International Journal of Advanced Engineering Research and

Science (IJAERS)

Peer-Reviewed Journal

ISSN: 2349-6495(P) | 2456-1908(O)

Vol-10, Issue-10; Oct, 2023

Journal Home Page Available: https://ijaers.com/

Article DOI:https://dx.doi.org/10.22161/ijaers.1010.12

Evaluating the Dynamics of Capital Structure, Corporate

Governance, and Bank Performance: A Case Study of

Listed Banks in Ghana

Winnifred Coleman

School of Finance, Zhongnan University of Economics and Law, Wuhan, P.R. China

Received: 07 Sep 2023,

Receive in revised form: 10 Oct 2023,

Accepted: 17 Oct 2023,

Available online: 26 Oct 2023

©2023 The Author(s). Published by AI

Publication. This is an open access article

under the CC BY license

(https://creativecommons.org/licenses/by/4.0/).

Keywords— Capital structure, corporate

governance, Bank performance, Ghana.

I.

Abstract— This study explores the interconnections among capital structure,

corporate governance, and bank performance in listed banking institutions

in Ghana, utilizing a comprehensive scorecard approach to assess corporate

governance compliance. We identify a bi-causal link between corporate

governance and stock returns, indicating that changes in corporate

governance practices lead to subsequent fluctuations in stock returns. As

stock returns rise, banks can attract more investors, reducing their debt and

leverage (debt to equity ratio) ratios. Regarding capital structure and bank

performance, we find no evidence supporting the notion that the equity ratio

causes changes in stock returns, but a causal relationship exists in the

opposite direction. Stock returns impact the proportion of total assets

attributed to equity, as higher returns attract investors, facilitating bank

expansion through new share issuance. Furthermore, we detect a bidirectional causality between stock returns and the debt ratio. Lastly, we

observe a unidirectional causality where the debt to equity ratio does not

cause changes in stock returns, but stock returns influence the debt to equity

ratio. Rising stock returns enhance equity value, prompting banks to

increase equity at the expense of debt, thus boosting operational funding

through retained earnings. These findings illuminate the complex

relationships between capital structure, corporate governance, and bank

performance, offering valuable insights for financial practitioners and

policymakers.

INTRODUCTION

In recent years, the global economy has witnessed

significant transformations, marked by events such as the

2008 financial crisis and subsequent credit crunch (BlascoMartel, Y., Cuevas, J., & Riera-Prunera, 2023). These events

have sparked a surge in academic and research interest in

the banking industry worldwide. The effects of these global

shifts have reverberated through the African banking sector,

driven by the increasing interconnectedness of global

financial systems (Allam, Bibri & Sharpe, 2022). African

banks, particularly those in Ghana, have found themselves

deeply influenced by the evolving landscape of banking

services on a global scale (Ahmed & Rehman, 2008).

www.ijaers.com

Despite these challenges, banks continue to earn

commendation for their profitability, extensive branch

networks, and outstanding customer service (Lottu et

al.,2023). Central to a bank's mission is the accumulation of

surplus capital and its effective deployment to areas of the

economy facing deficits, achieved through lending and

saving operations, primarily driven by customer deposits.

Larger banks, in particular, are assumed to wield more

financial influence due to their ability to engage in extensive

lending and saving operations. However, the banking

industry has undergone substantial transformations in its

financial and monetary environment, coupled with

technological advancements, leading to heightened

Page | 125

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

competition among banks (Spathis et al., 2002; Bisht et al.,

2022). As financial intermediaries, banks are entrusted with

the critical role of ensuring the efficient flow of capital to

sectors of the economy in need. Despite the presence of

other financial institutions in the intermediation process,

banks are widely regarded as the most pivotal.

In the Ghanaian context, the banking sector presents

substantial financial opportunities despite fierce

competition (Ghana Banking Survey, 2009; Boadi &

Osarfo, 2019). However, these opportunities are

accompanied by inherent risks, including credit, market,

and operational risks, which banks must navigate to

maintain their competitive edge (Amidu, 2007).

Consequently, banks must devise innovative strategies to

determine the adequate capital reserves required to mitigate

unexpected losses stemming from these risk exposures. The

importance of capital in ensuring the stability and longevity

of banks in this dynamic landscape cannot be overstated.

The definition of banks varies from one nation to

another, encompassing a range of functions and services.

The banking sector is regulated and overseen by the Bank

of Ghana, serving as the central bank. Reforms aimed at

fostering competition, attracting foreign investment,

enhancing operational efficiency, and promoting electronic

banking services have liberalized Ghana's banking sector.

As a result, the industry has witnessed increased

competition and the adoption of robust business practices,

cutting-edge technology, and advanced risk management

systems.

In addition to the 31 universal banks, including those

with foreign ownership, Ghana's banking sector

encompasses rural and community banks, as well as nonbanking financial institutions such as savings and loan

associations, leasing companies, finance firms, and

mortgage lenders. This diverse landscape reflects the

evolving and dynamic nature of the banking industry in

Ghana, poised to meet the challenges and opportunities of

the future.

The choice between debt and equity capital represents a

pivotal financial decision for businesses, including banks

(Glen and Pinto, 1994; Park, 2022). To make this choice

effectively, managers must grasp how capital structure

impacts performance, as profitable banks meticulously

consider their financing options to remain competitive. This

choice varies across economies due to country-specific

factors (Bos and Fetherston, 1993; Omete, 2023). This

understanding underscores the importance of exploring the

relationship between capital structure and bank

performance in the Ghanaian banking sector, which has

received limited attention in the existing literature.

www.ijaers.com

Amidu (2007) pioneered the examination of Ghanaian

banks' capital structure determinants. Recent developments,

such as the 2017-2018 banking crisis in Ghana, wherein the

central bank allowed private entities to take over indigenous

banks through mergers and acquisitions, alongside the entry

of international players like First National Bank and

Republic Bank, have reshaped the competitive landscape.

Liberal banking laws have also permitted international

banks, including Citibank N.A. and Bank of Beirut, to

establish a presence in Ghana. The perception of sustainable

growth, transparent legislation, competent regulation, and

political stability serve as key drivers of investment in the

Ghanaian banking sector.

Corporate governance, although has a universal goal,

varies across nations due to unique systems influenced by

socioeconomic, legal, political, and cultural factors (Huynh

et al., 2022; Nobanee & Ellili, 2022; Borgia, 2005; Okike,

2007). Despite these variations, its core objective remains

consistent: to govern the actions of a company's various

members. The OECD (1999) defines corporate governance

as the system managing and governing commercial

businesses, prescribing decision-making processes, rights

and obligations distribution among stakeholders, and

performance evaluations (El-Chaarani et al., 2022; Molla et

al., 2023 ).

Although extensive research exists globally on the

relationship between capital structure, corporate

governance, and firm performance, there is a dearth of

literature on their interplay in the context of the Ghanaian

banking sector. Understanding this dynamic is crucial given

the sector's significance in the country's transition from an

agriculture-focused economy to a service sector-driven one

(Agwu et al., 2023; EconomyWatch.com, 2011). The recent

banking crisis in Ghana underscored the importance of

effective corporate governance, but the impact of these

practices on banks' performance remains context-specific.

Therefore, this study aims to investigate the causal

relationship between capital structure and stock return, as

well as the link between corporate governance and stock

returns, filling the research gap and shedding light on the

unique dynamics of Ghanaian banks in the service sector.

