Detailed Description

The technical solutions in the embodiments of the present application will be clearly and completely described below with reference to the drawings in the embodiments of the present application, and it is obvious that the described embodiments are only a part of the embodiments of the present application, and not all of the embodiments. All other embodiments obtained by a person of ordinary skill in the art based on the embodiments in the present application without making any creative effort belong to the protection scope of the present application.

As shown in fig. 1, fig. 1 is a schematic flow chart of an embodiment of the evaluation method of the insurance product of the present application. The method comprises the following steps:

step 101: and acquiring the marked insurance product.

Wherein, the marked information comprises the marks of the types and the quality of all guarantees or responsibilities of the insurance product. Generally, each insurance product has many terms, so that corresponding guarantees and responsibilities are also many, and in order to completely embody the quality or cost performance of the insurance product in the same type of products, the type and quality of each guarantee or responsibility of the insurance product are labeled. Wherein, marking the quality comprises marking the quality score or marking the quality annotation. And then, acquiring the quality grade of each guarantee or responsibility of the insurance product according to the quality label. Specifically, the quality grade may be obtained by grade distribution of the labeled quality score, or may be obtained by grade classification according to the quality annotation, which is not limited herein. Generally, a quality class includes a fractional segment, for example, 60 or less is D, 60 to 70 are C, 71 to 80 are B, and 81 to 100 are a.

Wherein, the marking of each guarantee or responsibility of the insurance product can be manually marked. Or labeling may be performed by a labeling model first and then by a manual verification, which is not limited herein.

Step 102: and distributing the guarantees or responsibilities with the same labeling type and quality grade of different insurance products to the same group, and calculating to obtain the percentage grade of each guarantee or responsibility in the same group.

Wherein the insurance products can be different types of insurance products. However, in order to provide contrast of insurance products of the same type and improve the practicability of the evaluation method, it is preferable that different insurance products in the present embodiment refer to insurance products of the same type, such as child insurance or old care insurance.

Since many original values of quality of guarantee or responsibility of the insurance product, such as scores, do not have continuity and are not suitable for being directly evaluated by the standard score, the percentage grade is firstly converted into the continuous variable in the embodiment and then evaluated by the standard score method.

As shown in fig. 2, fig. 2 is a flowchart illustrating an embodiment of step 102, which includes:

step 1021: and distributing the same-grade guarantees or responsibilities of the same labeling type of different insurance products to the same group, and calculating to obtain the percentile of each guarantee or item in the same group.

Generally, the same dimension terms of the same type of insurance products, namely, the responsibilities and the contents of the guarantee of the same labeling type are basically the same and different, and the difference is generally in the size of the guarantee range, the amount of the guarantee or the severity of the conditions during reimbursement and the like. The same guarantee or responsibility of the same type of insurance products is compared independently, so that a reference for a certain independent guarantee or responsibility can be provided for a user, and a reference is also provided for the subsequent calculation of the quality of the insurance products.

Specifically, in this embodiment, the number of guarantees or responsibilities of all the same labeling types of the dimension, i.e. the number of samples N, is counted first R . Then from the insurance productOr the responsibility marking, a quality marking is obtained, such as a score or a grade annotation, such as optimal, worst and the like, and the grade of each guarantee or responsibility in the dimension is determined according to the quality, such as the grade of the score, according to a preset grade setting rule, such as one of the four grades A, B, C, D in the above example.

