RU2673399C1 - Method of preserving savings purchasing ability - Google Patents

Method of preserving savings purchasing ability Download PDFInfo

- Publication number

- RU2673399C1 RU2673399C1 RU2017131390A RU2017131390A RU2673399C1 RU 2673399 C1 RU2673399 C1 RU 2673399C1 RU 2017131390 A RU2017131390 A RU 2017131390A RU 2017131390 A RU2017131390 A RU 2017131390A RU 2673399 C1 RU2673399 C1 RU 2673399C1

- Authority

- RU

- Russia

- Prior art keywords

- value

- savings

- named

- standard

- cost

- Prior art date

Links

Classifications

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q20/00—Payment architectures, schemes or protocols

-

- G—PHYSICS

- G06—COMPUTING OR CALCULATING; COUNTING

- G06Q—INFORMATION AND COMMUNICATION TECHNOLOGY [ICT] SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES; SYSTEMS OR METHODS SPECIALLY ADAPTED FOR ADMINISTRATIVE, COMMERCIAL, FINANCIAL, MANAGERIAL OR SUPERVISORY PURPOSES, NOT OTHERWISE PROVIDED FOR

- G06Q30/00—Commerce

Landscapes

- Business, Economics & Management (AREA)

- General Physics & Mathematics (AREA)

- Strategic Management (AREA)

- Physics & Mathematics (AREA)

- General Business, Economics & Management (AREA)

- Accounting & Taxation (AREA)

- Engineering & Computer Science (AREA)

- Theoretical Computer Science (AREA)

- Development Economics (AREA)

- Economics (AREA)

- Finance (AREA)

- Marketing (AREA)

- Financial Or Insurance-Related Operations Such As Payment And Settlement (AREA)

Abstract

Description

Настоящее изобретение относится к области вычислительной техники и информационных технологий, а именно, к области создания и использования баз данных и систем электронного документооборота, эмиссии/демиссии и обращения электронных денег, выполнения электронных платежей и функционирования электронных платежных систем. Назначением изобретения является обеспечение неизменности покупательной способности доходов и сбережений населения и предприятий, что позволяет при осуществлении торговых операций и при материальном обеспечении населения избежать потерь, связанных с изменением покупательной способности денег.The present invention relates to the field of computer engineering and information technology, namely, to the field of creating and using databases and electronic document management systems, issue / release and circulation of electronic money, electronic payments and the functioning of electronic payment systems. The purpose of the invention is to ensure the invariability of the purchasing power of income and savings of the population and enterprises, which allows to avoid losses associated with changes in the purchasing power of money when carrying out trade operations and with material support of the population.

Стоимость денег традиционно была привязана к их носителям - монетам и банкнотам. Несмотря на то, что в современном мире деньги преимущественно являются безналичными и существуют в виде электронной записи на счете и лишены физического носителя, привязка стоимости к носителю, остается правилом во всех валютных зонах.The value of money has traditionally been tied to their carriers - coins and banknotes. Despite the fact that in the modern world money is predominantly non-cash and exists in the form of an electronic record on the account and is deprived of a physical medium, linking the value to the medium remains the rule in all currency zones.

Управление стоимостью денег в современном мире происходит через выпуск дополнительных денег или изъятия избытков денег на рынке. Вместе с тем наличие ставки рефинансирования центрального банка, спекулятивные операции на фондовых рынках и рынках обмена валют могут приводить к значительному колебанию стоимости денег и, как следствие, к изменению покупательной способности сбережений. Страх снижения покупательной способности сбережений заставляет людей брать на себя риски, которых они брать на себя не стали бы, если сбережения были бы защищены от снижения покупательной способности. Так людям приходится открывать депозиты в банках благонадежность которых они сами оценить не в состоянии или другими способами пускать деньги в оборот, тем самым принимая на себя риски потери сбережений, которыми они сами управлять не в состоянии. В случае дефолта банка или в случае неудачного размещения денег непрофессиональные инвесторы рискуют потерять значительную часть сбережений или даже их все. Связанные с этим переживания часто приводят людей к психологическим расстройствам, заболеваниям и даже самоубийствам. Поскольку подавляющая часть населения не является профессиональными инвесторами, то сохранение покупательной способности сбережений отвечает потребностям практически всего населения, при этом самыми уязвимыми для колебаний покупательной способности сбережений группами населения являются государственные служащие, пенсионеры и инвалиды. Таким образом, возможность сохранения покупательной способности сбережений обладает огромным полезным эффектом.Management of the value of money in the modern world occurs through the release of additional money or withdrawal of excess money in the market. At the same time, the presence of a central bank refinancing rate, speculative operations in stock and currency exchange markets can lead to a significant fluctuation in the value of money and, as a result, to a change in the purchasing power of savings. The fear of a decline in the purchasing power of savings forces people to take risks that they would not take if the savings were protected from a decrease in purchasing power. So people have to open deposits in banks, the reliability of which they themselves are not able to evaluate or otherwise put money into circulation, thereby taking on the risks of losing savings that they themselves are not able to manage. In the event of a default of the bank or in case of unsuccessful placement of money, non-professional investors risk losing a significant part of their savings, or even all of them. The experiences associated with this often lead people to psychological disorders, illnesses, and even suicides. Since the overwhelming majority of the population is not professional investors, the preservation of the purchasing power of savings meets the needs of almost the entire population, while the most vulnerable to fluctuations in the purchasing power of savings are civil servants, pensioners, and people with disabilities. Thus, the ability to preserve the purchasing power of savings has a huge beneficial effect.

В условиях высокой волатильности стоимости денег возникают серьезные риски возникновения убытков также и для бизнеса, прежде всего для участников экспортно-импортных торговых операций. Оптовые поставщики часто отгружают товар потребителям на условиях товарного кредита, для чего используют собственный или заемный оборотный капитал и, если за срок товарного кредитования курс валюты снижался, то поставщик понесет убытки пропорциональные снижению покупательной способности валюты расчетов и как результат не сможет на вырученные деньги оборотного капитала восстановить товарный запас. Быстрое снижение курса национальной валюты, как правило, ведет к быстрому снижению внутренних товарных запасов и остановке экспортно-импортных операций, что в конце концов ведет к коллапсу трансграничной оптовой торговли. Таким образом, сохранение покупательной способности валюты расчетов позволяет стабилизировать оптовую и розничную торговлю, а также увеличить сроки товарного кредитования, что в конце концов позволяет увеличить объемы торговли.In conditions of high volatility of the value of money, serious risks arise for losses also for business, especially for participants in export-import trade operations. Wholesale suppliers often ship goods to consumers on the terms of a commodity loan, for which they use their own or borrowed working capital and, if the currency exchange rate has decreased over the period of commodity lending, the supplier will incur losses proportional to the decrease in the purchasing power of the settlement currency and, as a result, will not be able to use working capital for the proceeds restore inventory. A rapid depreciation of the national currency, as a rule, leads to a rapid decline in domestic inventories and a halt in export-import operations, which ultimately leads to a collapse of cross-border wholesale trade. Thus, maintaining the purchasing power of the settlement currency allows you to stabilize wholesale and retail trade, as well as increase the terms of commodity lending, which ultimately allows you to increase trading volumes.

