Chapter 6 -- Interest Rates

Interest rates

The determinants of interest rates

Term structure of interest rates and yield curves

What determines the shape of yield curves

Other factors

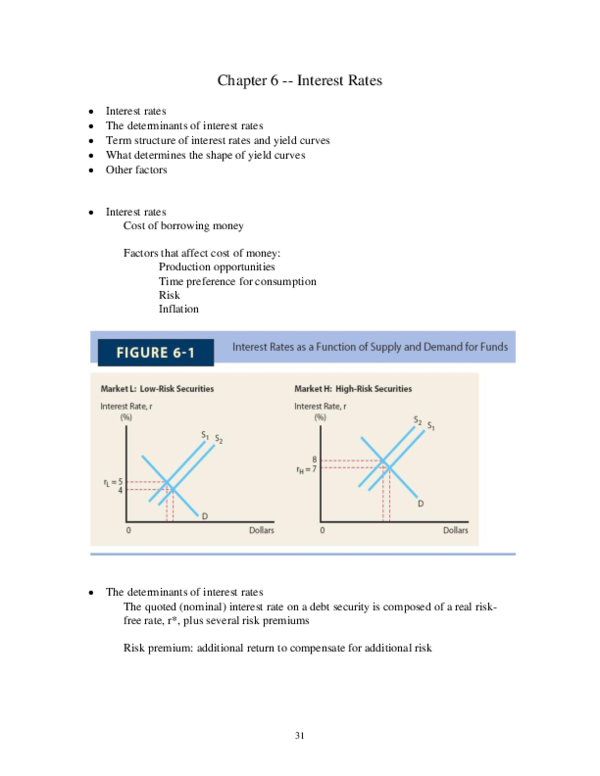

Interest rates

Cost of borrowing money

Factors that affect cost of money:

Production opportunities

Time preference for consumption

Risk

Inflation

The determinants of interest rates

The quoted (nominal) interest rate on a debt security is composed of a real riskfree rate, r*, plus several risk premiums

Risk premium: additional return to compensate for additional risk

31

�Quoted nominal return = r = r* + IP + DRP + MRP + LP

where, r = the quoted, or nominal rate on a given security

r* = real risk-free rate

IP = inflation premium (the average expected rate of inflation over the life

time of the security)

DRP = default risk premium

MRP = maturity risk premium

LP = liquidity premium

and r* + IP = rRF = nominal risk-free rate (T-bill rate)

Examples (online)

Term structure of interest rates and yield curves

Term structure of interest rates: the relationship between yields and maturities

Yield curve: a graph showing the relationship between yields and maturities

Normal yield curve (upward sloping)

Abnormal yield curve (downward sloping)

Humped yield curve (interest rates on medium-term maturities are higher than

both short-term and long-term maturities)

Term to maturity

1 year

5 years

10 years

30 years

Interest rate

0.4%

2.4%

3.7%

4.6%

Interest rate (%)

Years to maturity

What determines the shape of yield curves

Term structure theories

(1) Expectation theory: the shape of the yield curve depends on investor’s

expectations about future interest rates (inflation rates)

Forward rate: a future interest rate implied in the current interest rates

For example, a one-year T-bond yields 5% and a two-year T-bond yields 5.5%,

then the investors expect to yield 6% for the T-bond in the second year.

(1+5.5%)2 = (1+5%)(1+X), solve for X(forward rate) = 6.00238%

Approximation: (5.5%)*2 - 5% = 6%

32

�(2) Liquidity preference theory: other things constant, investors prefer to make

short-term loans, therefore, they would like to lend short-term funds at lower rates

Implication: keeping other things constant, we should observe normal yield

curves

Other factors

Fed policy: money supply and interest rates

Increase in money supply lowers short-term interest rates and stimulates the

economy but may lead to inflation in the future

Government budget deficit or surpluses: if government runs a huge deficit and

the debt must be covered by additional borrowing, which increases the demand

for funds and thus pushes up interest rates

33

�International perspective: trade deficit, country risk, exchange rate risk

Business activity: during recession, demand for funds decreases; during

expansion, demand for funds rises

Exercise

ST-1, ST-2, and ST-3

Problems: 2, 3, 5, 7, 9, 10*, 11, and 12*

Problem 10: expected inflation this year = 3% and it will be a constant but above

3% in year 2 and thereafter; r* = 2%; if the yield on a 3-year T-bond equals the

1-year T-bond yield plus 2%, what inflation rate is expected after year 1, assuming

MRP = 0 for both bonds?