II. LITERATURE REVIEW

2.1 Corporate governance and Agency theory

The oversight and regulation of business operations in a

transparent manner has long been recognized as a crucial

aspect of corporate governance. The centrality of the agency

theory in the examination of corporate governance is

evident via the extensive referencing of research

publications. The research conducted by Ross (1973) and

later expanded upon by Jensen and Meckling (1976) has

Page | 126

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

suggested that the agency theory provides a suitable

framework for examining corporate governance. This

notion prompts us to contemplate the behavioural

tendencies of managers. The case of corporations that

provide their managers with variable remuneration based on

the growth of turnover might be cited. Similarly, it is

imperative to acknowledge that the effectiveness of internal

control and internal audit functions within organizations can

significantly contribute to enhancing the corporate

governance framework of those organizations. According to

Nyakundi et al. (2014) and Kumar et al. (2022) it serves as

a key factor in ensuring the effective operation of business

processes within a regulated setting, with the goal of

enhancing financial performance.

Effective

corporate

governance

entails

the

implementation of control and oversight procedures to

guarantee that managerial actions align with the optimal

interests of shareholders (Al-Zaqeb et al., 2022; Abdullah &

Tursoy, 2023). This may encompass the establishment of an

autonomous board of directors, remuneration of executives

tied to the company's success, financial transparency, and

dissemination of pertinent information to shareholders.

Corporate governance plays a pivotal role in mitigating

conflicts of interest and enhancing the financial

performance of a company by the implementation of

suitable incentives and controls. This, in turn, leads to an

augmentation in the firm's value and the return on

investment for its shareholders. Yermack (1996) conducted

a study to examine the significance of corporate governance

mechanisms and their influence on financial performance.

Additionally, Shleifer and Vishny (1997) conducted a

comprehensive evaluation of the current body of literature

to assess the status of research on corporate governance.

The researchers reached the conclusion that agency theory

serves as a significant conceptual framework for

comprehending the connection between corporate

governance and financial performance. Moreover, they

assert that it can be utilized to develop efficient governance

procedures for companies (Abdullah & Tursoy, 2023). Let

us contemplate a corporation that is listed on the stock

exchange, wherein the stakeholders own a vested interest in

the optimization of their share value. In contrast, the

objectives of the company's managers may diverge,

encompassing the maximization of personal income or the

preservation of their authority inside the organization. The

divergence of interests among stakeholders can result in

strategic decisions that may not align with the ideal

outcomes for the company or its shareholders. In the above

scenario, it is posited by agency theory that the

implementation of robust corporate governance

mechanisms can effectively harmonize the interests of

stakeholders and enhance the financial performance of the

www.ijaers.com

organization. One illustrative instance involves the

establishment of an autonomous and proficient board of

directors, which can effectively oversee the actions of

executives and formulate strategic choices that align with

the welfare of shareholders. In a similar vein, the provision

of incentives to executives, contingent upon the

performance of the company, can serve as a motivating

factor for exerting increased effort towards enhancing the

overall worth of the organization. In essence, agency theory

posits that the establishment of effective corporate

governance mechanisms is crucial to align the interests of

stakeholders and enhance the financial performance of the

firm. Through the implementation of suitable control and

oversight systems, corporate governance has the potential

to mitigate conflicts of interest and enhance shareholder

value.

2.2 Capital structure and bank performance

The discourse surrounding the capital structure of

enterprises originated with the seminal research conducted

by (Modigliani and Miller, 1958). The proponents initially

maintained the stance that the financial techniques

employed by a firm do not have an impact on the firm's

worth. However, this perspective underwent a shift in 1963

following subsequent investigations. The study determined

that altering the capital structure of a firm can effectively

enhance its value, although it is crucial to consider an

optimal blend of capital structure. The discourse

surrounding the most advantageous capital structure was

reinvigorated in 1984 by the introduction of the pecking

order theory. According to Myers and Majluf ,1984, this

theory posits that profitable firms tend to limit their reliance

on debt capital and instead prioritize the utilization of

domestically generated money.

The subsequent proposition known as the static trade-off

theory posits that organizations make decisions regarding

their target leverage ratios by considering the trade-off

between the advantages and disadvantages associated with

increasing their leverage (Opoku-Asante et al., 2022). In the

absence of adjustment costs, firms would consistently

counteract departures from their primary aim. Conversely,

in situations where significant adjustment costs are present,

it is probable that the duration of the adjustment process will

be significantly prolonged (Fama and French, 2002; Oanh

et al.,2023). Gleason et al., 2000 posited that organizations

could enhance their performance by strategically employing

varying proportions of debt and equity in their capital

structure, drawing primarily upon the static trade-off

concept.

When analysing the influence of capital structure on

firm performance, the extant finance literature identifies

two types of performance measures. These include the

Page | 127

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

conventional accounting measures of performance, such as

return on assets (ROA), return on equity (ROE), earnings

per share, and Tobin's Q. Additionally, there are profit

efficiency measures, such as frontier efficiency as proposed

by Berger and di Patti, 2002. Abu-Rub, 2012 employed

various performance indicators, including return on average

equity (ROE), return on average assets (ROA), earnings per

share, Tobin's Q, and the market value of equity to book

value of equity ratio, to examine the influence of capital

structure on firm performance. In addition to the impact of

capital structure on a company's success, Hansen and

Wernerfelt (1989) identified external and organizational

factors as key determinants of firm performance.

In a separate investigation, Hoffmann (2011) conducted

an analysis utilizing data from the United States banking

sector spanning a duration of 13 years. The objective of this

study was to explore the association between earnings and

capital within the industry. The findings revealed a negative

correlation between the ratio of equity to assets and bank

profitability. Additionally, a non-monotonic U-shaped

relationship was observed between these variables. This

statement suggests that the first adoption of leverage can

potentially lead to a reduction in agency costs and an

enhancement in firm performance. However, after a certain

point, further increases in leverage can raise the anticipated

costs associated with bankruptcy and financial distress

(Berger and di Patti, 2002). Additionally, Berger, 1995

conducted a study investigating the correlation between the

capital-to-assets ratio and bank profitability. The findings of

the study revealed a significant and positive association

between the capital-to-assets ratio and bank profitability.

This suggests that an increase in the capital-to-assets ratio

may result in reduced bankruptcy costs and lower interest

payments, which could potentially mitigate a substantial

portion of any decline in earnings.

2.3 Corporate governance and performance

In scholarly investigations that have incorporated

corporate governance as a primary variable, two principal

domains have been subject to examination. The primary

objective is to examine governance through the lens of

shareholder and capital structure considerations. The

secondary objective is to explore the composition of boards

of directors and enhance the effectiveness of governance

mechanisms to enhance financial performance. Several

studies have highlighted the significance of capital

structure, including the works of Khan et al. (2022);

Haralayya, B. (2022); McConnell and Servaes (1990),

Nesbitt (1994), Smith (1996), Del Guercio and Hawkins

(1999), and Hartzell and Starks (2003). These researchers

have observed a positive impact on management behaviour

resulting from the involvement of institutional shareholders.

www.ijaers.com

In the realm of board of directors' operations, notable

contributions have been made by Brickley et al. (1994) and

Lee et al. (1999), who have underscored the significance of

independent or external directors in enhancing the standard

of governance efficacy. Furthermore, Jensen (1993) has

demonstrated that the presence of multiple directorships

enhances the level of autonomy granted to directors,

enabling them to exert influence on the financial outcome.

Shleifer and Vishny (1997) propose that corporate

governance procedures serve to mitigate agency costs

arising from conflicts of interest among stakeholders inside

institutions. According to a later analysis by the OECD

advisory group in 2004, it was found that efficient corporate

governance has the potential to boost economic efficiency

and growth, while also improving investor trust. Moreover,

it leads to enhanced operational performance. According to

Claessens (2003), the adoption of corporate governance

practices also enhances institutions' access to external

financing, improves operational performance, and reduces

the cost of capital.