Assigning guarantees or responsibilities with the same labeling type and quality grade to the same group, ordering the actual labeling quality or the quality of specific content in the same group, and assigning a grade R in the group G . And counting according to the number of samples of the guarantee or responsibility in the group to obtain the level R of the guarantee or responsibility in the group G Percentile P of G 。

For example, if there are 4000 insurance products of the same type, such as a major risk, the total number of samples N for the insurance products is 4000. The 4000 critical care or liability may include A, B, C, D of the label types, each of which is N R . And the guarantee or responsibility marked with the type A is divided into three levels of 3 a, b and c, so that the guarantee or responsibility marked with the type A is divided into a group as the guarantee or responsibility of the level a, is divided into a group as the guarantee or responsibility of the level b, and is divided into a group as the guarantee or responsibility of the level c. The 200 guarantees or responsibilities in the a level can be graded or sorted again by the marked evaluation scores or the mode of manually judging the actual content quality, and preferably, the quality sorting of the guarantees or responsibilities is sorted in a descending order. According to the level of each guarantee or liability in the group, i.e. R G And through R G Calculating to obtain a percentile P G 。

Step 1022: the percentile rating for each guarantee or liability is obtained based on the percentile and the number of samples of the insurance product.

Wherein, the percentage grade refers to the percentage of the number of times of scores lower than a certain preset score to the total number of times in a numerical sequence arranged according to the size sequence.

Specifically, the percentage grade P is calculated by the following formula R 。

Where N is the total number of samples of insurance products, such as the total number of samples 4000 for the above-mentioned critical risks.

cf L The guarantees or responsibilities for the same group correspond to the cumulative number of samples of the level before the level, for example, the guarantees or responsibilities with the label type A are classified into a group for the level a guarantees or responsibilities, and the group comprises 200 items of guarantees or responsibilities of three levels (1), (2) and (3). Level (1) is 100 items, level (2) is 30 items, level (3) is 70 items, and level (1) is higher than level (2) and level (2) is higher than level (3). When the percentage rating of the rating (1) is calculated, the cumulative sample number is 100 items of the cumulative sample number, when the percentage rating of the rating (2) is calculated, the cumulative sample number is 100 items of the rating (1), and when the percentage rating of the rating (3) is calculated, the cumulative sample number is the sum of the samples of the rating (1) and the rating (2), and the cumulative sample number is 130 items.

P GL The lower limit of the percentile in the same group, for example, the grade (3) has the lowest grade, and the corresponding percentile is the lowest grade, at this time, the lower limit of the percentile is the percentile of the grade (3).

i is a percentage scale of the intra-group distance, e.g. 1% or 2% or other values such as 5%. For example, for the class of car insurance, some are full reimbursements, some are 90% reimbursements, and some are 80% reimbursements. Some reimbursement ratios are 85%, but all are in the grade of 80% -90%, the reimbursement ratios are divided into the same group, and the distance i in the group is 5%.

N R Number of samples, P, for guarantee or responsibility of the same type of label G Percentiles of the levels within a group for each guarantee or term within the same group. And are not limited herein.

Step 103: and calculating the standard score of the guarantee or the responsibility by utilizing the percentage grade of each guarantee or responsibility in the same group.

In a specific embodiment, the criterion score T is calculated by the following formula.

T=50+10*Z pr 。

Wherein, Z pr Is rated in normal scaleCorresponding standard scores in the table.

In other embodiments, if the original value of quality of assurance or liability of the insurance product, e.g., the score, is continuous, e.g., average insurance claim age or total incidence probability of the assured disease. The criterion score T can be obtained directly by calculating by the following formula:

wherein, X is the original value of a sample of a certain guarantee or responsibility, such as premium. Mu is the mean of the guarantee or liability samples in the same group, and sigma is the standard deviation of the samples, and for example, in the claims, the actual parameters of the insurance product A are 10 days, i.e., the original value of the samples is 10 days, the mean value of the claims days of all insurance products of the same type is 11 days, and the mean value of the samples is 11 days.

Step 104: and performing weighted calculation on all the standard scores of guarantee or responsibility of the same insurance product according to a set proportion to obtain the evaluation score of the insurance product.

And after the standard scores of all the guarantees or responsibilities of a certain insurance product are obtained, weighting the standard scores of all the guarantees or responsibilities according to the preset weighting proportion, and summing to obtain the evaluation score of the insurance product.