Answer: yield on 1-year bond, r1 = 3% + 2% = 5%; yield on 3-year bond,

r3 = 5% + 2% = 7% = r* + IP3; so IP3 = 5%;

IP3 = (3% + x + x) / 3 = 5%, x = 6%

Problem 12: Given r* = 2.75%, inflation rates will be 2.5% in year 1, 3.2% in year

2, and 3.6% thereafter. If a 3-year T-bond yields 6.25% and a 5-year T-bond yields

6.8%, what is MRP5 - MRP3 (For T-bonds, DRP = 0 and LP = 0)?

Answer: IP3 = (2.5%+3.2%+3.6%)/3=3.1%; IP5 = (2.5%+3.2%+3.6%*3)/5=3.3%;

Yield on 3-year bond, r3=2.75%+3.1%+MRP3=6.25%, so MRP3=0.4%;

Yield on 5-year bond, r5=2.75%+3.3%+MRP5=6.8%, so MRP5=0.75%;

Therefore, MRP5 - MRP3 = 0.35%

Example: given the following interest rates for T-bonds, AA-rated corporate

bonds, and BBB-rated corporate bonds, assuming all bonds are liquid in the

market.

(c)

Years to maturity

1 year

5 years

10 years

T-bonds

5.5%

6.1

6.8

AA-rated bonds

6.7%

7.4

8.2

BBB-rate bonds

7.4%

8.1

9.1

The differences in interest rates among these bonds are caused primarily by

a.

b.

c.

d.

Inflation risk premium

Maturity risk premium

Default risk premium

Liquidity risk premium

34

�Chapter 7 -- Bond Valuation

Who issues bonds

Characteristics of bonds

Bond valuation

Important relationships in bond pricing

Bond rating

Bond markets

Who issues bonds

Bond: a long-term debt

Treasury bonds: issued by the federal government, no default risk

Municipal bonds (munis): issued by state and local governments with some

default risk - tax benefit (returns are tax exempt)

Corporate bonds: issued by corporations with different levels of default risk

Mortgage bonds: backed by fixed assets (first vs. second)

Debenture: not secured by a mortgage on specific property

Subordinated debenture: have claims on assets after the senior debt has been paid

off

Zero coupon bonds: no interest payments (coupon rate is zero)

Junk bonds: high risk, high yield bonds

Eurobonds: bonds issued outside the U.S. but pay interest and principal in U.S.

dollars

International bonds

Characteristics of bonds

Claim on assets and income

Par value (face value, M): the amount that is returned to the bondholder at

maturity, usually it is $1,000

Maturity date: a specific date on which the bond issuer returns the par value to the

bondholder

Coupon interest rate: the percentage of the par value of the bond paid out annually

to the bondholder in the form of interest

35

�Coupon payment (INT): annual interest payment

Fixed rate bonds vs. floating rate bonds

Zero coupon bond: a bond that pays no interest but sold at a discount below par

For example, a 6-year zero-coupon bond is selling at $675. The face value is

$1,000. What is the expected annual return? (I/YR = 6.77%)

0

-675

1

2

3

4

5

1000

6

PV = -675, FV = 1,000, N = 6, PMT = 0, solve for I/YR = 6.77%

Indenture: a legal agreement between the issuing firm and the bondholder

Call provision: gives the issuer the right to redeem (retire) the bonds under

specified terms prior to the normal maturity date

Convertible bonds: can be exchanged for common stock at the option of the

bondholder

Putable bonds: allows bondholders to sell the bond back to the company prior to

maturity at a prearranged price

Income bonds: pay interest only if it is earned

Sinking fund provision: requires the issuer to retire a portion of the bond issue

each year

Indexed bonds: interest payments are based on an inflation index

Required rate of return: minimum return that attracts the investor to buy a bond;