The current body of scholarly research pertaining to

Italian banks has primarily concentrated on the examination

of ownership structures, with a specific emphasis on the

efficiency disparities between publicly owned banks and

their privatized counterparts. In their study, Bianchi, Di

Battista, and Lusignani (1997) investigate the correlation

between various corporate governance measures and the

performance of banks. The researchers discover that private

banks consistently outperform publicly owned banks across

all evaluated criteria. De Bonis (1997) demonstrates that

publicly held banks exhibit inferior performance metrics,

even when eliminating the significantly distressed

institutions in the Southern region.

Multiple research investigations have identified

empirical data suggesting that private banks operating as

cooperative banks have superior management practices. In

the study conducted by Farabullini and Ferri (1997) about

the ex-ante probability of underperformance among banks

in the southern region, it was shown that cooperative banks

had a lower likelihood of bad performance. Within the realm

of publicly owned banks, savings banks are local

establishments that have predominantly fallen under the

jurisdiction of prominent banking foundations. The precise

role of these foundations remains a topic of ongoing

scholarly discourse. Furthermore, it has been observed that

the organizational structures of savings banks have

exhibited a greater resemblance to those commonly found

in public administration, as opposed to other banks that are

publicly held. The impact of the stock market on managerial

control is not definitively established: Bianchi, Di Battista,

and Lusignani (1997) observe limited evidence supporting

Page | 128

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

the notion that stock exchange listing leads to market

discipline. Due to the limited availability of comprehensive

data, there has been a relative neglect of alternative facets

pertaining to organizational structure and corporate

governance.

2.4 Hypothesis Development

Several research in Ghana have examined the

relationship between capital structure and performance,

yielding consistent findings. In a study conducted by Abor

(2005), the relationship between the capital structure and

performance of 22 firms listed on the Ghana Stock

Exchange (GSE) was examined. The findings revealed a

substantial positive correlation between short-term

indebtedness, as measured by the short-term debt-to-assets

ratio and return on average assets (ROAA). The researcher

also discovered a substantial negative link between

performance and long-term debt, as measured by the longterm debt-to-assets ratio. The results of this study align with

the findings of Hadlock and James (2002), which propose

that profitable enterprises tend to employ a greater amount

of short-term debt. In a separate investigation conducted by

Bokpin et al. (2010), it was observed that companies listed

on the Ghana Stock Exchange (GSE) tend to employ

significant amounts of loan capital, indicating a strong

inclination towards utilizing short-term debt as a means of

funding their business activities. However, Ghanaian listed

banks are limited when it comes to studies as such. It is for

this reason that this study seeks to address banks. To

discover if the results for listed firms are consistent

literature, we developed the following hypothesis:

H1: - There is a causal relationship between the equity

ratio and stock return.

H2: - There is a causal relationship between the debt

ratio and stock return.

H3: - There is a causal relationship between the debtto-equity ratio and stock return.

Corporate governance has garnered considerable

attention and experienced substantial development as a

significant instrument, particularly in recent decades. The

recent financial crises, rapid privatization growth, and the

presence of financial institutions have contributed to the

strengthening of corporate governance norms in various

institutions across different countries. Numerous studies

have demonstrated that effectively implemented corporate

governance procedures significantly contribute to

organizational performance. The implementation of

effective corporate governance practices is crucial for a firm

due to various reasons: According to the Organisation for

Economic Co-operation and Development OECD (2004),

the implementation of effective corporate governance

practices has been found to enhance the reputation of a

company, mitigate risks, and instil greater confidence

among shareholders. Moreover, the establishment of sound

corporate governance practices entails the implementation

of many cohesive processes, internal control systems, and

external settings that collectively enhance the overall

effectiveness of business enterprises, hence fostering

excellent corporate governance. The fundamental objective

of corporate governance is to enhance the performance of

companies by establishing and maintaining incentives that

motivate corporate managers to optimize the operational

efficiency, return on assets, and long-term growth of the

firm. This is achieved by implementing mechanisms that

restrict managers from misusing their authority over

corporate resources. For this reason, we test to find if there

exist a causal relationship between corporate governance

and stock returns as presented in our hypothesis four (4)

below:

H4: There is a causal relationship between corporate

governance and stock returns.

III.

DATA AND METHODOLOGY

This study utilized data of 11 listed Ghanaian banks

given the license to operate the business of banking in

Ghana over a period of fourteen years spanning from 2005

to 2019. The data was collected from the fact book of the

Ghana Stock Exchange.

The general form of the panel data model can be specified

more compactly as follows:

Yi ,t = + X i ,t + ei ,t

The subscript i representing the cross-sectional

dimension and t denoting the time-series dimension. The

lefthand variable Yi,t, represents the dependent variable in

the model and Xi,t contains the set of independent variables

in the estimation model, and is taken to be constant overtime

t and specific to the individual cross-sectional unit i. If α is

taken to be the same across units, ordinary least squares

(OLS) provide a consistent and efficient of α and β.

Researchers use multiple regression model to test the

impact of independent variables on dependent variable.

The following specification was thus adopted:

SRi ,t = 0 + 1ERi ,t + 2 DRi ,t + 3 DEi ,t + 4 M mt + 5 Ln _ TAi ,t + i ,t

www.ijaers.com

(1)

Page | 129

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

SR i,t total stock return i in period t andβ0, β1, β2, β3, β4

are model coefficients . ER i,t is the ratio of total equity to

total assets for firm i in period t. DR i,t is the ratio of long

term debt to total assets for firm i in period t . DE i,t is the

vector of macroeconomic variables (inflation and real GDP

per capita). Ln_TA is the log of Total Assets and i ,t is the

Error term.

ratio of debt to equity for firm i in period t and M m t is the

Table 1: Variables and Indicators

Concept

Capital Structure

Corporate Governance

Bank Performance

Variables

Equity ratio (ER)

Indicators

Total Equity/ Total Assets

Debt ratio (DR)

Total Debt/ Total Assets

Debt to Equity Ratio (DE)

Total Debt / Total Equity

Governance processes

Stock Return (SR)

Scorecard

(P1-P0) +D/P0

P1=Pending Stock Price

P0=Initial Stock Price

D= Dividend

Robust Checks

Controls

ROA

Net Income/Total Assets

ROE

Net Income/Stockholder’s Equity

TOBIN’S Q

Equity Market Value/Equity Book Value

Macroeconomic Variables

Inflation and GDP

Ln_TA

Firm size=log of Total Assets

The equity ratio is a financial indicator utilized to assess

the level of leverage employed by a company. The

evaluation of a company's debt management and asset

funding is determined by analysing its investments in assets

and the level of equity. A low equity ratio signifies that the

corporation predominantly relied on debt for asset

acquisition, a well-recognized indicator of heightened

financial risk. Companies that possess higher equity ratios

typically demonstrate adequate funding of their asset

requirements while minimizing the use of debt.

The debt ratio measures a company's debt-based

financing of assets, indicating its solvency. A high ratio

signifies significant debt reliance, raising lending risk for

creditors. Steady cash flows are essential to service debt,

particularly in competitive or rapidly evolving industries.

Oligopolistic or monopolistic firms may safely accumulate

debt with reliable cash flows. Investors use this ratio to

assess efficient debt utilization for business expansion. It

holds critical importance for both company management

and investors. The formula, as shown in Table 1.0,

computes total debt, consisting of short-term (due within 12

months) and long-term liabilities. Total assets encompass

all assets owned, including cash, marketable securities,

accounts receivable, and more, categorized as current or

www.ijaers.com

long-term assets. Total assets result from adding liabilities

and owner's equity.