Because the data volume involved in the evaluation of each guarantee or responsibility is large, the calculation and the character expression are performed in a vector manner in the embodiment, and the following formula is specifically shown:

wherein +>

And (4) a vector corresponding to the standard weight of each guarantee or responsibility.

A vector corresponding to the standard score of the guarantee or liability. In pair->

And &>

And after the inner product is calculated, the evaluation score of the insurance product can be obtained.

Referring to the following table, the following table lists the product scores and partial calculation data for one insurance product a:

wherein the evaluation score of insurance product A

After the evaluation score of the insurance product is obtained, the evaluation score is stored, so that the subsequent user can conveniently inquire and use the insurance product. In addition, in order to conveniently inquire the comparison condition of each dimension, namely the guarantee or responsibility of the same type, the percentage grade and the standard score of each guarantee or responsibility can be stored, so that a more comprehensive reference is provided for the user.

Different from the prior art, after the labeled insurance products are obtained, the guarantees or responsibilities with the same labeling type and quality grade of different insurance products are distributed to the same group, the percentage grade of each guarantee or responsibility in the same group is calculated, the standard score of the guarantee or responsibility is calculated by using the percentage grade, and the evaluation score of the insurance products is further obtained. Through the method for quantifying the responsibility or guarantee of the insurance products, all the insurance products can be reasonably evaluated to form reasonable comparison of all the insurance products, so that a user can visually and simply know the advantages and disadvantages of various insurance products to find the insurance product which is most suitable for the self requirement.

Since the evaluation score of an insurance product is generally an assessment of the quality of the product, normally, the higher the quality, i.e. the higher the premium, the faster the claim settlement. But the premium corresponding to insurance products with higher quality is also very high, and for general families or users, the trend is that the insurance products which are more suitable for the users are searched.

As shown in fig. 3, fig. 3 is a schematic flow chart of another embodiment of the evaluation method of the insurance product of the present application. The present embodiment differs from any of the above embodiments in that after the evaluation score of the insurance product is obtained, the step 305 of calculating the cost performance of the insurance product is further obtained.

The method specifically comprises the following steps:

step 301: and acquiring the marked insurance product.

This step is the same as step 101, and please refer to step 101 and the description of the relevant text, which are not described herein again.

Step 302: and distributing the guarantees or responsibilities with the same labeling type and quality grade of different insurance products to the same group, and calculating to obtain the percentage grade of each guarantee or responsibility in the same group.

This step is the same as step 102, and please refer to step 102 and the related text description thereof for details, which are not repeated herein.

Step 303: and calculating the standard score of the guarantee or the responsibility by utilizing the percentage grade of each guarantee or responsibility in the same group.

This step is the same as step 103, and please refer to step 103 and the description of the relevant text, which are not described herein again.

Step 304: and performing weighted calculation on all the standard scores of guarantee or responsibility of the same insurance product according to a set proportion to obtain the evaluation score of the insurance product.

This step is the same as step 104, and please refer to step 104 and the description of the relevant text specifically, which is not described herein again.

Step 305: and obtaining the cost performance of the insurance product according to the evaluation score of the insurance product and the premium of the insurance product.

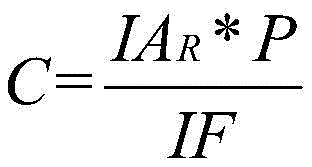

Specifically, the cost performance C of the insurance product is calculated by the following formula:

wherein, IA R IF is the premium and P is the evaluation score of the insurance product.

The premium and the premium are combined into the evaluation score of the insurance product to comprehensively calculate the cost performance of the insurance product, so that the user can know the performance at a glance, spend the least funds and obtain the insurance product which is most suitable for the user.

Further, the cost performance of the insurance product is stored. When the system is put into use and receives a query instruction sent by a user, according to the insurance product or the responsibility or guarantee of the insurance product included in the query instruction, the percentage grade of the responsibility or guarantee of the insurance product or the insurance product including the guarantee or the responsibility, the standard score or the evaluation score and the cost performance of the insurance product are queried and provided for the user so as to facilitate the reference of the user.