It serves as the discount rate (I/YR) in bond valuation

Bond valuation

Market value vs. intrinsic (fair) value

Market value: the actual market price, determined by the market conditions

Intrinsic value: the fair or fundamental value

36

�(1) Intrinsic value: present value of expected future cash flows, fair value

M

INT INT INT

INT

0

1

2

3

...

N

N

INT

M

, where INT is the annual coupon payment, M is the

VB

t

(1 rd ) N

t 1 (1 rd )

face value, and rd is the required rate of return on the bond

Annual and semiannual coupon payments using a financial calculator

Example: a 10-year bond carries a 6% coupon rate and pays interest annually. The

required rate of return of the bond is 8%. What should be the fair value of the

bond?

Answer: PMT = 60, FV = 1,000, I/YR = 8% (input 8), N = 10, solve for

PV = -$865.80

What should be the fair value if the bond pays semiannual interest?

Answer: PMT = 30, FV = 1,000, I/YR = 4% (input 4), N = 20, solve for

PV = -$864.10

Should you buy the bond if the market price of the bond is $910.00?

No, because the fair value is less than the market price (the bond in the market is

over-priced)

Discount bond: a bond that sells below its par value

Premium bond: a bond that sell above its par value

(2) Yield to maturity (YTM): the return from a bond if it is held to maturity

Example: a 10-year bond carries a 6% coupon rate and pays interest

semiannually. The market price of the bond is $910.00. What should be YTM for

the bond?

Answer: PMT = 30, FV = 1,000, PV = -$910.00, N = 20, solve for I/YR = 3.64%

YTM = 3.64%*2 = 7.28%

(3) Yield to call: the return from a bond if it is held until called

Example: a 10-year bond carries a 6% coupon rate and pays interest

semiannually. The market price of the bond is $910.00. The bond can be called

after 5 years at a call price of $1,050. What should be YTC for the bond?

Answer: PMT = 30, FV = 1,050, PV = -$910.00, N = 10, solve for I/YR = 4.55%

YTC = 4.55%*2 = 9.10%

37

�(4) Current yield (CY) = annual coupon payment / current market price

Example: a 10-year bond carries a 6% coupon rate and pays interest

semiannually. The market price of the bond is $910.00. What is CY for the bond?

Answer: CY = 60/910 = 6.59%

Important relationships in bond pricing

(1)

The value of a bond is inversely related to changes in the investor’s

present required rate of return (current interest rate); or

As interest rates increase, the value of a bond decreases

Interest rate risk: the variability in a bond value caused by changing

interest rates

Interest rate price risk: an increase in interest rates causes a decrease in

bond value

Interest reinvestment risk: a decrease in interest rates leads to a decline in

reinvestment income from a bond

(2)

If the required rate of return (or discount rate) is higher than the coupon

rate, the value of the bond will be less than the par value; and

If the required rate of return (or discount rate) is less than the coupon rate,

the value of the bond will be higher than the par value

(3)

As the maturity date approaches, the market value of a bond approaches

its par value

38

�(4)

Long-term bonds have greater interest rate risk than short-term bonds

(5)

The sensitivity of a bond’s value to changing interest rates depends not

only on the length of time to maturity, but also on the pattern of cash

flows provided by the bond (or coupon rates)

39

�

Bond rating

Importance: firm’s credit

Moody’s and S&P provide bond ratings

AAA

AA

A

Investment-grade bonds

BBB

BB

B

Junk bonds

.

Criteria to consider

Financial ratios: for example, debt ratio and interest coverage ratio

Qualitative factors: for example, contract terms, subordinated issues, etc.