The Debt-to-Equity ratio, also known as the "debtequity ratio," measures the proportion of total debt to

shareholders' equity. It reveals a company's capital structure

preference for debt or equity financing. A higher ratio

suggests leverage, favorable for stable, cash-rich firms but

not for declining ones. Conversely, a lower ratio indicates

less reliance on debt, nearing full equity financing. The

ideal ratio varies by industry. A stock market return refers

to the alteration in value, either positive or negative, of an

investment or asset as observed over a specific period. A

positive return signifies that a financial gain has been

achieved on the investment. A negative return signifies a

decline in the value of the investment, resulting in a

financial loss.

The Return on Assets (ROA) is a financial indicator

used to assess the profitability of a corporation by

comparing its net income to its total assets. The ratio serves

as a measure of a company's performance, as it compares

the net income it generates to the capital invested in its

assets. A positive correlation exists between the level of

return and the degree of productivity and efficiency

Page | 130

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

demonstrated by management in the allocation and

utilization of economic resources.

Return on Equity (ROE) assesses a company's

profitability relative to its shareholders' equity. It calculates

net income as a percentage of shareholders' equity, typically

presented as a percentage. For instance, a 7% ROE means

earning $7 for every $100 in shareholder equity. This

percentage reveals how efficiently a firm utilizes its capital

for profit generation. ROE can also gauge a company's selfsustaining growth potential, i.e., its ability to grow without

additional borrowing. Comparing a company's ROE to the

industry average can highlight its competitive advantage. A

consistent, increasing ROE suggests a firm effectively

reinvests earnings, enhancing productivity and gains.

Conversely, a declining ROE may signal management's

inefficiency in reinvesting capital. Companies surpassing

their industry's ROE average are often preferred choices for

investors.

collected data on corporate governance practices and

financial performance from secondary sources, specifically

annual reports provided by the Ghana Stock Exchange Fact

Book. These reports offer detailed insights into a firm's

activities and financial performance during the preceding

year, benefiting investors and stakeholders.

Lastly, a scorecard methodology, inspired by Ebenezer

Edward Arthur, evaluates corporate governance

implementation in Ghana's banks. Scorecards, per the

International Finance Corporation (IFC) in 2014,

quantitatively assess adherence to governance codes. These

tools gauge governance processes against predetermined

benchmarks, aiding market analysts, policymakers,

directors, shareholders, and others in assessing corporate

governance levels. Rankings or ratings can be derived from

scores to position a corporation relative to others. However,

the mere existence of a local governance code does not

guarantee improved practices. Adopted from private sector

investors, scorecards offer a means to identify areas for

performance enhancement in strategic planning, decisionmaking, risk management, controls, and organizational

structures, as per the IFC (2014)

The Q Ratio, also known as Tobin's Q Ratio, quantifies

the relationship between the market value and replacement

value of tangible assets. Developed by Nobel laureate James

Tobin, it hypothesizes that the aggregate market value of

listed corporations should approximate their replacement

costs. This ratio is useful for evaluating individual

IV. EMPIRICAL RESULTS AND DISCUSSION

companies and the overall stock market. To account for

Table 2 provides a summary of the descriptive statistics

potential size-related impacts on profitability in the banking

of the dependent and independent and control variables and

sector, we used the natural logarithm of total assets

shows the average indicators of variables computed from

(Ln_TA). Larger banks can offer a broader range of services

the financial statements. The mean equity of the banks is

and operate more efficiently, potentially boosting

0.21 which means around 21 per cent of the total assets

profitability. They can also access cost-effective borrowing

consists of equity. The average of debt ratio of 84 percent

opportunities, enhancing profitability. We also considered

suggests that 84% of banks assets are financed by debt.

the macroeconomic environment's impact on bank

Given a standard deviation of 6%, the table tells us that

profitability, factoring in variables like inflation and real

majority of the Ghanaian listed banks achieved this mean.

GDP per capita, which influence customer demand for

The mean Debt to equity ratio is 6.34 with standard

banking products and services. The study's population

deviation of 1.26 suggesting that majority of banks could

included all 11 banks listed on the Ghana Stock Exchange,

not attain the mean Debt-to equity ratio.

licensed and operating between 2005 and 2015. We

Table 2: Descriptive Statistics

Variables

Mean

Std. Dev.

Min

Max

Observations

ER

0.21

0.12

0.12

0.47

154

DR

0.84

0.06

0.72

0.90

154

DE

6.34

1.26

4.06

7.79

154

SR

0.09

0.25

0.06

0.14

154

Ln_TA

0.71

0.63

0.82

0.94

154

Mmt

0.54

0.23

0.54

0.89

154

4.1 Diagnostic tests

In the domain of statistical modelling and data analysis,

the presence of heteroscedastic errors introduces a

www.ijaers.com

captivating and intricate phenomenon. Heteroscedasticity,

often characterized as a departure from the

homoscedasticity assumption, adds layers of complexity

Page | 131

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

and nuance to our understanding of statistical relationships,

demanding careful consideration. Robust estimation

becomes imperative when there is a strong suspicion of

heteroscedasticity. The homoscedastic model assumes

constant error variance across all values of x, but in the real

world, variance may vary with x, aligning more accurately

with practical scenarios.

Another common scenario where robust estimation is

crucial is when dealing with data containing outliers. In the

presence of outliers originating from distinct datageneration processes, traditional least squares estimation

becomes inefficient and biased. Least squares predictions

are pulled towards outliers, inflating estimate variances, and

potentially obscuring the true impact of outliers. Although

least squares methods are considered robust in terms of not

increasing the type I error rate under model violations, they

often exhibit a lower type I error rate and a significant

increase in type II errors when outliers are present, a

phenomenon known as the conservatism of classical

methods. To evaluate the presence of heteroscedasticity, we

conducted a White Noise Test, with the results presented in

Figure 1. The absence of data flaws has led us to proceed

with robust regression, emphasizing the critical importance

of robust estimation in addressing the complexities

introduced by heteroscedastic errors.

Fig.1: Heteroscedasticity test

www.ijaers.com

Page | 132

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

The stationarity of variables in this study plays a critical

role in its behavior and characteristics. If two variables

exhibit trends over time, a regression of one on the other

may yield a high R2 even if they are unrelated. Furthermore,

if the variables in the regression model are not stationary, it

violates the standard assumptions for asymptotic analysis.

In such cases, the typical "t-ratios" will not follow a tdistribution, rendering hypothesis tests on regression

parameters invalid. To mitigate these issues, we conducted

an Augmented Dickey Fuller (ADF) test to ensure the

variables' stationarity. The ADF test results are presented in

Table 3. If the t-statistic exceeds the 5% critical value, we

reject the stationarity assumption. At the initial level, all our

variables have absolute t-statistics greater than the 5%

critical value (absolute value) of 3.000. Consequently, we

take a first difference. After differencing, only two variables

(equity ratio and debt-to-equity ratio) exhibit t-statistics

conforming to stationarity. Therefore, we proceed to take a

second difference for the remaining non-stationary

variables. At this stage, all our variables are stationary,

enabling us to move to the next step: investigating whether

these variables move together in the long run. To

accomplish this, we conducted a Johansen test for

cointegration, as detailed in Table 3.