Referring to fig. 4, fig. 4 is a schematic structural diagram of an embodiment of an evaluation device for an insurance product according to the present application. In this embodiment, the evaluation device of the insurance product includes an acquisition module 401, a percentage rating calculation module 402, a criterion score calculation module 403, and an evaluation score calculation module 404.

The obtaining module 401 is configured to obtain a labeled insurance product; the labeling includes labeling the type and quality of each guarantee or liability of the insurance product.

Wherein, the marked comprises marking the types and the quality of each guarantee or responsibility of the insurance product. Generally, each insurance product has many terms, so that corresponding guarantees and responsibilities are also many, and in order to completely embody the quality or cost performance of the insurance product in the same type of products, the type and quality of each guarantee or responsibility of the insurance product are labeled. Wherein, marking the quality comprises marking the quality score or marking the quality annotation. And then, acquiring the quality grade of each guarantee or responsibility of the insurance product according to the quality label. Specifically, the quality grade may be obtained by grade distribution of the quality score of the label, or may be obtained by grading directly according to the quality annotation, which is not limited herein. Generally, a quality class includes a fractional segment, for example, 60 or less is D, 60 to 70 are C, 71 to 80 are B, and 81 to 100 are a.

The labeling of each guarantee or responsibility of the insurance product can be manually labeled. Or labeling may be performed by a labeling model first, and then labeling may be performed by a manual verification method, which is not limited herein.

The percentage level calculation module 402 is configured to assign guarantees or responsibilities with the same labeling type and quality level for different insurance products to the same group, and calculate a percentage level of each guarantee or responsibility in the same group.

Since many original values of quality of guarantee or responsibility of the insurance product, such as scores, do not have continuity and are not suitable for being directly evaluated by the standard score, the percentage grade is firstly converted into the continuous variable in the embodiment and then evaluated by the standard score method.

Wherein the insurance product can be a different type of insurance product. However, in order to provide contrast of insurance products of the same type and improve the practicability of the evaluation method, it is preferable that different insurance products in the present embodiment refer to insurance products of the same type, such as child insurance or old care insurance.

In the embodiment, the guarantees or responsibilities of the insurance products are quantified, and specifically, the percentage grade of each guarantee or responsibility is calculated to determine the quality of the guarantee or responsibility.

Specifically, the percentile level calculation module 402 allocates the guarantees or responsibilities of the same level of the same labeling type of different insurance products to the same group, and calculates the percentile of each guarantee or term in the same group.

Generally, the same dimension terms of the same type of insurance products, namely, the responsibilities and the contents of the guarantee of the same labeling type are basically the same and different, and the difference is generally in the size of the guarantee range, the amount of the guarantee or the severity of the conditions during reimbursement and the like. The same guarantee or responsibility of the insurance products of the same type are compared separately, so that a reference for a certain guarantee or responsibility can be provided for a user, and a reference is also provided for the quality of the subsequent calculation insurance products.

Specifically, in this embodiment, the percentage level calculation module 402 first counts the number of guarantees or responsibilities of all the same labeling types of the dimension, i.e. the number of samples N R . Then, quality labels, such as scores or grade annotations, such as optimal, worst and the like, are obtained from the labels of the guarantees or responsibilities of the insurance products, and the grade of each guarantee or responsibility in the dimension thereof is determined according to the quality, such as the grade of the score, according to the preset grade setting rule, such as one of the four grades A, B, C, D in the above example.

The percentage grade calculation module 402 assigns guarantees or responsibilities with the same annotation type and quality grade to the same group, sorts actual annotation quality or quality of specific content in the same group, and assigns a grade R in the group G And counting according to the number of samples of the guarantee or responsibility in the group to obtain the guarantee or responsibility in-group grade R G Percentile P of G 。

Further, the percentage rating calculation module 402 derives a percentage rating for each safeguard or liability based on the percentile and the number of samples of the insurance product.