Other factors: for example, profitability ratios and firm size

Bond markets

OTC markets

Quotes: quoted as a % of par value of $100

Invoice price (dirty price) = quoted price (clear price) + accrued interest

0

182 days

62 days

120 days remaining until next coupon

Suppose annual coupon is $60 ($30 in 6 months) and the quoted price is 95.500,

Invoice price = 955 + (62/182)*30 = $965.22 = 955.00 + 10.22

where $955 is the quoted price and $10.22 is the accrued interest

40

�

Exercise

ST-1 and ST-2

Problems: 5, 8, 9, 10, 13, and 15*

Problem 15: bond X has 20 years to maturity, a 9% annual coupon, and a $1,000

face value. The required rate of return is 10%. Suppose you want to buy the bond

and you plan to hold the bond for 5 years. You expect that in 5 years, the yield to

maturity on a 15-year bond with similar risk will be priced to yield 8.5%. How

much would you like to pay for the bond today?

0

90

1

…

…

90

5

90

6

…

…

90

19

1,000

90

20

PV5 =1,041.52 (I/YR=8.5%, PMT=90, N=15, FV=1,000)

PV0 = 987.87 (I/YR=10%, PMT=90, N=5, FV=1,041.52)

Answer:

Step 1: figure out what should be the fair value of the bond after 5 years (PV5)

Step 2: figure out what should be the fair value of the bond now (PV0)

41

�

Chapter 8 -- Risk and Rates of Return

Investment returns

Risk

Expected rate of return and standard deviation

Diversification

Beta coefficient - market risk

Return on a portfolio and portfolio beta

Relationship between risk and rates of return

Investment returns

Dollar return vs. rate of return

If you invested $1,000 and received $1,100 in return, then

your dollar return = 1,100 - 1,000 = $100 and

your rate of return = (1,100 - 1,000) / 1,000 = 10%

Risk

The chance that some unfavorable event will occur

Stand-alone risk vs. market risk

Stand-alone risk: risk of holding one asset measured by standard deviation

Market risk: risk of holding a well-diversified portfolio measured by beta

Expected rate of return and standard deviation

Probability distribution: a list of possible outcomes with a probability assigned to

each outcome

Expected rate of return: the rate of return expected to be realized

42

�Expected rate of return = r Pi ri

Variance and standard deviation: statistical measures of variability (risk)

N

^

Variance = 2 =

P (r r )

N

i 1

^

i

i

i 1

2

and

Standard deviation = 2

Coefficient of variation (CV) = standard deviation / expected rate of return,

which measures the risk per unit of expected return

Example: probability distribution for Martin Products vs. U.S. Water

Example: calculation of standard deviation (risk) for Martin Products

43

�Using historical data to estimate average return and standard deviation

Stock returns: expected vs. realized

68. 26%

95. 44%

99. 74%

Expected return

Using Excel to calculate mean and standard deviation with historical data

Risk premium: the difference between the expected/required rate of return on a

given security and that on a risk-free asset

44

�

Diversification

As you increase the number of securities in your portfolio, the portfolio total risk

decreases

Total risk = firm’s specific risk + market risk

Total risk = diversifiable risk + nondiversifiable risk

Total risk = unsystematice risk + systematic risk

Beta coefficient - market risk

Sensitivity of an asset (or a portfolio) with respect to the market or the extent to

which a given stock’s returns move up and down with the stock market

Plot historical returns for a firm along with the market returns (S&P 500 index,

for example) and estimate the best-fit line. The estimated slope of the line is the

estimated beta coefficient of the stock, or the market risk of the stock.