Table 3: Unit Root Test using Augmented Dickey-Fuller Test

Variable

Test

Test statistics

Equity ratio

Level

-2.326

-3.00

N

1st diff

-3.971

-3.00

Y

Level

-1.851

-3.00

N

1st diff

-2.660

-3.00

N

2nd diff

-3.589

-3.00

Y

Level

-2.518

-3.00

N

1 diff

-3.364

-3.00

Y

Level

-1.834

-3.00

N

1 diff

-2.254

-3.00

N

2 diff

-3.574

-3.00

Y

Level

-1.450

-3.00

N

1 diff

-2.640

-3.00

N

2 diff

-5.742

-3.00

Y

Level

-2.813

-3.00

N

1st diff

-3.615

-3.00

Y

Level

-1.642

-3.00

N

1st diff

-4.283

-3.00

Y

Level

-0.695

3.00

N

1 diff

-3.999

3.00

Y

Level

-0.316

3.00

N

1st diff

-3.918

3.00

Y

Level

-3.168

3.0

Debt ratio

De ratio

st

Corporate

Governance

st

nd

Stock return

st

nd

Ln_TA

Mmt

ROA

st

TOBIN’S

Q

5% Critical Value

Conclusion

Y

NOTES: 1% critical value of -3.750 and 10% critical value of -2.630. In the conclusion, N indicates non- stationery and Y

indicates stationary.

Once variables have been classified as integrated of

order I (0), I (1), I(2) etc., it is then possible to set up models

that lead to stationary relations among the variables, and

where standard inference is possible. Johansen co-

www.ijaers.com

integration test was used to find a broader classification of

co-integration for the variables, it follows that:

x1, t = 1 + 2 x 2, t + ... + pxp, t + ut

Page | 133

( 2)

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

Where, p is the number of variables in the equation. We

assumed that I (1) might cointegrate to form a stationary

relationship, and a stationary residual term ˆut =

x1,t−β1−β2x2,t−...−βpxp,t. This equation represents the

assumed economically understanding of steady state or

equilibrium relationship among the variables. If the

variables are cointegrating, they will share a common trend

and form a stationary relationship in the long run.

Table 4: Johansen Tests for cointegration

Maximum rank

Parm

LL

Eigen value

Trace stats

5% critical value

0

4

1.6114584

-0.9956

110.7300

47.21

1

11

26.019266

0.99241

61.9144

29.68

2

16

40.266099

0.94212

33.4207

33.4207

3

19

51.775911

0.89994

10.4011

3.76

4

20

56.976447

0.64658

27.6396

8.32

5

21

59.231780

0.62689

11.6591

7.45

6

23

61.534562

0.57243

79.6427

12.61

From our table 4, we see that our variables will cointegrate in the long run given that all six trace statistics are greater than

their corresponding 5% critical value.

Table 5: Granger Causality Wald Tests

Variable

Hypothesis

Lag

Chi 2

P> chi2

Decision

ER on SR

ER Granger Causes SR

1

3.5756

0.059

Reject

SR Granger Causes ER

1

23.139

0.000

Accept

DR Granger Causes SR

1

18.925

0.000

Accept

SR Granger Causes DR

1

20.33

0.000

Accept

DE Granger Causes SR

1

1.1883

0.276

Reject

SR Granger Causes DE

1

29.853

0.000

Accept

1

39.149

0.000

Accept

1

8.5031

0.004

Accept

DR on SR

DE on SR

CORGOV on SR

SR on CORGOV

CORGOV Granger Causes SR

SR Granger Causes CORGOV

After undergoing the series of test in tables 4 and 5 we

finally conduct our causality to test to estimate the

relationship between our variables. From our table above

we realize that Equity ratio does not granger cause Stock

return, however there is a granger cause of Stock return on

Equity ratio. This means that a change in stock return is

likely to have an impact on the percentage of total assets

that is contributed by equity. Practically, when stock returns

increase, more and more investors are likely to purchase the

banks shares. The increase in capital for the company raised

by selling additional shares of stock can finance additional

company growth. If the bank invests the additional capital

successfully, then the ultimate gains in stock price and

dividend pay-outs realized by investors may be more than

sufficient to compensate for the dilution of their shares.

www.ijaers.com

From table 5, we once again realize that Debt Ratio

granger causes Stock Return. Likewise, Stock Return also

granger causes Debt Ratio. We can at this point establish a

bi-directional causality between these two variables. By

this, we can also boldly say that a change in either Debt

Ratio or Stock return would cause a significant change in

both variables respectively. The last bit of our table depicts

a uni-directional causality. In the sense that, debt to equity

ratio does not granger cause Stock return whereas Stock

return granger causes debt to equity ratio. As earlier

established an increase in stock return may increase equity

holders of a bank, simultaneously, a bank may reduce its

debt as opposed to equity just so to have more ownership

interest. If equity is increased, possibility of the application

of retained earnings may lead to more funding for the bank’s

activities.

Page | 134

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

scores serve as a barometer, reflecting the level of

adherence to governance standards and practices within

financial institutions. In the vibrant landscape of Ghana's

banking sector, these scores become particularly

noteworthy, differentiating between listed and non-listed

banks. Corporate Governance Scores for Listed and NonListed Banks in Ghana serve as a critical benchmark for

evaluating how effectively financial institutions uphold

principles of transparency, accountability, and ethical

conduct. They offer a compelling glimpse into the

governance strategies employed by banks, with a particular

focus on those listed on the Ghana Stock Exchange, and

those operating independently outside the formal listing

framework.

The table 5 further revealed that there is a bi- causal

relationship between Corporate Governance and Stock

Return. Which means a change in corporate governance

would cause a significant change in Stock return and vice

versa. When stock returns are higher, the banks would in the

long run attract more and more investors and hence reduce

its debt and debt to equity ratios significantly. It is therefore

imperative that all Ghanaian banks; not just the listed few

drives towards achieving higher corporate governance

scores and subsequently increase their performance.