На внутреннем рынке волатильность стоимости денег также приводит к негативным изменениям в динамике и объемах торговли, особенно в части торговли импортными товарами и услугами на потребительском рынке. Колебания динамики и объемов торговли на внутреннем рынке в условиях быстрого изменения национальной валюты связано, прежде всего, с поведением покупателей, которые пытаются защитить свои сбережения от обесценивания путем вложения сбережений в товары, стоимость которых с точки зрения покупателей не подвержена такому быстрому изменению стоимости как стоимость денег.In the domestic market, the volatility of the value of money also leads to negative changes in the dynamics and volumes of trade, especially in terms of trade in imported goods and services in the consumer market. Fluctuations in the dynamics and volume of trade in the domestic market in the context of a rapid change in the national currency is primarily due to the behavior of buyers who try to protect their savings from depreciation by investing savings in goods whose value from the point of view of buyers is not subject to such a rapid change in value as the cost money.

Таким образом, и продавцы и покупатели заинтересованы в стабилизации стоимости сбережений и накоплений, то есть заинтересованы в стабилизации покупательной способности сбережений или кошельков, а сама стабилизация покупательной способности сбережений и валюты имеет огромный экономический эффект.Thus, both sellers and buyers are interested in stabilizing the cost of savings and savings, that is, they are interested in stabilizing the purchasing power of savings or wallets, and the stabilization of the purchasing power of savings and currency has a huge economic effect.

Поскольку сбережения представлены денежными средствами, находящимися в кошельке или на счете, то далее будем считать значения слов «сбережения», «накопления» и «кошелек» эквивалентными по смыслу для целей настоящего изобретения.Since the savings are represented in cash in the wallet or in the account, then we will consider the meaning of the words “savings”, “savings” and “wallet” to be equivalent in meaning for the purposes of the present invention.

Попытки людей избавиться от падающих в цене денег доказывают, что для людей ценность денег состоит не в их физическом количестве, а в покупательной способности сбережений, то есть в количестве товаров и услуг, которую может себе позволить приобрести человек на свои сбережения. Каждому человеку хотелось бы, чтобы покупательная способность его сбережений, по меньшей мере, не уменьшалась, однако, как видно из статистики, стоимость потребительской корзины товаров и услуг (далее «потребительская корзина» или «корзина») с годами растет во всех валютных зонах, а в некоторых валютных зонах наблюдается такой стремительный рост стоимости продуктов и услуг, что он лишает людей возможности иметь какие бы то ни было сбережения (https://tradingeconomics.com/united-states/consumer-price-index-cpi). Как видим, денежная политика центральных банков и финансовых властей, сводящаяся к управлению курсовыми стоимостями валют друг к другу не позволяет сохранить покупательную способность сбережений и потому традиционный подход требует ревизии.Attempts by people to get rid of falling in the price of money prove that for people the value of money does not lie in their physical quantity, but in the purchasing power of savings, that is, in the amount of goods and services that a person can afford to buy for his savings. Each person would like the purchasing power of his savings, at least not to decrease, however, as can be seen from statistics, the cost of a consumer basket of goods and services (hereinafter referred to as the “consumer basket” or “basket”) grows over the years in all currency zones, and in some currency zones there is such a rapid increase in the cost of products and services that it deprives people of the opportunity to have any kind of savings (https://tradingeconomics.com/united-states/consumer-price-index-cpi). As you can see, the monetary policy of central banks and financial authorities, which boils down to managing the exchange rates of currencies against each other, does not allow preserving the purchasing power of savings, and therefore the traditional approach requires revision.

Задачей настоящего изобретения является разработка способа управления стоимостью сбережений, позволяющего стабилизировать покупательную способность сбережений и тем самым защитить различные группы населения, а также защитить представителей бизнеса в торговле и производстве.The present invention is the development of a method of managing the cost of savings, which allows to stabilize the purchasing power of savings and thereby protect various groups of the population, as well as protect business representatives in trade and production.

Краткая сущность изобретенияSUMMARY OF THE INVENTION

Для решения поставленной задачи настоящее изобретение предлагает выражать стоимость сбережений одновременно в стандартных единицах стоимости и в денежных единицах стоимости сбережений. Причем в денежной системе рассчитывают курс обмена одной стандартной единицы на денежные единицы, путем расчета денежной стоимости корзины и ее приравнивания одной стандартной единице стоимости. При росте денежной стоимости корзины путем дополнительной эмиссии денег пропорционально увеличивают денежную стоимость сбережений, а при снижении денежной стоимости корзины путем частичного изъятия денег из суммы сбережений пропорционально уменьшают денежную стоимость сбережений, при этом стандартная стоимость сбережений остается неизменной, что и позволяет достигнуть требуемого полезного эффекта изобретения.To solve this problem, the present invention proposes to express the cost of savings simultaneously in standard units of value and in monetary units of the value of savings. Moreover, in the monetary system, the exchange rate of one standard unit for monetary units is calculated by calculating the monetary value of the basket and equating it to one standard unit of value. With the increase in the monetary value of the basket through additional issue of money, the monetary value of the savings is proportionally increased, and when the monetary value of the basket is reduced by partially withdrawing money from the amount of savings, the monetary value of the savings is proportionally reduced, while the standard value of the savings remains unchanged, which allows to achieve the desired useful effect of the invention .

Сущность изобретенияSUMMARY OF THE INVENTION

Для решения поставленной задачи сначала определим, что означает «покупательная способность» сбережений. Удовлетворение прямых потребностей человека не может быть выражено количеством золота или серебра, потому что человек как биологический вид не способен потреблять эти металлы или бумажные деньги напрямую в качестве пиши, одежды, жилья или жизненно важных услуг. Поэтому во всех развитых экономиках определено понятие «потребительской корзины товаров и услуг», которая и является списком товаров и услуг прямого потребления для людей, без которых жизнь современного человека представляется недостаточно обеспеченной. Поэтому для целей изобретения «покупательной способностью» сбережений будем считать способность сбережений приобретать товары и услуги из потребительской корзины.To solve this problem, we first determine what “purchasing power” of savings means. Satisfaction of a person’s direct needs cannot be expressed by the amount of gold or silver, because a person as a biological species is not able to consume these metals or paper money directly as writing, clothing, housing or vital services. Therefore, in all developed economies, the concept of “consumer basket of goods and services” is defined, which is a list of direct consumption goods and services for people without whom the life of a modern person seems to be insufficiently secured. Therefore, for the purposes of the invention, the “purchasing power" of savings will be considered the ability of savings to purchase goods and services from a consumer basket.