Wherein, the percentage grade refers to the percentage of the number of times of scores lower than a certain preset score to the total number of times in a numerical sequence arranged according to the size sequence.

The specific percentage grade calculation module 402 calculates the percentage grade P by the following formula R 。

Wherein N is the total number of samples, cf, of the insurance product L Cumulative number of samples, P, for the level preceding the level for the guarantee or responsibility of the same group GL The lower limit of percentile in the same group, i is the group of percentile gradeInner distance, N R Number of samples, P, for guarantee or responsibility of the same type of label G Percentiles of the levels within a group for each guarantee or term within the same group.

The standard score calculating module 403 is used for calculating the standard score of the guarantee or responsibility by using the percentage grade of each guarantee or responsibility in the same group.

In a specific embodiment, the standard score calculating module 403 calculates the standard score T according to the following formula.

T=50+10*Z p r。

Wherein Z is pr And is a standard score corresponding to the percentage grade in the normal distribution table.

In other embodiments, if the original value of quality of assurance or liability of the insurance product, e.g., the score, is continuous, e.g., average insurance claim age or total incidence probability of the assured disease. The standard score calculation module 403 may obtain the standard score T directly by calculating with the following formula:

wherein, X is the original value of a sample of a certain guarantee or responsibility, such as premium. Mu is the sample mean of the guarantee or liability within the same group, and sigma is the sample standard deviation, and for example, in the claims, the actual parameters of the insurance product A are 10 days, i.e. the original value of the sample is 10 days, the mean value of the claim number of all the insurance products of the same type is 11 days, and then the sample mean value is 11 days.

The evaluation score calculating module 404 is configured to perform weighted calculation on all the standard scores of guarantee or liability of the same insurance product according to a set proportion to obtain an evaluation score of the insurance product.

After obtaining the standard scores of all the guarantees or responsibilities of a certain insurance product, the evaluation score calculating module 404 weights the standard scores of all the guarantees or responsibilities according to the preset weighting proportion, and the evaluation scores of the insurance product are obtained after summing.

Because the data volume involved in evaluating each guarantee or responsibility is large, in this embodiment, the evaluation score calculation module 404 performs calculation and text expression in a vector manner, specifically as shown in the following formula:

wherein it is present>

And (4) a vector corresponding to the standard weight of each guarantee or responsibility.

A vector corresponding to the standard score of the guarantee or liability. In pairs>

And &>

And after the inner product calculation is carried out, the evaluation score of the insurance product can be obtained.

After the evaluation score of the insurance product is obtained, the evaluation score is stored, so that the subsequent user can conveniently inquire and use the insurance product. In addition, in order to conveniently inquire the comparison condition of each dimension, namely the guarantee or responsibility of the same type, the percentage grade and the standard score of each guarantee or responsibility can be stored, so that a more comprehensive reference is provided for the user.

Different from the prior art, after the labeled insurance products are obtained, the guarantees or responsibilities with the same labeling type and quality grade of different insurance products are distributed to the same group, the percentage grade of each guarantee or responsibility in the same group is calculated, the standard score of the guarantee or responsibility is calculated by using the percentage grade, and the evaluation score of the insurance products is further obtained. Through the method for quantifying the responsibility or guarantee of the insurance products, all the insurance products can be reasonably evaluated to form reasonable comparison of all the insurance products, so that the purpose that the user can visually and simply know the quality of each insurance product and can find the insurance product which is most suitable for the user's own requirements is provided for the user.

Since the evaluation score of an insurance product is generally an assessment of the quality of the product, normally, the higher the quality, such as the higher the premium, the faster the claim settlement. But insurance products with higher quality are also very high in premium, and for general families or users, the trend of seeking insurance products more suitable for the users is a popular trend.