45

�

Return on a portfolio and portfolio beta

Expected return on a portfolio: the weighted average of the expected returns on

the assets held in the portfolio

rp wi ri

^

N

^

i 1

46

�For example, the expected rate of return on stock A is 10% and the expected rate

of return on stock B is 14%. If you invest 40% of your money in stock A and 60%

of your money in stock B to form your portfolio then the expected rate of return

on your portfolio will be 12.4% = (0.4)*10% + (0.6)*14%*

Portfolio beta: weighted average of individual securities’ betas in the portfolio

b p wi bi

N

i 1

For example, if the beta for stock A is 0.8 and the beta for stock B is 1.2, with the

weights given above, the beta for your portfolio is 1.04 = (0.4)*0.8 + (0.6)*1.2

Relationship between risk and rates of return

Required rate of return: the minimum rate of return necessary to attract an investor

to purchase or hold a security

Market risk premium: the additional return over the risk-free rate needed to

compensate investors for assuming an average amount (market) of risk

RPM rM rRF

For example, if the required rate of return on the market is 11% and the risk-free

rare is 6% then the market risk premium will be 5%

Risk premium for a stock: the additional return over the risk-free rate needed to

compensate investors for assuming the risk of that stock

RPi ri rRF

For example, if the required rate of return on a stock is 15% and the risk-free rare

is 6% then the risk premium for that stock will be 9%

Capital Asset Pricing Model (CAPM)

ri rRF (rM rRF )bi

where ri is the required rate of return on stock i; rRF is the risk-free rate;

(rm – rRF) is the market risk premium; bi is the market risk for stock i, and

(rm – rRF) bi is the risk premium of stock i

47

�Security market line (SML): a line that shows the relationship between the

required return of an asset and the market risk

Overvalued vs. undervalued securities

If the actual return lies above the SML, the security is undervalued

If the actual return lies below the SML, the security is overvalued

Example: a stock has a beta of 0.8 and an expected rate of return of 11%. The

expected rate of return on the market is 12% and the risk-free rate is 4%. Should

you buy the stock?

Answer: required rate of return for the stock (using CAPM) is

4% + (12% - 4%)*(0.8) = 10.4% < 11% (expected rate of return)

The stock is under-valued

48

�The impact of inflation: a parallel shift in SML

Change in risk aversion: the slope of SML gets steeper

49

�Change in beta: changes the required rate of return

Some concerns about beta and the CAPM and multivariable models

Exercise

ST-1 and ST-3

Problems: 1, 2, 3, 7, 8, 9, and 13*

Problem 13: given the information about stocks X, Y, and Z below (X, Y, and Z

are positively but not perfectly correlated), assuming stock market equilibrium:

Stock

X

Y

Z

Expected Return

9.00%

10.75%

12.50%

Standard Deviation

15%

15%

15%

Beta

0.8

1.2

1.6

Fund Q has one-third of its funds invested in each of the three stocks; rRF is 5.5%

a. What is the market risk premium?

Applying CAPM to stock X and use the formula ri rRF (rM rRF )bi

9.00% = 5.50% + (rM – rRF)*0.8, solve for rM - rRF = 4.375%

b. What is the beta of Fund Q?

bQ = (1/3)*(0.8) + (1/3)*(1.2) + (1/3)*(1.6) = 1.20

c. What is the expected (required) rate of return on Fund Q?

Applying CAPM to Fund Q, rQ = 5.50% + (4.375%)*1.2 = 10.75%

d. What would be the standard deviation of Fund Q (>15%, =15%, or <15%)?

It should be less than 15% due to diversification (positive but not perfect)

50

�Chapter 9 -- Stock Valuation

Characteristics of common stock

Common stock valuation

Valuing a corporation

Preferred stock

Characteristics of common stock

Ownership in a corporation: control of the firm

Claim on income: residual claim on income

Claim on assets: residual claim on assets

Commonly used terms: voting rights, proxy, proxy fight, takeover, preemptive

right, classified stock, and limited liability

Common stock valuation

Stock price vs. intrinsic value: a revisit

Growth rate g: expected rate of growth in dividends

g = ROE * retention ratio

Retention ratio = 1 - dividend payout ratio

The growth rate, g plays an important role in stock valuation

The general dividend discount model: P0

^

t 1

Dt

(1 rs ) t

Rationale: estimate the intrinsic value for the stock and compare it with the

market price to determine if the stock in the market is over-priced or under-priced

(1) Zero growth model (the dividend growth rate, g = 0)

^

D

It is a perpetuity model: P0

rs

For example, if D = $2.00 and rs = 10%, then P0 $20

^

If the market price (P0) is $22, what should you do?