Такой подход является общепризнанным и потому финансовые власти практически всех развитых стран публикуют данные по стоимости потребительской корзины товаров и услуг, а также публикуют Индекс Потребительских Цен - Consumer Price Index, данные по которому публикуются например здесь https://tradinqeconomics.com/united-states/consumer-price-index-cpi. Стоимость корзины в США выражена в долларах США, стоимость корзины в России номинирована а Рублях, однако используя курсы валют, например курс Доллара США к Российскому Рублю можно рассчитать стоимость потребительской корзины в США в Российских Рублях. Поскольку криптовалюты можно обменять на доллары США и другие валюты, включая Российские Рубли, то используя курс такого обмена можно рассчитать стоимость корзины в США или в России в любой валюте мира. Вместе с тем, содержание корзины товаров и услуг в каждой юрисдикции разное и оно меняется со временем. Например в настоящее время в корзину включена мобильная связь, но тридцать лет назад мобильная связь не существовала и потому не была частью услуг корзины. Цена помидоров в США и России также может существенно отличаться, а потому и стоимость корзины с одинаковым списком товаров и услуг может также отличаться по цене. Таким образом, содержание товаров и услуг в потребительской корзине является вопросом консенсуса специалистов конкретной юрисдикции, а стоимость корзины в разных юрисдикциях также может быть разной. Однако для целей платежной системы содержание корзины можно или заимствовать или создать свой набор товаров и услуг, которые внутри платежной системы будут считаться корзиной, стоимость которой в денежных единицах платежной системы будет вычисляться на основе действующих цен на включенные в корзину продукты и услуги, а также на основе курса обмена денежных единиц системы на фиатные валюты, такие как доллары США, Российские Рубли или другие фиатные валюты или криптовалюты.This approach is generally recognized and therefore the financial authorities of almost all developed countries publish data on the cost of a consumer basket of goods and services, as well as publish the Consumer Price Index, data on which are published for example here https://tradinqeconomics.com/united-states / consumer-price-index-cpi. The basket value in the USA is expressed in US dollars, the basket value in Russia is denominated in Rubles, however, using exchange rates, for example, the exchange rate of the US Dollar to the Russian Ruble, you can calculate the value of the consumer basket in the USA in Russian Rubles. Since cryptocurrencies can be exchanged for US dollars and other currencies, including Russian Rubles, using the exchange rate of such an exchange, you can calculate the cost of a basket in the USA or in Russia in any currency of the world. At the same time, the content of the basket of goods and services in each jurisdiction is different and it changes over time. For example, mobile communications are currently included in the basket, but thirty years ago mobile communications did not exist and therefore was not part of the basket services. The price of tomatoes in the USA and Russia can also vary significantly, and therefore the cost of a basket with the same list of goods and services may also differ in price. Thus, the content of goods and services in the consumer basket is a matter of consensus among specialists in a particular jurisdiction, and the cost of the basket in different jurisdictions can also be different. However, for the purposes of the payment system, the contents of the basket can either be borrowed or you can create your own set of goods and services, which inside the payment system will be considered a basket, the value of which in monetary units of the payment system will be calculated based on current prices for the products and services included in the basket, as well as based on the exchange rate of the system’s monetary units for fiat currencies such as US dollars, Russian Rubles or other fiat currencies or cryptocurrencies.

Как было показано выше для измерения меры потребления в развитых странах используется потребительская корзина товаров и услуг, которая является стандартом потребления в каждой такой стране. Для того чтобы покупательную способность можно было измерять, введем соответствующую стандартную стоимость сбережений и договоримся измерять ее в «стандартных единицах» или в «стандартах», которые будем обозначать как «Std», таким образом, стоимость кошелька эквивалентная трем потребительским корзинам, будет выражаться как<3 std>. Договоримся также, что денежная стоимость одного стандарта всегда должна быть равна денежной стоимости одной потребительской корзины товаров и услуг. Таким образом, при изменении денежной стоимости корзины одновременно и в равной степени должна меняться и денежная стоимость одного стандарта, таким образом обеспечивая неизменность стандартной стоимости названной корзины. То есть для достижение полезного эффекта - неизменности покупательной способности сбережений, при изменении денежной стоимости сбережений, стандартная стоимость сбережений меняться не должна.As shown above, in order to measure the measure of consumption in developed countries, a consumer basket of goods and services is used, which is the standard of consumption in each such country. In order for purchasing power to be measured, we introduce the corresponding standard cost of savings and agree to measure it in “standard units” or in “standards”, which we will designate as “Std”, so the wallet cost equivalent to three consumer baskets will be expressed as <3 std>. We also agree that the monetary value of one standard should always be equal to the monetary value of one consumer basket of goods and services. Thus, when the monetary value of the basket changes, the monetary value of one standard should simultaneously and equally change, thus ensuring that the standard value of the named basket remains unchanged. That is, to achieve a useful effect - the invariability of the purchasing power of savings, when the monetary value of savings changes, the standard cost of savings should not change.

Поддержание неизменной покупательной способности сбережений осуществляют в платежной системе, где средством платежа являются электронные деньги, где денежная стоимость товаров, услуг, платежей и сбережений представлена суммой электронных денег, где платежи проводятся между кошельками или заимодавца и заемщика или отправителя и получателя платежа или продавца и покупателя товара или услуги, а названные кошельки представлены записями в базе данных платежной системы, где каждая из названных записей содержит, по меньшей мере, значение денежной стоимости сбережений кошелька. Неизменность покупательной способности сбережений достигается тем, что в платежной системе рассчитывают и используют стандартную стоимость товаров, услуг, платежей и сбережений кошелька, для чего любым известным способом определяют набор товаров и услуг (далее «корзина»), рассчитывают денежную стоимость одной корзины и приравнивают названную денежную стоимость одной корзины единице стандартной стоимости. Значение стандартной стоимости названных товаров, услуг, платежей и сбережений кошельков рассчитывают путем деления денежной стоимости товаров, услуг, платежей и сбережений на денежную стоимость одной корзины. Для поддержания неизменной покупательной способности сбережений рассчитывают и сохраняют в названной записи кошелька значение стандартной стоимости сбережений, а при изменении денежной стоимости названной корзины из названной записи извлекают значение стандартной стоимости сбережений и умножают названную стандартную стоимость сбережений на названную денежную стоимость корзины, а результат умножения сохраняют в названной записи в качестве нового значения денежной стоимости сбережений. Стандартная стоимость сбережений при этом оставляют неизменной. Таким образом достигается требуемый полезный эффект неизменности покупательной способности сбережений.Maintaining the constant purchasing power of savings is carried out in a payment system where the means of payment are electronic money, where the monetary value of goods, services, payments and savings is represented by the sum of electronic money, where payments are made between wallets or a lender and a borrower or a sender and a payee or a seller and a buyer goods or services, and the named wallets are represented by records in the database of the payment system, where each of the named records contains at least the value d soft cost savings purse. The invariance of the purchasing power of savings is achieved by the fact that in the payment system the standard cost of goods, services, payments and wallet savings is calculated and used, for which, by any known method, a set of goods and services is determined (hereinafter referred to as the “basket”), the monetary value of one basket is calculated and the named The monetary value of one basket is a unit of standard value. The value of the standard value of the named goods, services, payments and savings of wallets is calculated by dividing the monetary value of goods, services, payments and savings by the monetary value of one basket. To maintain the constant purchasing power of savings, the value of the standard cost of savings is calculated and stored in the named wallet record, and when the monetary value of the named basket changes, the standard value of the savings is extracted from the named record and the named standard value of the savings is multiplied by the named monetary value of the basket, and the result of multiplication is stored in named entry as the new value of the monetary value of the savings. The standard cost of savings is left unchanged. Thus, the desired beneficial effect of the invariability of the purchasing power of savings is achieved.

