A Multi-Sectoral Agent-Based Monetary Model

of Transition to a Low-Carbon Economy

Extended Abstract for the European Social Simulation Association’s 2012 Conference

Brett W. Parris 1, Behrooz Hassani-M. and Elle Saber

Department of Econometrics & Business Statistics

Monash University, Clayton VIC, 3800 Australia

Introduction

Two of the greatest challenges of our age are the tasks of transitioning to low-carbon economies in

order to mitigate climate change, and of restoring financial balance and stability. The resulting more

stable, low-carbon economies must in turn deliver sustainable and equitable livelihoods.

The ‘Great Crash’ of 2008 laid bare the limitations of much modern macroeconomic theory and

analysis (Kirman 2010, Ormerod 2010, Keen 2011, Wray 2011). Even the former Chairman of the US

Federal Reserve, Alan Greenspan, remarked:

Those of us who have looked to the self-interest of lending institutions to protect shareholders’

equity, myself included, are in a state of shocked disbelief. … This modern risk-management

paradigm held sway for decades. The whole intellectual edifice, however, collapsed in the summer

of last year (Andrews, 2008).

In reference to the Great Crash, it is often asserted that ‘no-one saw it coming’. But as Bezemer

(2009, 2011) showed, this is simply untrue. Several economists did in fact predict not only the

impending ‘reality check’ of the Great Crash, but just as importantly, its timing and its origins. A

common feature of their analysis was the use of flow-of-funds models which keep track of debt levels,

firm balance sheets and financial disequilibria, rather than assuming a neoclassical equilibrium

framework (see e.g. Keen 2011a,b, Godley & Lavoie, 2007). The work of Hyman Minsky (1982,

1986) also features prominently in their analysis – for example Keen (2011a) and Wray (2012).

As noted by Beale et al. (2011), a system-wide perspective is also essential, since actions that may

reduce risk for individual firms in isolation may, and indeed did, make the financial system as a whole

far more fragile. While regulators tried to keep up with rapid innovations at the firm level, very few

were absorbing the implications of these firm-level activities for the system as a whole.

Meanwhile, the limitations of neoclassical economic models of climate change and integrated

assessment models (IEMs) have been extensively documented (e.g. DeCanio 2003, Ackerman 2008,

Ackerman et al. 2009, Ackerman & Stanton 2011). One of the key limitations with such models is the

omission of financial realities such as firm balance sheets, debt levels, credit and equity markets,

insurance premia and so on. These omissions are critical for two reasons: Firstly because the

economic impacts of climate change may be vastly underestimated by omitting financial market

effects (Michael 2007). And secondly, because it is not simply the end state of a low-carbon economy

that must be depicted. Just as important is the viability of the transition path that shows that getting

there is feasible. It is no longer adequate, if it ever was, to adopt the traditional comparative statics

approach of much economic analysis, in which ‘before’ and ‘after’ snapshots of an economy in

equilibrium are taken and a viable transition path between them is simply assumed.

1

Address for correspondence: brett.parris@monash.edu

1

�One of the most influential IEMs has been Nordhaus’s Dynamic Integrated model of Climate and the

Economy (DICE) model (see e.g. Nordhaus 2007a,b and 2008). Nordhaus has used this model to

argue against the need for urgent action on climate change, claiming that the Stern Review (Stern

2007) reached novel conclusions by giving too great a weight to the future (in technical terms, using

too low a discount rate), which did not reflect actual discount rates reflected in market interest rates.

To say that Nordhaus’s approach causes consternation among those who think that the future in 100

years should be valued at greater than nothing, is something of an understatement, as DeCanio (2003)

and Ackerman et al. (2009) attest.

Australia’s Garnaut Review (Garnaut 2008, 2011) used a more sophisticated modelling approach,

linking models of different species, but again, this state-of-the-art effort was hampered by the lack of

availability of integrated monetary and biophysical models that could adequately reflect the impacts

of climate change on the economy and society. These impacts include not only its direct physical

impacts such as drought, bushfires and sea-level rise, but also the reverberations through the

economic and financial systems of those impacts and of efforts to adapt to and mitigate climate

change.

New models are needed that integrate the real, financial, social and biophysical dimensions of

economies so that they can more realistically model the transition paths needed to ensure a more

sustainable future. This extended abstract reports on work in progress towards such a model.

The Model

The model builds on several recent contributions, including Dosi et al. (2008, 2010), Godley and

Lavoie (2007 and 2012), and Keen (2010, 2011a and 2012). The model is implemented in NetLogo

(Wilensky 1999).