You should not buy it because the stock is over-priced

51

�(2) Constant growth model (the dividend growth rate, g = constant)

^

D * (1 g )

D1

0

P0

rs g

rs g

^

2 * (1 5%)

For example, if D0 = $2.00, g = 5%, rs = 10%, then P0

$42

0.10 0.05

If the market price (P0) is $40, what should you do?

You should buy it because the stock is under-priced

Common stock valuation: estimate the expected rate of return given the market

price for a constant growth stock

Expected return = expected dividend yield + expected capital gains yield

^

D * (1 g )

D

g

rs 1 g 0

P0

P0

In the above example,

^

D * (1 g )

2.00 * (1 0.05)

rs 0

g

0.05 0.0525 0.05 10.25%

P0

40

where 5.25% is the expected dividend yield and 5% is the expected capital gains

yield (stock price will increase at 5% per year)

What would be the expected dividend yield and capital gains yield under the zero

growth model?

Expected capital gains yield, g = 0 (price will remain constant)

Expected dividend yield = D/P0

(3) Non-constant growth model: part of the firm’s cycle in which it grows much

faster for the first N years and gradually return to a constant growth rate

Apply the constant growth model at the end of year N and then discount all

expected future cash flows to the present

D0

0

D1

1

D2

2

…

…

DN

N

Non-constant growth, gs

DN+1

N+1

…

Constant growth, gn

^

DN 1

Horizon value PN

rs g n

52

�For example N = 3 gs = 30%, gn = 8%, D0 = $1.15, and rs = 13.4%

D4 = 2.7287, P3 53.0576 , and P0 39.2134

^

^

53

�

Valuing a corporation

It is similar to valuing a stock

V = present value of expected future free cash flows

FCF = EBIT*(1-T) + depreciation and amortization – (capital expenditures + in

net working capital)

The discount rate should be the WACC (weighted average cost of capital)

Preferred stock

A hybrid security because it has both common stock and bond features

Claim on assets and income: has priority over common stocks but after bonds

Cumulative feature: all past unpaid dividends should be paid before any dividend

can be paid to common stock shareholders

Valuation of preferred stock

Expected return = rP

DP

PP

Example: if a preferred stock pays $2 per share annual dividend and has a

required rate of return of 10%, then the fair value of the stock should be $20

^

Intrinsic value = Vp = Dp / rp

and

Exercises

ST-1, ST-2, and ST-3

Problems: 10, 11, and 13*

Problem 13: given D1 = $2.00, beta = 0.9, risk-free rate = 5.6%, market risk

premium = 6%, current stock price = $25, and the market is in equilibrium

^

Question: what should be the stock price in 3 years ( P3 )?

Answer: required return = expected return = 5.6% + 6%*0.9 = 11%

Expected dividend yield = D1/P0 = 2/25 = 8%

Expected capital gains yield = g = 11% - 8% = 3%

^

Expected stock price after 3 years P3 = 25*(1+3%)3 = $27.32

Or D4 = D1*(1+g)3 = 2*(1+3%)3 = $2.1855 and then apply the constant growth

model

^

D4

2.1855

P3

$27.32

rs g 0.11 0.03

54

�Chapter 10 -- Cost of Capital

Capital components

Cost of debt

Cost of preferred stock

Cost of retained earnings

Cost of new common stock

Weighted average cost of capital (WACC)

Adjusting the cost of capital for risk

Capital components

Debt: debt financing

Preferred stock: preferred stock financing

Equity: equity financing (internal vs. external)

Internal: retained earnings

External: new common stock

Weighted average cost of capital (WACC)

Cost of debt

Recall the bond valuation formula

Replace VB by the net price of the bond and solve for I/YR

I/YR = rd (cost of debt before tax)

Net price = market price - flotation cost

If we ignore flotation costs which are generally small, we can just use the actual

market price to calculate rd

Cost of debt after tax = cost of debt before tax (1-T) = rd (1-T)

Example: if a firm can issue a 10-year 8% coupon bond with a face value of

$1,000 to raise money. The firm pays interest semiannually. The net price for

each bond is $950. What is the cost of debt before tax? If the firm’s marginal tax

rate is 40%, what is the cost of debt after tax?