А для упрощения и придания планомерности процессу эмиссии и изъятия денежных единиц эмиссию и изъятие можно проводить перед проведением очередного платежа. А именно после проведения последнего платежа рассчитывают стандартную стоимость сбережений путем деления денежной стоимости сбережений на названный текущий курс обмена и до следующего платежа сохраняют значения денежной стоимости сбережений и значение рассчитанной стандартной стоимости сбережений. При этом стандартную стоимость сбережений считают до следующего платежа неизменной, а значение денежной стоимости сбережений перед проведением следующего платежа вычисляют. Для этого перед проведением следующего платежа неизменную стандартную стоимость сбережений умножают на текущий курс обмена и получают текущее значение денежной стоимости сбережений. Если текущее значение денежной стоимости сбережений выше сохраненного значения денежной стоимости сбережений, то вычисляют разницу между текущим и сохраненным значениями денежной стоимости сбережений и производят эмиссию денег в кошельке сбережений или в денежной системе на сумму названной разницы, а, если текущее значение денежной стоимости сбережений ниже сохраненного значения денежной стоимости сбережений, то вычисляют разницу между сохраненным и текущим значениями денежной стоимости сбережений и проводят изъятие денег из системы или из кошелька сбережений на сумму названной разницы.And in order to simplify and systematize the process of issue and withdrawal of monetary units, issue and withdrawal can be carried out before the next payment. Namely, after the last payment, the standard value of the savings is calculated by dividing the monetary value of the savings by the current exchange rate and until the next payment the values of the monetary value of the savings and the value of the calculated standard value of the savings are saved. In this case, the standard cost of savings is considered unchanged until the next payment, and the value of the monetary value of the savings before the next payment is calculated. To do this, before making the next payment, the constant standard cost of savings is multiplied by the current exchange rate and the current value of the monetary value of the savings is obtained. If the current value of the monetary value of the savings is higher than the stored value of the monetary value of the savings, then the difference between the current and saved values of the monetary value of the savings is calculated and money is issued in the savings wallet or in the monetary system for the amount of the mentioned difference, and if the current value of the monetary value of the savings is lower than the saved values of the monetary value of savings, then calculate the difference between the saved and current values of the monetary value of savings and withdraw money from the system we or purse savings amounting to tell the difference.

Значение стандартной стоимости сбережений изменяют при проведении платежей и так:The value of the standard cost of savings is changed when making payments and so:

- При проведении входящего платежа денежную стоимость входящего платежа делят на названную текущую денежную стоимость одной корзины, а результат деления сохраняют. Затем из записи кошелька извлекают значение стандартной стоимости сбережений кошелька и складывают его с сохраненным результатом деления, а полученный результат сложения записывают в запись кошелька в качестве нового значения стандартной стоимости сбережений.- When making an incoming payment, the cash value of the incoming payment is divided by the named current cash value of one basket, and the division result is saved. Then, the value of the standard value of the savings of the wallet is extracted from the wallet record and added to it with the saved division result, and the obtained addition result is recorded in the wallet record as the new value of the standard savings value.

- При проведении исходящего платежа денежную стоимость исходящего платежа делят на названную текущую денежную стоимость одной корзины, а результат деления сохраняют. Затем из названной записи кошелька извлекают названное значение стандартной стоимости сбережений кошелька и, если стандартная стоимость сбережений не меньше стандартной стоимости платежа, то сохраненный результат деления вычитают из значения стандартной стоимости сбережений, а полученный результат вычитания записывают в запись кошелька в качестве нового значения стандартной стоимости сбережений.- When conducting an outgoing payment, the cash value of the outgoing payment is divided by the named current cash value of one basket, and the division result is saved. Then, the named value of the standard value of the savings of the wallet is extracted from the said wallet record, and if the standard value of the savings is not less than the standard value of the payment, the saved division result is subtracted from the value of the standard cost of savings, and the obtained subtraction result is written into the wallet record as the new value of the standard cost of savings .

Для удобства фиатами или фиатными валютами станем называть традиционные валюты, которые циркулируют в денежных системах различных государств и эмитируются центральными банками соответствующих стран. Примером фиатов являются рубль, доллар, евро и другие традиционные валюты мира. В отличие от фиатов криптовалюты мы продолжим называть крипто валютами.For convenience, we will call fiat or fiat currencies the traditional currencies that circulate in the monetary systems of various states and are issued by the central banks of the respective countries. Examples of fiats are the ruble, dollar, euro and other traditional currencies of the world. Unlike cryptocurrency fiats, we will continue to call crypto currencies.

Для расчета стоимости денежной единицы или стоимости стандартной единицы денежной системы в фиатных денежных единицах (доллары США, Евро, Рубли и прочее) или в денежных единицах криптовалют (биткоины, эфиры и прочее) система может использовать котировки соответствующих курсов обмена, которые может получать как результат торгов парами деньги/фиат на денежных рынках и биржах обмена. Стоимость стандарта (1std) в денежных единицах денежной системы и в фиатных денежных единицах в каждый момент времени определяется с помощью кросс курса стандарт/деньги. Кросс-курс обмена стандарты/деньги определяют, исходя из принципа поддержания покупательной способности одного стандарта неизменно равной стоимости одной корзины, соответственно кросс курс стоимости стандарта в денежных единицах изменяют прямо пропорционально изменению стоимости одной корзины, также выраженной в денежных единицах.To calculate the value of a monetary unit or the value of a standard unit of a monetary system in fiat currency units (US dollars, Euros, Rubles, etc.) or in cryptocurrency monetary units (bitcoins, ethers, etc.), the system can use quotes of the corresponding exchange rates, which can be obtained as a result trading in money / fiat pairs in money markets and exchange exchanges. The cost of a standard (1std) in monetary units of the monetary system and in fiat currency units at each moment of time is determined using the standard / money cross rate. The cross rate of exchange of standards / money is determined on the basis of the principle of maintaining the purchasing power of one standard invariably equal to the cost of one basket; accordingly, the cross rate of the standard cost in monetary units is changed directly proportional to the change in the value of one basket, also expressed in monetary units.

Для расчета фиатной стоимости стандартов, денежная система также может использовать Индекс Потребительских Цен или ИПЦ (Consumer Price Index или CPI) и Стоимость Потребительской Корзины Товаров и Услуг («корзины»), публикуемые финансовыми властями различных стран, например https://tradingeconomics.com/united-states/consumer-price-index-cpi. или определенные другим способом (например, с помощью краудсорсинга - crowdsourcing) или полученные из другого источника.To calculate the fiat value of standards, the monetary system can also use the Consumer Price Index or CPI and the Consumer Basket of Goods and Services (“baskets”) published by the financial authorities of various countries, for example https://tradingeconomics.com / united-states / consumer-price-index-cpi. or defined in another way (for example, using crowdsourcing) or obtained from another source.

Как показано выше, при изменении Индекса Потребительских Цен и с ним денежной стоимости потребительской корзины товаров и услуг, стандартная стоимость сбережений и стандартная стоимость кошелька, остаются неизменными, что позволяет добиться требуемого эффекта стабилизации стоимости сбережений.As shown above, with a change in the Consumer Price Index and with it the monetary value of the consumer basket of goods and services, the standard cost of savings and the standard cost of the wallet remain unchanged, which allows to achieve the desired effect of stabilizing the cost of savings.

Технический результат, который позволяет достигнуть настоящее изобретение, заключается в том, что в условиях изменения покупательной способности денежной единицы дополнительная эмиссия и добавление денежных единиц в кошелек сбережений или изъятие денежных единиц из кошелька сбережений позволяет сохранить покупательную способность сбережений кошелька неизменной, что в свою очередь позволяет устранить влияние изменения покупательной способности денег на торговлю, а также избежать утраты людьми и предприятиями части покупательной способности своих сбережений и оборотных средств. Таким образом технический результат настоящего изобретения позволяет повысить надежность хранения сбережений в платежной системе, устранив изменение их покупательной способности, которому подвержены сбережения номинированные в любых известных фиатных деньгах или криптовалюте.The technical result that the present invention allows to achieve is that in the conditions of a change in the purchasing power of a monetary unit, additional issue and addition of monetary units to a savings wallet or withdrawal of monetary units from a savings wallet allows maintaining the purchasing power of the wallet's savings unchanged, which in turn allows eliminate the influence of changes in the purchasing power of money on trade, and also avoid the loss by people and enterprises of part of the purchasing power the benefits of their savings and working capital. Thus, the technical result of the present invention allows to increase the reliability of storage of savings in the payment system, eliminating the change in their purchasing power, which affects the savings denominated in any known fiat money or cryptocurrency.