The question of scale and the inter-relationships between different levels of the system is critical (Ahl

& Allen 1996; Manson 2008). Some agent-based models have millions of agents, with a separate

agent for every individual. ABMs inevitably face a trade-off between numbers of agents and their

interactions, and the computational burden and speed of execution. Our aim in this model is to

represent and integrate key elements of the system, more as a proof of concept, rather than seeking

detailed, calibrated fidelity at the level of individual people and firms. The actions of individual

people, households and firms are nevertheless important for the evolution of economic systems. We

have therefore adopted the approach of using ‘super-individuals’ (Scheffer et al. 1995) where

individual people, households and firms have relationships and act in ways appropriate to individuals,

but the amounts they consume, produce, borrow and so on are far greater than ‘normal’ individuals. In

this way an individual may represent many hundreds of individuals. Similar questions pertain to the

spatial and temporal resolutions – finer-grained representations permit greater fidelity to real-world

processes, but again, dramatically increase the computational burden and complexity of the model. At

the time of writing this abstract we are still determining the precise numbers and resolutions necessary

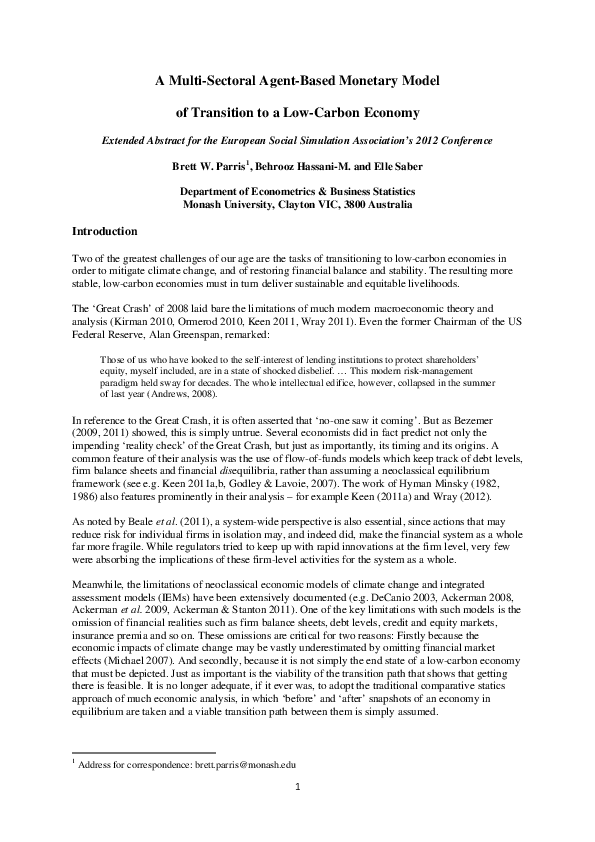

to give the best mix for our purposes. It is not possible to describe the model in detail in a short

abstract, but Figure 1 gives an indication of the principle classes and flows of funds.

Workers (W) are members of Households (HH), which include children (CH, not shown) who must be

nourished and educated in order to become productive workers. Workers work for Firms (F) and

Government (G) and receive wages (w) for their labour (L). Households must pay taxes to the

Government and must purchase the products of the different kinds of Firms to survive.

There are two primary types of Firms: Banks (B) and NonBankFirms (NBF). NonBankFirms are

further subdivided into four main industry sectors: agricultural firms (AgFirms, AF), manufacturing

firms (ManfFirms, MF) and two kinds of EnergyFirms (EF) – fossil energy firms

(FossilEnergyFirms, FEF) which are greenhouse gas emissions-intensive and renewable energy firms

(RenEnergyFirms, REF) which are far less emissions-intensive. Energy is critical, not simply because

2

�the focus here is on the transition to a low-carbon economy, but because too often energy is not given

its due weight in considerations of the crucial drivers of economic growth (Frondel & Schmidt, 2004).

Figure 1. Class diagram of the main features and flows in the model

All four types of NonBankFirms require finance from banks. AgFirms require inputs from

EnergyFirms and ManfFirms as well as arable land and water (not shown in Figure 1); EnergyFirms

require inputs from ManfFirms and EnergyFirms; and ManfFirms require inputs from EnergyFirms

and ManfFirms. Households require inputs from energy, agriculture (food) and manufacturing. Inputs

are purchased with money or credit flowing between the relevant accounts and prices are absolute

rather than relative price ratios.