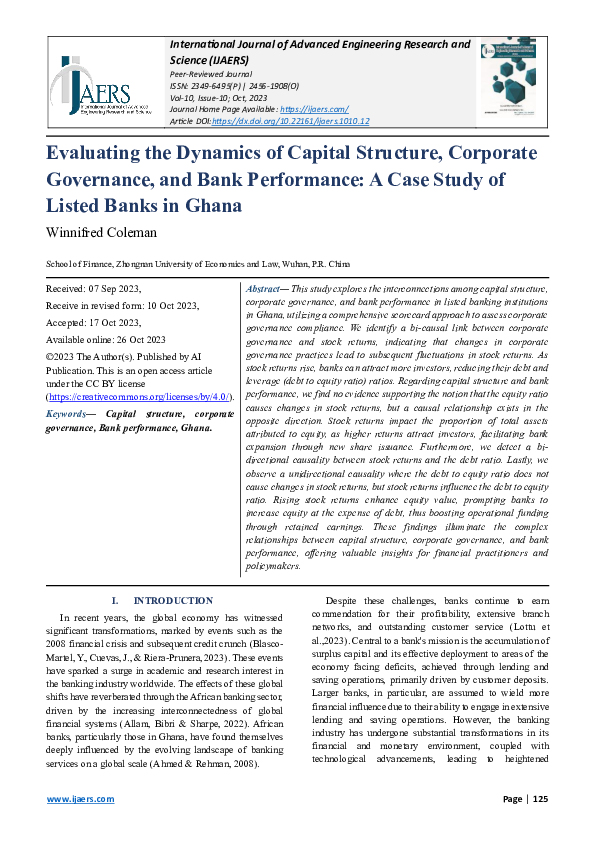

4.2 Corporate Governance and Bank Performance

In the realm of banking, the concept of Corporate

Governance Scores holds profound significance. These

MEAN SCORES

CORPORATE GOVERNANCE SCORES

41.1

44

18.18

22.74

24.54

2005

2006

2007

38.6

55.6

58.1

54.7

54.3

56.1

48.2

52.9

46.1

34.9

37.61

39.79

39.54

31

33.73

39.16

31.82

2008

2009

2010

2011

2012

2013

2014

2015

YEAR

LISTED BANKS

NON LISTED BANKS

Fig.2: Corporate Governance Scores for Listed and Non-Listed Banks in Ghana

Figure 2 illustrates that listed banks tend to attain higher

Corporate Governance scores compared to their non-listed

counterparts, indicating that listed banks are more likely to

implement rigorous corporate governance strategies

outlined by the Ghana Stock Exchange. This observation

prompts us to investigate whether these elevated corporate

governance scores have any causal impact on bank

performance, specifically measured as stock returns, and

vice versa. This analysis aims to explore the interplay

between corporate governance practices and stock returns,

shedding light on whether high corporate governance scores

contribute to better stock performance and, conversely,

whether strong stock returns can influence corporate

governance practices

Table 6: Capital Structure, Corporate Governance and Bank Performance

ROA

Coeff

ROE

Std

Coeff

Error

DR

-0.033

TOBIN

Std

Coeff

Error

SR

Std

Coeff

Error

Std

Error

0.19

-0.14

0.04*

-0.00

0.11

-0.19

0.008

0.19

0.00

0.00

-0.19

0.48*

ER

0.00

0.01

0.00

LR

0.00

0.00

0.06

0.00

0.00

0.00

-0.01

0.10

CORGOV

0.00

0.00

-0.01

0.00*

-0.00

0.00

-0.11

0.00*

Note: Significant at 5% critical value

www.ijaers.com

Page | 135

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

Our analysis suggests that only Return on Equity and

Stock Returns have a significant impact as seen in Table 6.

It's noteworthy that ROE and the Debt ratio exhibit a

negative relationship, implying that as the Debt ratio

increases, Return on Equity decreases. Our Johansen

cointegration test reinforces this finding, indicating that this

negative relationship holds in the long run. Furthermore,

our robust regression results reveal that Stock Returns have

a positive relationship with the Equity ratio. As ownership

interest increases, stock returns are expected to rise in the

long run. This observation aligns with our cointegration test,

confirming their coexistence in the long term. Additionally,

our robust analysis indicates that the relationship between

Corporate Governance and Return on Equity is significant

and positive. This implies that as more banks adopt better

Corporate Governance measures as outlined by the Ghana

Stock Exchange, Return on Equity is likely to increase.

V.

CONCLUSION AND POLICY

RECOMMENDATION

The Ghanaian banking sector has made commendable

strides in embracing corporate governance principles,

driven by the Securities and Exchange Commission's (SEC)

guidelines. This shift towards improved corporate

governance practices among banks in Ghana is a promising

development. The robust correlation between corporate

governance and bank performance underscores the

industry's dedication to adhering to SEC directives. The

commitment to ethical standards plays a pivotal role in

fraud prevention, transforming it into a collective

responsibility within these financial institutions. Enhanced

corporate governance not only safeguards against fraud and

conflicts of interest but also provides banks with a solid

foundation to explore more lucrative opportunities.

Furthermore, it is imperative to acknowledge the

consequential relationship between capital structure and

banks' performance in Ghana. The heavy reliance on debt

financing has led to a substantial debt ratio, hovering around

84%, with a corresponding negative association between

Return on Equity (ROE) and Debt Ratio. The prevalent use

of short-term customer deposits for debt financing further

exacerbates this issue, adding a layer of expense. The

study's findings emphasize that Ghanaian banks, on

average, employ GH¢6.34 in debt for every GH¢1 of equity.

This overdependence on short-term loans from customers

necessitates a reevaluation of financing strategies.

In light of these findings, it is essential for banks to

prioritize the utilization of internally generated funds to

support their operational activities. When external debt

becomes a requisite, banks should proactively seek lowinterest loans to ensure that the benefits of tax advantages

www.ijaers.com

outweigh any potential financial distress. To mitigate the

risks associated with heavy reliance on short-term, highcost debt, the Government of Ghana should collaborate with

financial sector stakeholders in fostering the development

of a bond market. This initiative would provide banks with

access to long-term debt, thereby reducing their dependence

on short-term sources.

Moreover, increasing tax relief measures could

substantially enhance banks' post-tax profits, leading to

improved retained earnings for internal investments. Given

the notable improvements in corporate governance scores

across banks, it is strongly recommended that the Bank of

Ghana, the industry regulator, harmonizes its regulations

with those stipulated by the Ghana Stock Exchange.

Specifically, the alignment should focus on disclosure

requirements. Such regulatory cohesion would exert

binding authority on banks to uphold governance standards,

in stark contrast to the non-binding nature of the SEC code.

While this study has centered on the Ghanaian banking

industry, it encourages future research to extend its scope to

other sectors, including telecommunications, insurance, and

pharmaceuticals. Additionally, researchers should consider

diversifying data sources beyond annual reports to capture

a more comprehensive dataset. Finally, there is a

compelling need for future investigations into exploring the

causal relationship between corporate governance and

performance.

In summation, the findings of this study underscore the

pivotal role played by corporate governance practices and

capital structure decisions in the Ghanaian banking sector.

By acting on the policy recommendations outlined above

and prioritizing corporate governance enhancements while

diversifying financing sources, Ghana's banking sector can

strive for sustained growth, financial stability, and longterm success.

VI.

LIMITATIONS AND SUGGESTIONS FOR

FUTURE STUDY

Just as any paper, this study comes with its own

limitations and hence should be taken into account when

interpreting its findings of this study. The limitations cut

across areas such as the sample size, data size and accuracy

and use of primary data. For instance, this study had limited

sample size of only eleven listed banks in Ghana which

restricts the generalizability of the results to the entire

banking industry in the country. This small sample size may

not fully capture the diversity and complexities of the

broader banking sector, potentially leading to biased or

incomplete conclusions. Additionally, the study solely

relied on annual reports as the primary data source and

hence may overlook critical information that could

Page | 136

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

contribute to a more comprehensive analysis. Data accuracy

and availability within annual reports may also vary among

banks, affecting the overall quality of the study's findings.

Furthermore, the study's exclusion of banks whose

annual reports were not obtained within the specified time

frame introduces selection bias, as reporting schedules and

delays can differ among financial institutions. Additionally,

while the study explored relationships between variables, it

did not establish causality. Future research could address

these limitations by considering a more extensive and

diverse sample, incorporating additional data sources,

accounting for external factors, and conducting longitudinal

analyses to provide a more robust understanding of the

complex interplay between corporate governance, capital

structure, and bank performance.

Furthermore, one promising area for future

research is the exploration of how changes in regulatory

frameworks and policies impact the relationship between

corporate governance, capital structure, and bank

performance. Regulatory changes, both at the national and

international levels, can have profound effects on financial

institutions. Investigating how shifts in regulatory

environments influence the strategies and practices of banks

in Ghana could provide valuable insights for policymakers,

regulators, and industry stakeholders. Additionally, future

could consider looking at a comparative analysis across

different industries in Ghana, such as telecommunications,

insurance, and pharmaceuticals, could shed light on whether

the observed relationships between corporate governance,

capital structure, and performance are unique to the banking

sector or extend to other sectors. This comparative approach

would contribute to a more comprehensive understanding

of the broader implications of corporate governance

practices on various industries within the Ghanaian

economy.

Moreover, future studies could delve into the

causal mechanisms underlying the identified relationships.

By employing advanced statistical methods and

longitudinal analyses, researchers can explore the causal

pathways through which corporate governance decisions

influence capital structure choices and, in turn, impact bank

performance. This deeper exploration of causality would

enhance our understanding of the dynamics at play in the

financial sector and provide actionable insights for

practitioners and policymakers.

REFERENCES

[1] Abdullah, H., & Tursoy, T. (2023). The effect of corporate

governance on financial performance: evidence from a

shareholder-oriented

system. Iranian

Journal

of

Management Studies, 16(1), 79-95.

www.ijaers.com

[2] Abor (2007), Relationship between capital structures of

publicly quoted firms, large unquoted firms, and Small and

Medium Enterprises in Ghana.