Еще одним полезным эффектом изобретения является отсутствие рисков потери стоимости сбережений в случае скоординированных атак на денежную единицу системы посредством валютных интервенций, так как интервенция приведет к увеличению или уменьшению стоимости денежной единицы системы и, как следствие, к такой дополнительной эмиссии или изъятию денег в кошельках со сбережениями, что позволит поддерживать определенную или неизменную стоимость стандарта, и/или совокупную стандартную стоимость денежной системы, и/или денежную стоимость системы, и/или денежную сумму системы, и/или стандартную сумму системы.Another useful effect of the invention is the absence of risks of loss of the cost of savings in the case of a coordinated attack on the monetary unit of the system through currency interventions, since the intervention will increase or decrease the value of the monetary unit of the system and, as a result, such additional issue or withdrawal of money in wallets with savings, which will allow to maintain a certain or constant value of the standard, and / or the total standard value of the monetary system, and / or the monetary value of threads and / or the amount of money the system, and / or a standard function of the system.

В некоторых исполнениях денежной системы, настоящее изобретение дает возможность использования технологии блокчейна и «умных» контрактов (smart contract) для эмиссии «умных» денег, которые способны использовать кросс курс стандарт/деньги системы для изменения денежной суммы платежей и/или сбережений/кошельков системы на величину, которая требуется для поддержания стоимости сбережений/кошельков неизменной в стандартных единицах std.In some versions of the monetary system, the present invention makes it possible to use blockchain technology and smart contracts to issue “smart” money that can use the system’s standard / money cross rate to change the monetary amount of payments and / or savings / wallets of the system by the amount required to maintain the cost of savings / wallets unchanged in standard std units.

Одним из форм выпуска электронных денег являются крипто валюты и токены умных контрактов. Токены умных контактов, содержащие компьютерную программу, позволяют токену взаимодействовать с другими токенами и с компьютерами инфраструктуры денежной системы с целью принятия решения о мерах по поддержанию стабильности стандартной стоимости std в системе. При снижении стоимости одного токена, токены кошелька возможно смогут «клонировать» себя, чтобы увеличить число токенов в кошельке, а при увеличении стоимости токена «уничтожать» избыточные токены кошелька оставляя стандартную стоимость кошелька между операциями оплаты неизменной. Далее физические носители денежной стоимости в системе мы станем называть токенами. Настоящее изобретение предлагает в качестве физического носителя денежной стоимости использовать токены или умные токены. Стоимость токена к фиатным валютам и к корзине может меняться.One of the forms of issuing electronic money is cryptocurrencies and smart contract tokens. Smart contact tokens containing a computer program allow the token to interact with other tokens and computers in the money system infrastructure in order to decide on measures to maintain the stability of the standard cost of std in the system. With a decrease in the cost of one token, wallet tokens will probably be able to “clone” themselves to increase the number of tokens in the wallet, and with an increase in the cost of the token, they will “destroy” excess wallet tokens, leaving the standard wallet cost unchanged between payment operations. Further, we will call physical carriers of monetary value in the system tokens. The present invention proposes to use tokens or smart tokens as a physical medium of monetary value. The cost of the token to fiat currencies and to the basket may vary.

Предлагаемая настоящим изобретением стандартная денежная система направлена на управление покупательной способностью сбережений, а не на поддержание курса обмена денежных единиц друг к другу. Тем не менее предпочтительным является исполнение системы, направленное на поддержание неизменной стандартной стоимости сбережений.The standard monetary system proposed by the present invention is aimed at managing the purchasing power of savings, and not at maintaining the exchange rate of monetary units to each other. Nevertheless, it is preferable to implement a system aimed at maintaining a constant standard cost of savings.

Механизм консенсуса и «доказательство стандартной стоимости»Consensus Mechanism and “Proof of Standard Cost”

В отличие от известных систем криптовалют, ориентированных только на эмиссию криптовалюты, предлагаемая стандартная платежная система допускает как эмиссию, так и изъятие денежной стоимости из системы. Поэтому механизмом достижения консенсуса не могут быть известные механизмы Proof-Of-Work, Proof-Of-Stake или другие известные.Unlike the well-known cryptocurrency systems focused only on the issue of cryptocurrency, the proposed standard payment system allows for both the issue and withdrawal of monetary value from the system. Therefore, the mechanism of consensus cannot be the well-known mechanisms of Proof-Of-Work, Proof-Of-Stake or other well-known.

Как было показано выше, механизм эмиссии или изъятия денежной стоимости в стандартной платежной системе обеспечивает неизменность стандартной стоимости сбережений. Поэтому безопасность стандартной платежной системы зависит от целостности данных о стандартной стоимости сбережений и достоверном подтверждении стандартной стоимости кошелька. Такой механизм консенсуса для простоты можно назвать «доказательством стоимости» или Proof-Of-Value (POV).As shown above, the mechanism for issuing or withdrawing monetary value in a standard payment system ensures that the standard cost of savings remains unchanged. Therefore, the security of a standard payment system depends on the integrity of the data on the standard cost of savings and reliable confirmation of the standard cost of the wallet. For simplicity, such a consensus mechanism can be called “proof of value” or Proof-of-Value (POV).

Эмиссия и изъятие денежной ликвидности в системеIssue and withdrawal of cash liquidity in the system

Как уже отмечалось выше, при увеличении денежной стоимости корзины, денежные суммы кошельков должны увеличиваться для поддержания стандартной стоимости кошелька неизменной, а эмитированные для этого дополнительные денежные единицы зачисляются в кошелек. По правилам бухгалтерского учета движение денег должно осуществляться двойной записью: счет донора откуда были изъяты деньги и счет получателя куда деньги поступили, поэтому пополнение сбережений кошелька дополнительной суммой денег может потребовать наличия кошелька или кошельков-доноров, а также оформления платежной операции для перечисления изъятой суммы из кошелька донора в кошелек получателя. При увеличении повышении денежной стоимости корзины, денежные суммы кошельков должны уменьшаться, и поэтому избыточные денежные единицы кошелька или должны уничтожаться, или должны быть зачислены в специальный кошелек или группу кошельков системы, которые накапливают избыточную денежную ликвидность системы. Назовем такой один или несколько кошельков «кошельками ликвидности». Кошелек-донор или кошелек ликвидности может как накапливать изъятую денежную ликвидность, так и возвращать эту ликвидность в денежную систему или ее кошельки. Предпочтительным является исполнение системы, в которой существует, по меньшей мере, один кошелек ликвидности. Другим предпочтительным исполнением системы является исполнение системы, в которой для каждого кошелька, поддерживающего покупательную способность сбережений, дополнительно создан один кошелек ликвидности.As already noted above, with an increase in the monetary value of the basket, the wallets should increase in order to keep the standard value of the wallet unchanged, and additional monetary units issued for this will be credited to the wallet. According to the accounting rules, the movement of money should be done in double entry: the donor account where the money was taken from and the recipient's account where the money came from, so replenishing wallet savings with an additional amount of money may require the presence of a wallet or donor wallets, as well as processing a payment transaction to transfer the withdrawn amount from donor wallet to recipient wallet. With an increase in the increase in the monetary value of the basket, the wallets' monetary amounts should decrease, and therefore the excess monetary units of the wallet either must be destroyed or must be credited to a special wallet or group of wallets of the system that accumulate excess monetary liquidity of the system. We call such one or several wallets “liquidity wallets”. A donor wallet or liquidity wallet can either accumulate withdrawn cash liquidity or return this liquidity to the monetary system or its wallets. It is preferable to execute a system in which at least one liquidity wallet exists. Another preferred embodiment of the system is the execution of a system in which for each wallet that supports the purchasing power of savings, an additional liquidity wallet is created.

