[last updated in 10th July 2022]

These lecture notes are intended for econometrics training (originally used for new-hire training in the hedge fund that I was working in), suitable for university/grad students, data/quantitative analysts, junior business/economic/financial researchers and etc. The training are in two parts, the first part cover basic level and implementation in Python, the second part dive deeper into the econometric/statistical theory which is much more mathematical intensive.

This set of notes are rewritten from my MATLAB econometrics notes, which are outdated. I am still organizing the old materials.

The lectures notes are loosely based on several textbooks:

- Introduction to Econometrics, by Christopher Dougherty

- Introduction to Econometrics, by James H. Stock and Mark W. Watson

- Basic Econometrics, by Damodar N. Gujarati

The first part is introductory level, it requires trainees have basic knowledge of statistics and probability theory. The second part require linear algebra.

And you would benefit more from the tutorials if you have some skills of:

- NumPy

- Matplotlib

- Pandas

I strongly advise you to download all the files to view them on your PC, since nbviewer and Github has frequent rendering glitches.

Lecture 1 - Simple Linear R

8DF9

egression

Lecture 2 - Multiple Linear Regression, Multicollinearity and Heteroscedasticity

Lecture 3 - Practical Cases of Linear Regression

Lecture 4 - Dummy Variables

Lecture 5 - Nonlinear Regression

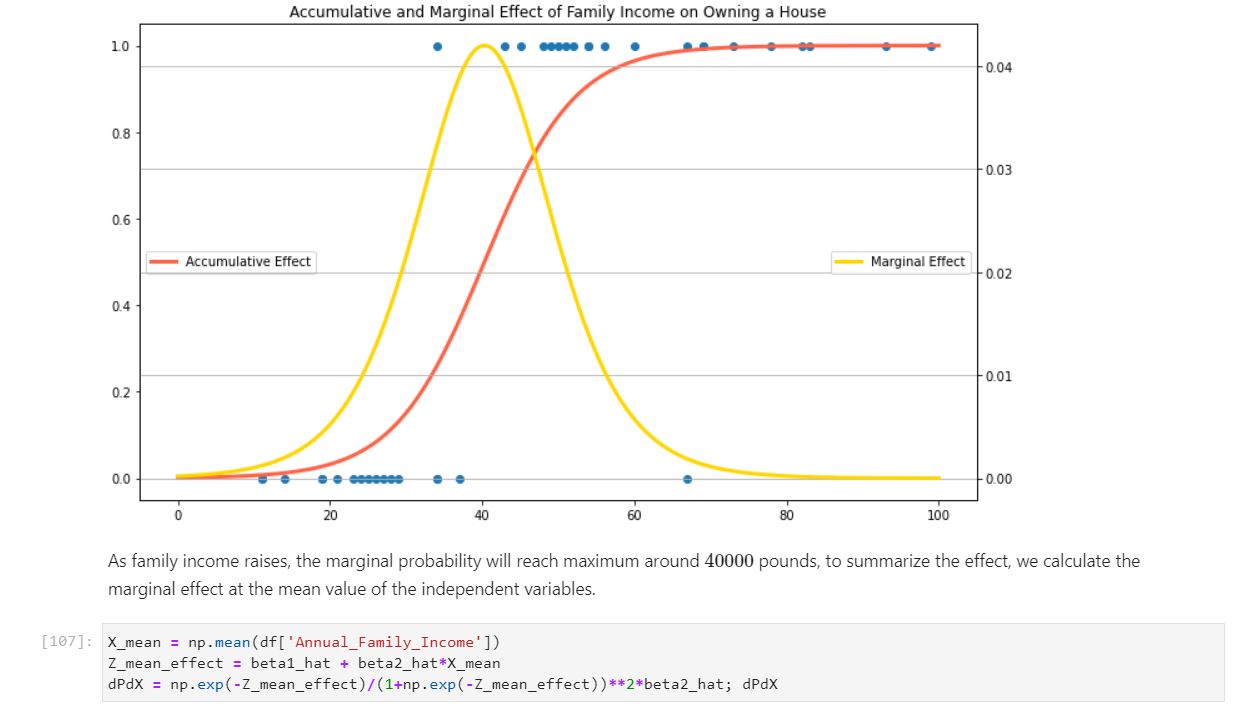

Lecture 6 - Qualitative Response Model

Lecture 7 - Model Specification

Lecture 8 - Identification and Simultaneous-Equation Models

Lecture 9 - Panel Data Analysis

Lecture 10 - Autocorrelation

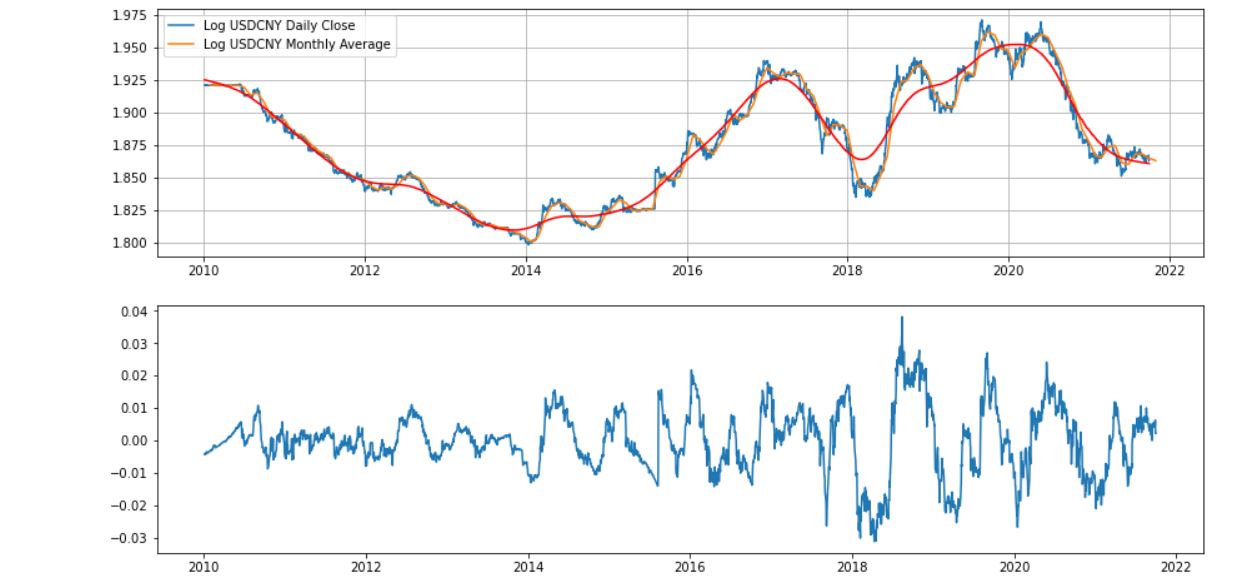

Lecture 11 - Time Series: Basics

Lecture 12 - Time Series: Forecast

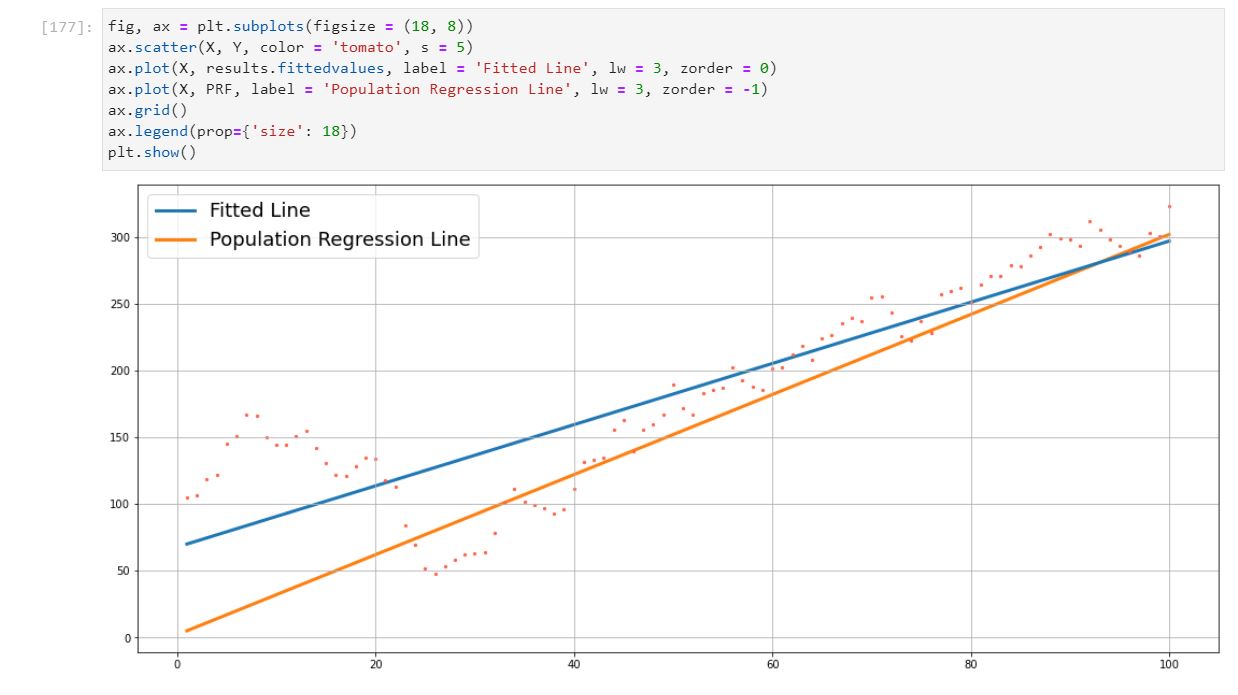

Lecture 1 - Geometry of OLS

Lecture 2 - Statistical Properties of OLS

Lecture 3 - Hypothesis Test and Confidence Interval