[3] Abor, J. and Biekpe, N. (2005), “What determines the capital

structure of listed firms in Ghana? African Finance Journal,

Vol. 7 No. 1, pp. 37-48.

[4] Abu‐Rub, N. (2012), ‘Capital Structure and Firm

Performance: Evidence from Palestine Stock Exchange’,

Journal of Money, Investment and Banking, Vol. 23, pp. 109–

17.

[5] Agwu, A. E., Suvedi, M., Chanza, C., Davis, K., OywayaNkurumwa, A., Mangheni, M. N., & Sasidhar, P. V. K. (2023).

Agricultural Extension and Advisory Services in Nigeria,

Malawi, South Africa, Uganda, and Kenya.

[6] Al-Zaqeba, M. A. A., Abdul Hamid, S., Ineizeh, N. I.,

Hussein, O. J., & Albawwat, A. H. (2022). The effect of

corporate governance mechanisms on earnings management

in Malaysian manufacturing companies. Asian Economic and

Financial Review.

[7] Allam, Z., Bibri, S. E., & Sharpe, S. A. (2022). The rising

impacts of the COVID-19 pandemic and the Russia–Ukraine

war: energy transition, climate justice, global inequality, and

supply chain disruption. Resources, 11(11), 99.

[8] Amidu, M. (2007) “Determinants of Capital Structure of

Banks in Ghana: an empirical approach. Baltic Journal of

Management.2(1), .67-69Watson and Head (2007).

[9] Asuamah Yeboah, S. (2023). Unleashing Ghana's

Manufacturing Might: A Comprehensive Analysis of

Performance, Competitiveness, and Policy Pathways.

[10] Berger, A. N. and L. N. Babinskaia (2002), ‘Capital Structure

and Firm Performance: A New Approach to Testing Agency

Theory and an Application to the Banking Industry’,

International Review of Business Research Papers, Vol. 6,

No. 2, pp. 17–55.

[11] Bianchi, M., M. L. Di Battista and G. Lusignani (1998):

"Asset to proprietario e performance dell banche". Banca,

Impresa, Società, forthcoming.

[12] Bisht, D., Singh, R., Gehlot, A., Akram, S. V., Singh, A.,

Montero, E. C., ... & Twala, B. (2022). Imperative role of

integrating digitalization in the firms finance: A technological

perspective. Electronics, 11(19), 3252

[13] Blasco-Martel, Y., Cuevas, J., & Riera-Prunera, M. C. (2023).

The consolidation of public banking in Spain: from the 1970s

crisis to the 2008 crisis. Financial History Review, 30(1), 128.

[14] Boadi, I., & Osarfo, D. (2019). Diversity and return: the

impact of diversity of board members’ education on

performance. Corporate Governance: The International

Journal of Business in Society, 19(4), 824-842.

[15] Bokpin, G. A., A. Q. Q. Aboagye and K. A. Osei (2010), ‘Risk

Exposure and Corporate Financial Policy on the Ghana Stock

Exchange’, Journal of Risk Finance, Vol. 11, No. 3, pp. 323–

32.

[16] Borgia F. (2005). Corporate Governance and Transparency

Role of Disclosure: How Prevent New Financial

[17] Bos, T. and Fetherston, T.A. (1993), “Capital Structure

Practices on the Pacific rim”, Research in International

Business and Finance, Vol. 10, pp. 53-66.

Page | 137

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

[18] Brickley, J.A., Coles, J.L. and Jarrell, G. (1997) Leadership

Structure: Separating the CEO a Chairman of the Board.

Journal

of

Corporate

Finance,

3,

189-220.

https://doi.org/10.1016/S0929-1199(96)00013-2

[19] Claessens, S. (2003). Corporate governance and

development. The International Bank for Reconstruction and

Development/ World Bank. http://www.ifc.org.

[20] Claessens, S., & Fan, J. P. H. (2003). Corporate Governance

in Asia: A Survey. International Review of Finance, 3(2), 71–

103.

[21] Dadson Awunyo-Vitor and Jamil Badu (March 2012).in their

research, capital structure and bank performance in Ghana.

[22] De Bonis, R. (1997) : "Passato e presente delle banche

pubbliche". Banca d'Italia, manuscript.

[23] Ebenezer Edward Arthur, Corporate governance, and

performance of banks in Ghana, September 2015.

[24] El-Chaarani, H., Abraham, R., & Skaf, Y. (2022). The impact

of corporate governance on the financial performance of the

banking sector in the MENA (Middle Eastern and North

African) region: An immunity test of banks for COVID19. Journal of Risk and Financial Management, 15(2), 82

[25] El‐Sayed Ebaid, I. (2009). The impact of capital‐structure

choice on firm performance: empirica evidence from Egypt.

The Journal of Risk Finance, 10(5), 477–487.

doi:10.1108/15265940911001385

[26] El‐Sayed Ebaid, I. (2009). The impact of capital‐structure

choice on firm performance: empirical evidence from Egypt.

The Journal of Risk Finance, 10(5), 477–487.

doi:10.1108/15265940911001385

[27] Elewechi N. M. Okike, 2007. "Corporate Governance in

Nigeria: the status quo," Corporate Governance: An

International Review, Wiley Blackwell, vol. 15(2), pages

173-193.

[28] Fama, E. F. and K. R. French (2002), ‘Testing Trade‐off and

Pecking Order Predictions about Dividends and Debt.

Review of Financial Studies, Vol. 15, No. 1, pp. 1–33.

[29] Farabullini, F. and G. Gobbi (1996): "La redditività delle

banche italiane negli ultimi venti anni" Banca d'Italia,

manuscript.

[30] Frank, M. and Goyal, V. (2003), “Testing the pecking order

theory of capital structure. Journal of Financial Economics,

Vol. 67, pp. 217-48.

[31] Ghana SEC (2020). Code of Best Practices for the Public

Companies.

[32] Gleason, K. C., L. K. Mathur and I. Mathur (2000), ‘The

Interrelationship between Cultures,Capital Structure, and

Performance: Evidence from European Retailers’, Journals of

Business Research, Vol. 50, pp. 185–91.

[33] Glen, J. and Pinto, B. (1994), “Debt or Equity? How Firms in

Developing Countries Choose”, IFC Discussion paper No.

22, pp. 1-16.

[34] Global Legal Insights (2016), Ghana Banking Regulation 3rd Edition

[35] Hadlock, C. J. and C. M. James (2002), ‘Do Banks Provide

Financial Slack?’ Journal of Finance, Vol. 57, No. 3, pp.

1383–420.

[36] Hansen, G. S. and B. Wernerfelt (1989), ‘Determinants of

Firm Performance: The Relative Importance of Economic

www.ijaers.com

and Organizational Factors’, Strategic Management Journal,

Vol. 10, No. 5, pp. 399–411.

[37] Haralayya, B. (2022). An Exploratory Investigation On

Implications Of Corporate Governance On Financial

Performance In India. Journal of Positive School

Psychology, 6(8), 633-647.

[38] Hoffmann, P. S. (2011), ‘Determinants of the Profitability of

the US Banking Industry’ International Journal of Business

and Social Science, Vol. 2, No. 22, pp. 1–15.

[39] Huynh, Q. L., Hoque, M. E., Susanto, P., Watto, W. A., &

Ashraf, M. (2022). Does financial leverage mediates

corporate

governance

and

firm

performance?. Sustainability, 14(20), 13545.

[40] Jensen, M.C., and W.H. Meckling. 1976. Theory of the firm:

Managerial behavior, agency cost and ownership structure.

