0.0797

�0.14

�0.13

�0.13

�0.13

�0.13

�0.13

�0.14

�0.14

�0.14

0.0500

0.0424

0.0437

0.0444

0.0440

0.0430

0.0421

0.0422

0.0437

Test for equality of variances

Brown–Forsythe prob > F

0.000

0.000

0.000

0.000

0.000

0.000

0.000

0.000

0.000

Sample meansa and standard deviations for residualsfrom Y dlt regression estimates of

Eq. (8) of Table 5

Tests of equality of variances in the two sample periods

for residuals from Y dit regression estimates of Eq. (8) of Table 5

Original issue

maturity sector (years)

Brown–Forsythe prob > F

Panel B

10

5

3

a

First sample

period: 1993–1997

Second sample

period: 1998–2002

Mean · 102

Standard

deviation

Mean · 102

Standard

deviation

0.000

0.000

0.000

0.035

0.060

0.072

0.000

0.000

0.000

0.031

0.034

0.034

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

Sample means and standard deviations for levels of fitted

zero coupon yields (in %)

0.000

0.000

0.000

Regression residual sample means equal 0 by construction.

1329

�1330

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

etary Union had no detectable impact on the dispersion of term structure arbitrage

trading opportunities in the Spanish market. For each of the three original issue

maturity sectors, Panel B of Table 6 presents tests of equality of residual variances

from the Y dit regressions (8) in the 1993–1997 and 1998–2002 subsamples. The valuation equation residuals have lower estimated standard deviations in the latter period. The test statistics have p-values that indicate strong rejections of the null

hypothesis of equal residual variances. We interpret these results as evidence that

the new class of euro-based investors created under European Monetary Union

has significantly increased pricing efficiency in the Spanish bond market.29

5. Summary and conclusions

This paper has examined liquidity and volatility in the Spanish Treasury bond

market in the context of debt policy shifts engineered by the Spanish government

in preparation for entrance into European Monetary Union. Empirically detectable

impacts of SpainÕs mid-1997 debt management initiatives exist for both trading activity and debt market valuation. We interpret these impacts through shifts in the coefficients of a liquidity life cycle model relating individual Treasury bond market share

to a bondÕs age (the time since its initial auction). Test for shifts in this market share

function as a result of the TreasuryÕs debt policy innovations clearly reject the

hypothesis of no structural change in the post-initiatives sample period.

We also estimate the structure of liquidity premiums in the different maturity sectors within the Spanish bond market. We investigate liquidity effects within a framework that values the lifetime flow of liquidity services and distinguishes between a

securityÕs current liquidity and its average expected future liquidity. Our empirical results for 10- and 5-year Spanish Treasury bond sectors reveal statistically significant

valuation impacts of expected future liquidity on current market value. Our expected

future liquidity measure adds significant explanatory power to the traditional auction status dummy variable approach to assessing bond liquidity value.

Our results for data from 1993 to 1997 detect statistically significant pricing biases

confirming that discount bonds were favored over high coupon, premium bonds.

These results lend support to the Spanish TreasuryÕs tactical decision to target

high-coupon, premium bonds in its pre-EMU debt exchanges.

Finally, we examine the impacts of European Monetary Union on volatility of

yields in the Spanish Treasury market. First, we use our basic fitted term structures

to show that the standard deviation of zero coupon bond yields declined dramatically after the market began pricing European Monetary Union as certain to occur.

Formal tests based on the first-differences of yields strongly reject the null hypothesis

of no change in variance from the pre-EMU period. Such an impact on volatility is

29

Changes in the Spanish tax regime beginning in 1999 (e.g., newly-issued Treasuries began trading free

of withholding tax for domestic institutions) may also have helped increase pricing efficiency.

�A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

1331

generally acknowledged (and had been forecasted by EMUÕs early supporters). It is

less widely recognized that European Monetary Union has also led to more efficient

relative pricing in the Spanish Treasury bond market. Our results reveal that the

residual variance of our liquidity and bond characteristic-augmented yield regressions fell sharply between our pre-EMU and post-EMU samples. Such improved

pricing efficiency may be attributed to an important byproduct of European Monetary Union: the creation of a much larger universe of euro-based fixed income investors willing to focus attention on trading opportunities in Spain.

References

Alonso, F., Blanco, R., del Rı́o, A., Sanchis, A., 2004. Estimating liquidity premia in the Spanish

government securities market. European Journal of Finance 10 (6), 453–474.