Предпочтительно денежная эмиссия или денежное изъятие в кошельке происходит непосредственно перед новым платежом за период после последнего проведенного кошельком платежа.Preferably, the money issue or withdrawal in the wallet occurs immediately before the new payment for the period after the last payment made by the wallet.

Рассмотрим подробнее процесс эмиссии и изъятия денег из обращения в стандартной денежной системе, предлагаемой изобретением. Стандартная денежная система обеспечивает эмиссию и изъятие части денег для поддержания неизменной стоимости сбережений/кошельков в единицах std. Эмиссия и изъятие денег в системе может быть как централизованной, так и децентрализованной. Поскольку между платежами стандартная стоимость кошелька не меняется, то пересчитывать денежную стоимость сбережений в кошельке можно только перед проведением очередного входящего или исходящего платежка такого кошелька. Тем не менее увеличивать или уменьшать денежную стоимость кошельков для приведения денежной стоимости кошелька в соответствие с их стандартной стоимостью можно и между платежами.Let us consider in more detail the process of emission and withdrawal of money from circulation in the standard monetary system proposed by the invention. The standard monetary system provides the issue and withdrawal of part of the money to maintain the constant value of savings / wallets in units of std. The issue and withdrawal of money in the system can be both centralized and decentralized. Since the standard value of the wallet does not change between payments, it is possible to recalculate the monetary value of the savings in the wallet only before the next incoming or outgoing payment of such a wallet. Nevertheless, it is possible to increase or decrease the monetary value of wallets in order to bring the monetary value of the wallet in accordance with their standard value between payments.

Рассмотрим изменение денежной стоимости сбережений кошелька за некоторый период, в течении которого стандартная стоимость сбережений кошелька оставалась неизменной. При расчете учтем тот факт, что в современном мире стоимость корзины определена в фиатных деньгах. Предположим, что с момента времени 1 стандартная стоимость кошелька не менялась до момента времени 2. Причем момент времени 1 может быть временем после проведения последнего платежа кошелька, а момент времени 2 моментом, когда готовится новый платеж кошелька. Тогда денежная стоимость сбережений кошелька в момент времени 2 будет:Consider the change in the monetary value of the wallet’s savings over a period during which the standard value of the wallet’s savings remained unchanged. When calculating, we take into account the fact that in the modern world the cost of a basket is determined in fiat money. Suppose that from time 1, the standard value of the wallet has not changed until time 2. Moreover, time 1 can be the time after the last payment of the wallet, and time 2 can be the moment when a new wallet payment is being prepared. Then the monetary value of the wallet’s savings at time 2 will be:

где T1 и T2 - курс денежных единиц системы к фиатным деньгам в моменты времени 1 и 2where T 1 and T 2 - the currency of the system units to fiat money at time points 1 and 2

N1 и N2 - денежная стоимость кошелька в моменты времени 1 и 2N 1 and N 2 - the monetary value of the wallet at time points 1 and 2

NP - денежная стоимость платежа, которая вычитается (-) в случае исходящего и прибавляется (+) в случае входящего платежа;N P is the monetary value of the payment, which is deducted (-) in the case of outgoing and added (+) in the case of incoming payment;

F1 и F2 - фиатная стоимость одной корзины (фиатная стоимость одного std) в момент времени 1 и 2.F 1 and F 2 - the fiat value of one basket (the fiat value of one std) at time 1 and 2.

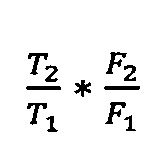

По сути в вышеприведенной формуле расчета N2 группа

![]()

![]()

При централизованной эмиссии и/или изъятии, эмиссией и/или изъятием занимаются один или группа кошельков ликвидности платежной системы. При децентрализованной эмиссии и изъятии избыточная и добавочная ликвидности эмитируются или поглощаются специальным кошельком ликвидности, который является дополнительным кошельком каждого пользователя. При децентрализованной эмиссии/изъятии можно также использовать умные контракты, которые будут использовать процедуру Proof-Of-Value (POV) - доказательство стандартной стоимости сбережений для целей эмиссии или изъятия денежной стоимости из умных контрактов.In case of centralized issue and / or withdrawal, one or a group of payment system liquidity wallets are engaged in issue and / or withdrawal. In case of decentralized issue and withdrawal, excess and additional liquidity are issued or absorbed by a special liquidity wallet, which is an additional wallet for each user. With decentralized issuance / withdrawal, you can also use smart contracts that will use the Proof-Of-Value (POV) procedure - proof of the standard cost of savings for the purpose of emission or withdrawal of monetary value from smart contracts.

Осуществление платежейMaking payments

Как говорилось выше, платежи в системе номинированы, по меньшей мере, в денежных единицах. Поэтому при проведении платежа из кошелька, номинированного, по меньшей мере, в стандартных единицах, может оказаться необходимо определить число денежных единиц соответствующих сумме платежа в стандартных единицах с использованием стандартного курса - содержания денежных единиц в одной стандартной. Зачисление платежа может проходить или в валюте платежа или в выбранной валюте, однако, если скорость платежей в системе ниже скорости изменения курса стандарта в единицах денежной стоимости системы (имеется в виду содержания денежных единиц в одной стандартной единице), то это может накладывать валютные риски на стороны проведения платежа, поскольку стандартная стоимость платежа представленного денежной стоимостью может меняться в процессе проведения платежа. Для исключения валютных рисков платежи между кошельками системы могут проводиться в стандартных единицах. Другим способом снижения названных рисков является использование технологий ускоряющих срок проведения платежа.As mentioned above, payments in the system are denominated, at least in monetary units. Therefore, when making a payment from a wallet nominated at least in standard units, it may be necessary to determine the number of monetary units corresponding to the payment amount in standard units using the standard rate — the content of monetary units in one standard. A payment can be credited either in the payment currency or in the chosen currency, however, if the payment rate in the system is lower than the rate of change of the standard exchange rate in units of the monetary value of the system (meaning the content of monetary units in one standard unit), this may impose currency risks on parties of the payment, since the standard value of the payment represented by the monetary value may change during the payment process. To eliminate currency risks, payments between system wallets can be carried out in standard units. Another way to reduce these risks is to use technologies that accelerate the payment term.

Биржевые торги денежной единицей системыExchange trading in the monetary unit of the system

Денежные единицы системы могут быть представлены носителями - токенами системы, а стандартная стоимость не имеет носителей и представлена в системе механизмом консенсуса Proof-Of-Value - POV. Поэтому на валютных биржах денежные единицы системы могут продаваться с плавающим курсом (плавающая фиатная стоимостью за один токен системы), а фиатная стоимость стандартной единицы системы на биржах торговаться не может, потому что в реальном мире эквивалентом стандартной стоимости является корзина, чья фиатная стоимость в реальном мире существует независимо от стандартной денежной системы и не связана с созданием и деятельностью стандартной денежной системы или ее виртуальной стандартной единицей стоимости. Попытка биржевой торговли единицами стандартной стоимости системы приведет к биржевой торговле котировками фиатной стоимости корзины, что связано с торговлей покупательной способностью фиатной валюты и не имеет смысла в реальном мире.Monetary units of the system can be represented by carriers - system tokens, and the standard cost does not have carriers and is represented in the system by the Proof-Of-Value consensus mechanism - POV. Therefore, on currency exchanges, the monetary units of the system can be sold at a floating rate (floating fiat value for one system token), and the fiat value of a standard unit of the system on exchanges cannot be traded, because in the real world the equivalent of the standard value is a basket whose fiat value in real the world exists independently of the standard monetary system and is not associated with the creation and operation of a standard monetary system or its virtual standard unit of value. An attempt to exchange trading units of the standard cost of the system will lead to exchange trading in quotes of the fiat value of the basket, which is associated with trading in the purchasing power of fiat currency and does not make sense in the real world.