The NonBankFirms rely on the Banks for credit and must pay the banks interest on borrowed funds.

Firms pay taxes to the Government and also issue equity (e, not shown). Firms must also innovate to

improve their energy efficiency and product offerings in order to survive. Following Schumpeter

(1934), the extension of credit to firms is an essential ingredient in the process of innovation, which in

turn is arguably the major driver of economic development.

The Government receives taxes (t) from Workers and Firms and must spend a certain proportion of

funds on health (HL), education (ED), social security (SOS) and infrastructure (INF) to maintain a

productive economy and stable society. The Government must also survive an ‘election’ every three

to four years, based on its popularity with Workers. If the Government loses the election, an

alternative set of policies is introduced. The two sets of policies available to the Government agent are

based on policies reflective of ‘Conservative/Republican’ and ‘Democrat/Labour/Green’ parties in the

Western democracies. This aspect of the model can be developed to incorporate an important spatial

aspect of the transition, namely the fact that certain geographical areas are affected more than others,

particularly those in which fossil-fuel intensive industries are concentrated, or those which stand to

gain from the transition through, for example, investment in renewable energy industries.

3

�In common with most ABMs, the model contains considerable stochasticity, particularly in the ways

in which agents are interact. Random numbers are used in a variety of ways in the construction of the

agents and in their interactions as the system evolves. Since all computer-generated random numbers

are deterministic however, these are strictly speaking only ‘pseudo-random’ numbers rather than true

random numbers. Model runs can be replicated precisely by setting and using the same random ‘seed’

number for the random number generator. We use this feature by incrementally increasing the random

seed for multiple model runs to ensure that the results are not an artefact of a particular random seed.

The key challenge for the Government, Households and Firms is to manage the transition from a

fossil-fuel intensive economy to a low-carbon economy. Substantial emissions reductions must be

undertaken between 2010 and 2050, in accordance with the recommendations of the

Intergovernmental Panel on Climate Change (IPCC, 2007). This implies that energy production and

use in the economy must become far less emissions-intensive. This in turn implies that appropriate

policies must be put in place to encourage such a transition without causing financial instability, credit

crunches or unnecessary bankruptcies of otherwise viable firms. Since these policies must also be

voted into place in democratic countries, low unemployment, financial stability and social cohesion is

vital to the transition.

The ABM incorporates likely long-term impacts of climate change such as lower agricultural

productivity and rising sea-levels, as well as discrete disaster events such as cyclones, bushfires and

heatwaves. These different types of climate impacts are treated distinctly rather than lumping them

together in the form of a ‘damage curve’ as is common with many IEMs.

Conclusion

This model is part of a wider research program intended to help provide a bridge between some of the

most insightful analyses of modern monetary economics and financial instability, and the integrated

assessment literature modelling potential transition paths to low-carbon economies. An agent-based

modelling framework is ideally suited to such a task by providing a dynamic, spatial environment in

which large numbers of heterogeneous agents can interact and evolve.

Acknowledgements

We are grateful to two anonymous reviewers for helpful comments.

References

Ackerman, F., (2008) Can We Afford the Future? The Economics of a Warming World, The New Economics

Series; Zed Books, London & New York, viii +151 pp.

Ackerman, F., DeCanio, S.J., Howarth, R.B. and Sheeran, K., (2009) "Limitations of Integrated Assessment

Models of Climate Change", Climatic Change, Vol. 95, No. 3-4, August, pp. 297-315.

Ackerman, F. and Stanton, E.A., (2011) Climate Economics: The State of the Art, Stockholm & Somerville MA,

Stockholm Environment Institute, November, 148 pp. http://sei-us.org/publications/id/417

Ahl, V. and Allen, T.F.H., (1996) Hierarchy Theory: A Vision, Vocabulary, and Epistemology, Colombia

University Press, New York, 206 pp.

Andrews, E.L., (2008) "Greenspan Concedes Error in Regulation", New York Times, 23 October, p. B1.

http://www.nytimes.com/2008/10/24/business/economy/24panel.html

Beale, N., Rand, D.G., Battey, H., Croxson, K., May, R.M. and Nowak, M.A., (2011) "Individual versus

Systemic Risk and the Regulator's Dilemma", Proceedings of the National Academy of Sciences, Vol. 108, No.