Amihud, Y., Mendelson, H., 1991. Liquidity, maturity, and the yields on US Treasury securities. Journal

of Finance 46 (4), 1411–1425.

Carayannopoulos, P., 1996. A seasoning process in the US Treasury bond market: The curious case of

newly issued ten-year notes. Financial Analysts Journal 52 (1), 48–55.

Chakravarty, S., Sarkar, A., 1999. Liquidity in US fixed income markets: A comparison of the bid–ask

spread in corporate, government and municipal bond markets. Working paper, Federal Reserve Bank

of New York.

Chen, L., Wei, J., 2001. An indirect estimate of transaction costs for corporate bonds. Working Paper,

University of Toronto.

Codogno, L., Favero, C., Missale, A., 2003. Yield spreads on EMU government bonds. Economic Policy

18, 503–532.

Dı́az, A., Navarro, E., 2002. La prima de liquidez en la Deuda del Estado española. Revista de Economı́a

Aplicada (10), 23–58.

Dı́az, A., Skinner, F.S., 2001. Estimating corporate yield curves. The Journal of Fixed Income 11 (2), 95–

103.

Duffee, G.R., 1998. The relation between Treasury yields and corporate bond yield spreads. Journal of

Finance 53 (6), 2225–2241.

Elton, E.J., Green, T.C., 1998. Tax and liquidity effects in pricing government bonds. Journal of Finance

53 (5), 1533–1562.

Fisher, L., 1959. Determinants of risk premiums of corporate bonds. Journal of Political Economy 67 (3),

217–237.

Fleming, M.J., 2001. Measuring Treasury market liquidity. Working Paper, Federal Reserve Bank of New

York, June.

Fleming, M.J., Remolona, E.M., 1999. Price formation and liquidity in the US Treasury market: The

response to public information. Journal of Finance 54 (5), 1901–1915.

Fridson, M.S., Jónsson, J.G., 1995. Spread versus Treasuries and the riskiness of high-yield bonds. Journal

of Fixed Income 5 (2), 79–88.

Goldreich, D., Hanke, B., Nath, P., 2005. The price of future liquidity: Time-varying liquidity in the US

Treasury market. Review of Finance 9 (1), 1–32.

Gwilym, O., Trevino, L., Thomas, S., 2002. Bid–ask spreads and the liquidity of international bonds.

Journal of Fixed Income, 82–91.

Heligman, L., Pollard, J.H., 1980. The age pattern of mortality. Journal of the Institute of Actuaries (107),

49–80.

Hong, G., Warga, A., 2000. An empirical study of bond market transactions. Financial Analyst Journal 56

(2), 32–46.

Houweling, P., Mentink, A., Vorst, T., 2002. Is liquidity reflected in bond yields? Evidence from the Euro

corporate bond market. Working Paper, Erasmus University, Rotterdam, April.

�1332

A. Dı́az et al. / Journal of Banking & Finance 30 (2006) 1309–1332

International Monetary Fund and World Bank, 2001. Guidelines for Public Debt Management.

Kamara, A., 1994. Liquidity, taxes, and short-term Treasury yields. Journal of Financial and Quantitative

Analysis 29 (3), 403–417.

Krishnamurthy, A., 2002. The bond/old-bond spread. Journal of Financial Economics 66, 463–506.

Nelson, C., Siegel, A., 1987. Parsimonious modeling of yield curves. Journal of Business 60, 473–489.

Sarig, O., Warga, A., 1989. Bond price data and bond market liquidity. Journal of Financial and

Quantitative Analysis 24 (3), 367–378.

Schmidt, P., Sickles, R., 1977. Some further evidence on the use of the Chow test under heteroskedasticity.

Econometrica 45, 1293–1298.

Shen, P., Starr, R.M., 1998. Liquidity of the Treasury bill market and the term structure of interest rates.

Journal of Economics and Business 50 (5), 401–417.

Shulman, J., Bayless, M., Price, K., 1993. Marketability and default influences on the yield premia of

speculative-grade debt. Financial Management (Autumn), 132–141.

Strebulaev, I.A., 2001. Many faces of liquidity and asset pricing: Evidence from the US Treasury securities

market. Working Paper, London Business School, February.

Warga, A., 1992. Bond returns, liquidity, and missing data. Journal of Financial and Quantitative

Analysis 27 (4), 605–617.

�

Antonio Díaz

Antonio Díaz