In another embodiment, as shown in fig. 5, fig. 5 is different from fig. 4 in that the evaluation device of the insurance product further includes a cost performance calculation module 505. The cost performance calculation module 505 is configured to obtain the cost performance of the insurance product according to the evaluation score of the insurance product and the premium of the insurance product.

Specifically, the cost performance calculating module 505 calculates the cost performance C of the insurance product by using the following formula:

wherein, IA R IF is the premium and P is the evaluation score of the insurance product.

The insurance product cost performance is comprehensively calculated by combining the insurance amount and the insurance fee into the evaluation score of the insurance product, so that the user can find the insurance product suitable for the user at a glance, spend the least capital and obtain the insurance product most suitable for the user.

Referring to fig. 6, fig. 6 is a schematic structural diagram of an embodiment of the intelligent system of the present application. The intelligent system is an intelligent customer service system or other intelligent terminals, network terminals, a PC and the like. The intelligent system 60 of this embodiment includes a human-computer interaction control circuit 602, and a processor 601 coupled to the human-computer interaction control circuit. A computer program executable on the processor 601. The processor 601, when executing the computer program, can implement the method for evaluating an insurance product according to any of the embodiments described in fig. 1 to 3 and the related text.

Referring to fig. 7, fig. 7 is a schematic structural diagram of a memory device according to an embodiment of the present disclosure. The application also provides a schematic structural diagram of an embodiment of the storage device. In this embodiment, the storage device 70 stores processor-executable computer instructions 71, and the computer instructions 71 are used for executing the method for evaluating an insurance product according to any one of the embodiments described in fig. 1 to 3 and the associated text.

The storage device 70 may be a medium that can store the computer instructions 71, such as a usb disk, a removable hard disk, a Read-Only Memory (ROM), a Random Access Memory (RAM), a magnetic disk or an optical disk, or may be a server that stores the computer instructions, and the server may send the stored computer instructions 71 to another device for operation or may self-operate the stored computer instructions.

In the several embodiments provided in the present application, it should be understood that the disclosed method and apparatus may be implemented in other manners. For example, the above-described apparatus embodiments are merely illustrative, e.g., a unit or division of units is merely a logical division, and other divisions may be realized in practice, e.g., a plurality of units or components may be combined or integrated into another system, or some features may be omitted, or not executed. In addition, the shown or discussed mutual coupling or direct coupling or communication connection may be an indirect coupling or communication connection through some interfaces, devices or units, and may be in an electrical, mechanical or other form.

The units described as separate parts may or may not be physically separate, and parts displayed as units may or may not be physical units, may be located in one position, or may be distributed on a plurality of network units. Some or all of the units can be selected according to actual needs to achieve the purpose of the embodiment.

In addition, functional units in the embodiments of the present application may be integrated into one processing unit, or each of the units may exist alone physically, or two or more units may be integrated into one unit. The integrated unit may be implemented in the form of hardware, or may also be implemented in the form of a software functional unit.

The integrated unit, if implemented in the form of a software functional unit and sold or used as a separate product, may be stored in a computer readable storage medium. Based on such understanding, the technical solutions of the present application, which are essential or contributing to the prior art, or all or part of the technical solutions may be embodied in the form of a software product, which is stored in a storage medium and includes several instructions for causing a computer device (which may be a personal computer, a server, a network device, or the like) or a processor (processor) to execute all or part of the steps of the methods of the embodiments of the present application. And the aforementioned storage medium includes: a U-disk, a removable hard disk, a Read-Only Memory (ROM), a Random Access Memory (RAM), a magnetic disk, or an optical disk, and various media capable of storing program codes.

The above embodiments are merely examples and are not intended to limit the scope of the present disclosure, and all modifications, equivalents, and flow charts using the contents of the specification and drawings of the present disclosure or those directly or indirectly applied to other related technical fields are intended to be included in the scope of the present disclosure.