В случае, если стандартная денежная система станет доминирующей платежной системой в мире, то стандартная стоимость торговаться на биржах также не сможет, потому что в стандартной платежной системе единица стандартной стоимости по определению должна оставаться неизменной.In the event that the standard monetary system becomes the dominant payment system in the world, the standard value will not be able to trade on exchanges either, because in the standard payment system the unit of standard value by definition must remain unchanged.

Распределенный реестр операций (блокчейн)Distributed operations registry (blockchain)

Если платежи производятся в крипто валюте с использованием технологии блокчейн, то реализация расчета N2 должна проводиться в момент расчета очередного блока или в другое время, удобное с точки зрения архитектуры или правил денежной системы.If payments are made in cryptocurrency using blockchain technology, then the implementation of calculation No. 2 should be carried out at the time of calculating the next block or at another time convenient from the point of view of the architecture or rules of the monetary system.

Блокчейном может быть представлен как реестр операций всей системы, так и реестр операции конкретного кошелька или группы кошельков. Механизм достижения консенсуса и защиты транзакций в платежной системе может быть реализован любым из известных способов или новым способом. Предпочтительным способом реализации консенсуса, как было сказано выше, является новый механизм Proof-Of-Value (POV).Blockchain can be represented as a registry of operations of the entire system, and a registry of operations of a particular wallet or group of wallets. The mechanism of consensus building and transaction protection in the payment system can be implemented in any of the known ways or in a new way. The preferred way to implement consensus, as mentioned above, is the new Proof-Of-Value (POV) mechanism.

Поскольку стоимость денежных единиц (токенов) и поддержание стабильной их стоимости не является задачей системы, то концепция временной стоимости денег в отношении стоимости токенов также теряет смысл. В стандартной системе можно говорить лишь о временной стоимости стандарта стоимости и его изменении в некоторых случаях. Тем не менее в стандартной системе можно реализовать займы и выплату процентов по ним, а также можно реализовать изъятие части денежной ликвидности в размере отрицательной ставки, что позволяет, например, взимать налоги.Since the value of monetary units (tokens) and maintaining a stable value are not the task of the system, the concept of the time value of money in relation to the value of tokens also loses its meaning. In the standard system, we can only talk about the time value of the standard value and its change in some cases. Nevertheless, in the standard system, you can realize loans and pay interest on them, and you can also implement the withdrawal of part of the cash liquidity in the amount of a negative rate, which allows, for example, to levy taxes.

Отрицательная и положительная ставка накоплений.Negative and positive rate of savings.

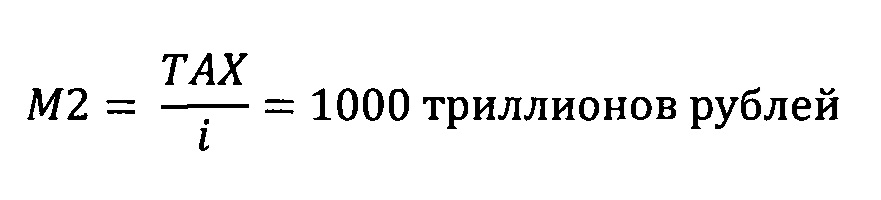

Практический интерес к внедрению отрицательной ставки в денежной системе продиктован тем, что отрицательной ставкой <i> можно автоматизировать сбор части налогов, что позволяет избавиться от расходов на содержание фискальных органов. Для сбора налогов TAX необходимо, чтобы объем денежной массы <наличные + средства на расчетных и текущих банковских счетах + срочные вклады > (денежный агрегат М2) удовлетворял условию:The practical interest in introducing a negative rate in the monetary system is dictated by the fact that a negative rate <i> can automate the collection of taxes, which eliminates the cost of maintaining fiscal authorities. To collect TAX taxes, it is necessary that the money supply <cash + funds in current and current bank accounts + time deposits> (money aggregate M2) satisfy the condition:

![]()

![]()

Так, например, если необходимо собирать 100 триллионов рублей налогов в год при ставке рефинансирования равной -10%, то объем денежной массы М2, находящейся в обращении, должен быть равен:So, for example, if it is necessary to collect 100 trillion rubles of taxes per year at a refinancing rate of -10%, then the volume of money supply M2 in circulation should be equal to:

При этом объем наличных денег (денежный агрегат М0) желательно свести к нулю, то есть денежный агрегат М0 в агрегате М2 желательно иметь равным нулю, потому, что невозможно уменьшить на i номинальную стоимость бумажной купюры не вводя купоны, что практически слабо осуществимо.At the same time, it is desirable to reduce the amount of cash (money aggregate M0) to zero, that is, it is desirable to have the money aggregate M0 in aggregate M2 equal to zero, because it is impossible to reduce the nominal value of a paper note by i without entering coupons, which is almost poorly feasible.

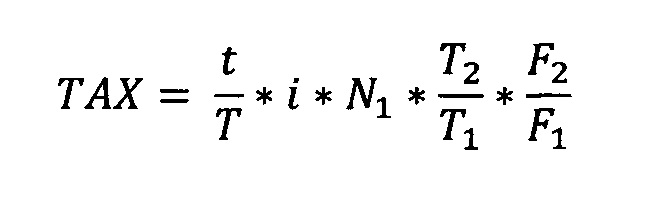

Настоящее изобретение предполагает возможность автоматического временного уменьшения суммы S стандартных единиц, находящейся в кошельке за время t (в единицах системного времени) между двумя последовательными входящими или исходящими платежами кошелька, то есть пока сумма S стандартных единиц кошелька была неизменной, налог TAX за время t:The present invention suggests the possibility of automatically temporarily reducing the amount S of standard units in the wallet during time t (in units of system time) between two consecutive incoming or outgoing wallet payments, that is, while the sum S of standard wallet units was unchanged, TAX tax for time t:

![]()

![]()

где T - количество системного времени в одном году.where T is the amount of system time in one year.

Учитывая, что сумма S стандартных единиц стоимости кошелька в момент времени 1 равнялась сумме N1 денежных единиц системы, а в момент времени 2 представлена суммой ![]()

![]()

Положительная ставка накоплений может использоваться системой с целью технологической поддержки процесса кредитования, при котором заимодавец и заемщик вступают в сделку, возможно представленную «умным контрактом», при которой заимодавец перечисляет заемщику сумму займа, выраженную в денежных единицах системы или в единицах потребительской стоимости системы, или в единицах потребительской стоимости кошелька заимодавца, или в единицах потребительской стоимости кошелька заемщика, если названные единицы отличаются из-за скорости проведения операций в системе или по другим причинам. Начисление процентов PLUS по кредиту может исчисляться по формуле аналогичной формуле исчисления налогов:A positive savings rate can be used by the system for the technological support of the lending process, in which the lender and the borrower enter into a transaction, possibly represented by a “smart contract”, in which the lender transfers to the borrower the loan amount expressed in monetary units of the system or in units of the consumer value of the system, or in units of the consumer value of the lender's wallet, or in units of the consumer value of the borrower's wallet, if the named units differ due to the speed of conducting operations in the system or for other reasons. The accrual of PLUS interest on a loan can be calculated using a formula similar to the tax calculation formula:

где n - сумма денежных единиц по начисленным процентам за период системного времени t;where n is the sum of monetary units for accrued interest for the period of system time t;

Т - количество системного времени в одном году.T is the amount of system time in one year.