Journal of Financial Economics 3 (4): 305–360.

[41] Khan, N., Abraham, O. O., Alex, A., Eluyela, D. F., &

Odianonsen, I. F. (2022). Corporate governance, tax

avoidance, and corporate social responsibility: Evidence of

emerging market of Nigeria and frontier market of

Pakistan. Cogent Economics & Finance, 10(1), 2080898.

[42] Kumar, K., Kumari, R., Nandy, M., Sarim, M., & Kumar, R.

(2022). Do ownership structures and governance attributes

matter for corporate sustainability reporting? An examination

in the Indian context. Management of Environmental

Quality: An International Journal, 33(5), 1077-1096.

[43] Kuznnetsov, P. &Muravyev, A. (2001). Ownership structure

and Firm Performance in Russia, the case of Blue Chips of

the Stock Market. Economic Education and Research

Consortium. Working Paper Series. No. 01/10.

[44] Lee, Yung Sheng, Stuart Rosenstein, and Jeffrey G. Wyatt.

1999. The value of financial outside directors on corporate

boards. International Review of Economics & Finance 8 (4):

421-431.

[45] Lottu, O. A., Abdul, A. A., Daraojimba, D. O., Alabi, A. M.,

John-Ladega, A. A., & Daraojimba, C. (2023). DIGITAL

TRANSFORMATION IN BANKING: A REVIEW OF

NIGERIA'S

JOURNEY

TO

ECONOMIC

PROSPERITY. International

Journal

of

Advanced

Economics, 5(8), 215-238.

[46] Maama, H. (2021). Achieving financial sustainability in

Ghana’s banking sector: is environmental, social and

governance reporting contributive?. Global Business Review,

09721509211044300.

[47] Modigliani, F. and Miller, M. (1958), “The Cost of Capital,

Corporation Finance, and the Theory of Investment”, The

American Economic Review, Vol. 48, 261–297. Mers, 1984.

[48] Molla, M. I., Islam, M. S., & Rahaman, M. K. B. (2023).

Corporate governance structure and bank performance:

evidence from an emerging economy. Journal of Economic

and Administrative Sciences, 39(3), 730-746.

[49] Myres, S.C (2001), “Capital Structure”, The Journal of

Economic Perspectives, 15 (2), 81-102.

[50] Nawaz, T., & Ohlrogge, O. (2022). Clarifying the impact of

corporate governance and intellectual capital on financial

performance: A longitudinal study of Deutsche Bank (1957–

2019). International Journal of Finance & Economics.

Page | 138

�Coleman

International Journal of Advanced Engineering Research and Science, 10(10)-2023

[51] Nobanee, H., & Ellili, N. O. D. (2022). Voluntary corporate

governance disclosure and bank performance: evidence from

an emerging market. Corporate Governance: The

international journal of business in society, 22(4), 702-719.

[52] Nyakundi, D.O., M.O. Nyamita, and T.M. Tinega. 2014.

Effect of internal control systems on financial performance of

small and medium scale business enterprises in Kisumu City,

Kenya. International Journal of Social Sciences and

Entrepreneurship 1 (11): 719–734.

[53] Oanh, T. T. K., Van Nguyen, D., Le, H. V., & Duong, K. D.

(2023). How capital structure and bank liquidity affect bank

performance: Evidence from the Bayesian approach. Cogent

Economics & Finance, 11(2), 2260243.

[54] OECD (2004). Principle of Corporate governance; edited

2004, Retrieved from, http:// www oecd. org/ corporate/ ca/

corporategovernanceprinciples/ 31557 724. Pdf

[55] Olusegun Gabriel Adegbite; Corporate governance

developments in Ghana: the past, the present and the future.

[56] Omete, F. I. (2023). Financial Intermediation Efficiency and

Performance of Commercial Banks Listed On the Nairobi

Securities Exchange in Kenya (Doctoral dissertation,

JKUAT-COHRED).

[57] Opoku-Asante, K., Winful, E. C., Sharifzadeh, M., &

Neubert, M. (2022). The relationship between capital

structure and financial performance of firms in Ghana and

Nigeria. European Journal of Business and Management

Research, 7(1), 236-244.

[58] Park, S. (2022). Do bank capital requirements make resource

allocation suboptimal?. Journal of Economic Analysis, 1(2),

35-49.

[59] PricewaterhouseCoopers (Ghana) Limited ,2009 Ghana

Banking Survey: Will Ghana’s Banking Industry survive the

crunch?

[60] Rajan, R. and Zingales, L. (1995), “What do we know about

capital structure? Some evidence from international data”,

Journal of Finance, Vol. 50, pp. 1421-60.

[61] Ramaswamy, K. (2001), “Organizational ownership,

competitive intensity, and firm performance: an empirical

study of the Indian manufacturing sectors”, Strategic

Management Journal, Vol. 22, pp. 989-98.

[62] Rechner, P. and Dalton, D (1991) 'CEO Duality and

Organizational Performance: Longitudinal study', Strategic

Management Journal, vol. 12, no. 155-160

[63] Rehman H. and Ahmed S. (2008), an empirical analysis of the

determinants of bank selection in Pakistan: A customer view.

Pakistan Economic and Social Review, Volume 46, No. 2

(winter), pp. 147‐160.

[64] Rosenstein, S., and Wyatt, J.G. (1990) 'Outside Directors,

Board Independence, and Shareholder Wealth', Journal of

Financial Economics, vol. 26, no. 2, pp. 175-91

[65] Ross, S.A. 1973. The economic theory of agency: The

principal’s problem. The American Economic Review 63

(2): 134–139.

[66] Saunders, M., Lewis P. and Thornhill, A., (2007), Research

Methods for Business Students, 4th ed., Prentice Hall, UK.

[67] Shleifer, A. and Vishny, R.W. (1997) 'A Survey of Corporate

Governance', The Journal of Finance, vol. 50, no. 2, pp. 73783.

www.ijaers.com

[68] Smallman, C 2004, 'Exploring Theoretical Paradigm in

Corporate Governance', International Journal of Business

Governance and Ethics, vol. 1, no. 1, pp. 78-94.

[69] Spathis C. Kosmidou Κ. and Doumpos Μ. (2002) “Assessing

Profitability Factors in the Greek Banking System”,

International Transactions in Operational Research, Vol. 9,

No. 5,517- 530.

[70] Sulaiman, M.A. Al-Sakran, (2001), “Leverage Determinants

in the Absence of Corporate Tax System: The Case of NonFinancial Publicly Traded Corporations in Saudi Arabia.

Managerial Finance 27, 261 – 275.

[71] Suryanarayana, A (ed.) 2005, Corporate Governance: The

Current Crisis and The Way Out, ICFAI. University Press,

Hyderabad

[72] Switzerland (2014) Swiss Code of Best Practice for

Corporate Governance. Zurich: Economiesuisse

[73] Titman, S., &Wessels, R. (1988). The determinants of capital

structure choice. Journal of Finance, 43(1), 1-19.

[74] Tze, O. S., &Heng, B. T. Capital Structure and Corporate

Performance of Malaysian Construction Sector (2011).

International Journal of Humanities and Social Science, 1(2),

28-36.

[75] United Kingdom Financial Reporting Council (2012) The

UK Corporate Governance Code. London: Financial

Reporting Council.

[76] Watson, D. and Head, A. (2007), Corporate Finance–

Principles and Practices, 4th ed., FT Prentice Hall, UK.

[77] Yermack, D. 1996. Higher market valuation of companies

with a small board of directors. Journal of Financial

Economics 40 (2): 185–211.

Page | 139

�

IJAERS Journal

IJAERS Journal