Answer: PMT = -40, FV = -1,000, N = 20, PV = 950, solve for I/YR = 4.38%

Cost of debt before tax = rd = 8.76%

Cost of debt after tax = rd*(1-T) = 8.76*(1-0.4) = 5.26%

55

�

Cost of preferred stock

Recall the preferred stock valuation formula

Replace Vp by the net price and solve for rp (cost of preferred stock)

Net price = market price - flotation cost

If we ignore flotation costs, we can just use the actual market price to calculate rp

D

rP P

PP

Example: a firm can issue preferred stock to raise money. The net price is $40 and

the firm pays $4.00 dividend per year. What is the cost of preferred stock?

Answer: 4/40 = 10%

Cost of retained earnings

CAPM approach

ri rRF (rM rRF )bi

DCF approach

^

D (1 g )

D

g

rs 1 g 0

P0

P0

Bond yield plus risk premium approach

rs = bond yield + risk premium

When must a firm use external equity financing?

R/E

Retained earning breakpoint = ----------------% of equity

It is the dollar amount of capital beyond which new common stock must be issued

For example, suppose the target capital structure for XYZ is 40% debt, 10%

preferred stock and 50% equity. If the firm’s net income is $5,000,000 and the

dividend payout ratio is 40% (i.e., the firm pays out $2,000,000 as cash dividend

and retains $3,000,000), then the retained earning breakpoint will be

3,000,000

--------------- = $6,000,000,

50%

which means that if XYZ needs to raise more than $6,000,000 it has to issue new

common stock

56

�

Cost of new common stock

D (1 g )

D1

re

g , where F is the flotation cost

g 0

P0 (1 F )

P0 (1 F )

Weighted average cost of capital (WACC)

Target capital structure: the percentages (weights) of debt, preferred stock, and

common equity that will maximize the firm’s stock price

WACC = wd rd (1-T) + wp rp + wc (rs or re)

Comprehensive example

Rollins Corporation is constructing its MCC schedule. Its target capital structure

is 20% debt, 20% preferred stock, and 60% common equity. Its bonds have a

12% coupon, paid semiannually, a current maturity of 20 years, and a net price of

$960. The firm could sell, at par, $100 preferred stock that pays a $10 annual

dividend, but flotation costs of 5% would be incurred. Rollins’ beta is 1.5, the

risk-free rate is 4%, and the market return is 12%. Rollins is a constant growth

firm which just paid a dividend of $2.00, sells for $27.00 per share, and has a

growth rate of 8%. Flotation cost on new common stock is 6%, and the firm’s

marginal tax rate is 40%.

a) What is Rollins’ component cost of debt before and after tax?

Answer:

Cost of debt before tax = 12.55%

Cost of debt after tax = 7.53%

b) What is Rollins’ cost of preferred stock?

Answer:

Cost of P/S = 10.53%

c) What is Rollins’ cost of R/E using the CAPM approach?

Answer:

Cost of R/E = 16%

d) What is the firm’s cost of R/E using the DCF approach?

Answer:

Cost of R/E = 16%

e) What is Rollins WACC if it uses debt, preferred stock, and R/E to raise money?

Answer:

WACC (R/E) = 13.21%

f) What is Rollins’ WACC once it starts using new common stock financing?

Answer:

Cost of N/C = 16.51%

WACC (N/C) = 13.52%

57

�

Adjusting the cost of capital for risk

Exercise

ST-1 and ST-2

Problems: 6, 7, 8, and 10

58

�

noname untell

noname untell