Claims (13)

Priority Applications (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| RU2017131390A RU2673399C1 (en) | 2017-09-07 | 2017-09-07 | Method of preserving savings purchasing ability |

Applications Claiming Priority (1)

| Application Number | Priority Date | Filing Date | Title |

|---|---|---|---|

| RU2017131390A RU2673399C1 (en) | 2017-09-07 | 2017-09-07 | Method of preserving savings purchasing ability |

Publications (1)

| Publication Number | Publication Date |

|---|---|

| RU2673399C1 true RU2673399C1 (en) | 2018-11-26 |

Family

ID=64556524

Family Applications (1)

| Application Number | Title | Priority Date | Filing Date |

|---|---|---|---|

| RU2017131390A RU2673399C1 (en) | 2017-09-07 | 2017-09-07 | Method of preserving savings purchasing ability |

Country Status (1)

| Country | Link |

|---|---|

| RU (1) | RU2673399C1 (en) |

Cited By (3)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| RU2731417C1 (en) * | 2018-12-28 | 2020-09-02 | Алибаба Груп Холдинг Лимитед | Parallel execution of transactions in network of blockchains based on white lists of smart contracts |

| RU2741279C2 (en) * | 2019-04-01 | 2021-01-22 | Рафик Равильевич Сингатуллин | Method of performing task in computer system |

| US11132676B2 (en) | 2018-12-28 | 2021-09-28 | Advanced New Technologies Co., Ltd. | Parallel execution of transactions in a blockchain network |

Citations (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| WO2001057616A2 (en) * | 2000-02-04 | 2001-08-09 | Xpenswise.Com, Inc. | System and method for dynamic price setting and facilitation of commercial transactions |

| EA008185B1 (en) * | 2006-01-23 | 2007-04-27 | Общество С Ограниченной Ответственностью «Интерактивная Мобильная Процессинговая Компания "Мегапэй"» | Method for performing off financial transaction (variants) |

| EA011308B1 (en) * | 2004-03-05 | 2009-02-27 | Н. Калеб Эйвери | Method and system for optimal pricing and allocation |

| US7685021B2 (en) * | 2005-10-21 | 2010-03-23 | Fair Issac Corporation | Method and apparatus for initiating a transaction based on a bundle-lattice space of feasible product bundles |

| WO2014071338A2 (en) * | 2012-11-05 | 2014-05-08 | Mastercard International Incorporated | Electronic wallet apparatus, method, and computer program product |

-

2017

- 2017-09-07 RU RU2017131390A patent/RU2673399C1/en active

Patent Citations (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| WO2001057616A2 (en) * | 2000-02-04 | 2001-08-09 | Xpenswise.Com, Inc. | System and method for dynamic price setting and facilitation of commercial transactions |

| EA011308B1 (en) * | 2004-03-05 | 2009-02-27 | Н. Калеб Эйвери | Method and system for optimal pricing and allocation |

| US7685021B2 (en) * | 2005-10-21 | 2010-03-23 | Fair Issac Corporation | Method and apparatus for initiating a transaction based on a bundle-lattice space of feasible product bundles |

| EA008185B1 (en) * | 2006-01-23 | 2007-04-27 | Общество С Ограниченной Ответственностью «Интерактивная Мобильная Процессинговая Компания "Мегапэй"» | Method for performing off financial transaction (variants) |

| WO2014071338A2 (en) * | 2012-11-05 | 2014-05-08 | Mastercard International Incorporated | Electronic wallet apparatus, method, and computer program product |

Cited By (5)

| Publication number | Priority date | Publication date | Assignee | Title |

|---|---|---|---|---|

| RU2731417C1 (en) * | 2018-12-28 | 2020-09-02 | Алибаба Груп Холдинг Лимитед | Parallel execution of transactions in network of blockchains based on white lists of smart contracts |

| US10911461B2 (en) | 2018-12-28 | 2021-02-02 | Advanced New Technologies Co., Ltd. | Parallel execution of transactions in a blockchain network based on smart contract whitelists |

| US11132676B2 (en) | 2018-12-28 | 2021-09-28 | Advanced New Technologies Co., Ltd. | Parallel execution of transactions in a blockchain network |

| US11381573B2 (en) | 2018-12-28 | 2022-07-05 | Advanced New Technologies Co., Ltd. | Parallel execution of transactions in a blockchain network based on smart contract whitelists |

| RU2741279C2 (en) * | 2019-04-01 | 2021-01-22 | Рафик Равильевич Сингатуллин | Method of performing task in computer system |

Similar Documents

| Publication | Publication Date | Title |

|---|---|---|

| RU2673399C1 (en) | Method of preserving savings purchasing ability | |

| Dark et al. | Stablecoins: Market developments, risks and regulation | |

| Nyambuu et al. | Globalization, gating, and risk finance | |

| Follain et al. | The unbundling of residential mortgage finance | |

| Grasselli et al. | Cryptocurrencies and the future of money | |

| Yuryevna et al. | Risk management of derivative financial instruments | |

| Yano | Theory of money: from ancient Japanese copper coins to virtual currencies | |

| US20220222658A1 (en) | Currency value management system and currency value management program | |

| DAHAL et al. | An analysis of the exchange rate regime of Nepal: Determinants and inter-dynamic relationship with macroeconomic fundamentals | |

| Senner et al. | Explaining global imbalances: the role of central-bank intervention and the rise of sovereign wealth funds | |

| Bacchetta | The sovereign money initiative in Switzerland: An assessment | |

| Drigă | The role of the banking system in the sustainable development of the economy | |

| Li | The Problems of Current International Monetary System | |

| LOTFI et al. | Bank liquidity risk in participatory banks. Which perspectives for Moroccan market? | |

| Michail | A Brief History of Money and Credit | |

| Prasetyowati et al. | Zakah Economic Concept in the Determination of Pricing on Islamic Banking Products | |

| Gizycki et al. | Contingent Claim Model of a Bank| RDP 9302: A Decade of Australian Banking Risk: Evidence from Share Prices | |

| Walton | Yield generation using decentralized financial (DeFi) applications | |

| Boudir et al. | Taking financial intermediation back to its original functions and activities | |

| Bacchetta | The sovereign money initiative in Switzerland: an economic assessment | |

| Dark et al. | Stablecoins: Market Developments, Risks and Regulation| Bulletin–December 2022 | |

| Huber | Three-Tier Monetary System. Types of Money, Their Creation and Circulation | |

| Russo | Debt, bubble policy, and the role of the repo market in the Federal Reserve’s management of capitalism in crisis | |

| Sadeghi et al. | Financial Markets and Speculative Motivations | |

| Havryliuk | M. Shevchenko, PhD in Economics, Associate Professor, Associate Professor of the Department of Accounting and Finance, National Technical University" Kharkov Polytechnic Institute" ORCID ID: https://orcid. org/0000-0003-2165-9907 |