31, 2 August, pp. 12647-12652. http://www.pnas.org/content/108/31/12647.abstract

4

�Bezemer, D.J., (2009) "“No One Saw This Coming”: Understanding Financial Crisis Through Accounting

Models", Munich University, Munich Personal RePEc Archive, MPRA Paper No. 15892, 16 June, 50 pp.

http://mpra.ub.uni-muenchen.de/15892/

Bezemer, D.J., (2011) "The Credit Crisis and Recession as a Paradigm Test", Journal of Economic Issues, Vol.

45, No. 1, March, pp. 1-18.

DeCanio, S.J., (2003) Economic Models of Climate Change: A Critique, Palgrave Macmillan, New York &

Houndmills, Basingstoke, UK, xiii + 203 pp.

Dosi, G., Fagiolo, G. and Roventini, A., (2008) "The Microfoundations of Business Cycles: An Evolutionary,

Multi-Agent Model", Journal of Evolutionary Economics, Vol. 18, No. 3, August, pp. 413-432.

Dosi, G., Fagiolo, G. and Roventini, A., (2010) "Schumpeter Meeting Keynes: A Policy-Friendly Model of

Endogenous Growth and Business Cycles", Journal of Economic Dynamics and Control, Vol. 34, No. 9,

September, pp. 1748-1767.

Frondel, M. and Schmidt, C.M., (2004) "Facing the Truth about Separability: Nothing Works without Energy",

Ecological Economics, Vol. 51, No. 3-4, December, pp. 217-223.

Garnaut, R., (2008) The Garnaut Climate Change Review: Final Report, Cambridge University Press,

Melbourne, xlv + 616 pp.

Garnaut, R., (2011) The Garnaut Review 2011: Australia in the Global Response to Climate Change,

Cambridge University Press, Cambridge, Melbourne & New York, xx + 221 pp.

Godley, W. and Lavoie, M., (2007) "Fiscal Policy in a Stock-Flow Consistent (SFC) Model", Journal of Post

Keynesian Economics, Vol. 30, No. 1, Fall, pp. 79-100.

Godley, W. and Lavoie, M., (2012) Monetary Economics: An Integrated Approach to Credit, Money, Income,

Production and Wealth, 2nd Edition; Palgave Macmillan, Houndmills, Basingstoke & New York, xlvi+ 530 pp.

IPCC, (2007) Climate Change 2007: Mitigation. Contribution of Working Group III to the Fourth Assessment

Report of the Intergovernmental Panel on Climate Change, ed. Metz, B., Davidson, O.R., Bosch, P.R., Dave, R.

and Meyer, L.A.; Cambridge University Press, Cambridge & New York, pp. viii + 851.

Keen, S., (2010) "Solving the Paradox of Monetary Profits", Economics: The Open-Access, Open-Assessment EJournal, Vol. 4, No. 2010-31, 28 October, pp. 1-32.

http://www.economics-ejournal.org/economics/journalarticles/2010-31

Keen, S., (2011a) "A Monetary Minsky Model of the Great Moderation and the Great Recession", Journal of

Economic Behavior & Organization, In press, Corrected proof, Online 1 February pp. 1-15.

Keen, S., (2011b) Debunking Economics - Revised and Expanded Edition: The Naked Emperor Dethroned?,

Zed Books, London & New York, xviii + 478 pp.

Keen, S., (2012) "A Dynamic Monetary Multi-sectoral Model of Production", Unpublished manuscript,

University of Western Sydney, 1-29 pp. http://www.debtdeflation.com/blogs

Kirman, A., (2010) "The Economic Crisis is a Crisis for Economic Theory", CESifo Economic Studies, Vol. 56,

No. 4, December, pp. 498-535. http://cesifo.oxfordjournals.org/content/56/4/498.abstract

Manson, S.M., (2008) "Does Scale Exist? An Epistemological Scale Continuum for Complex HumanEnvironment Systems", Geoforum, Vol. 39, No. 2, March, pp. 776-788.

Michael, J.A., (2007) "Episodic Flooding and the Cost of Sea-level Rise", Ecological Economics, Vol. 63, No.

1, 15 June, pp. 149-159.

Minsky, H.P., (1982) Can "It" Happen Again? Essays on Instability and Finance, M.E. Sharpe, Armonk NY &

London, xxiv + 301 pp.

5

�Minsky, H.P., (1986) Stabilizing an Unstable Economy, McGraw Hill, New York, 2008 Edition, xxxv + 395 pp.

Nordhaus, W.D., (2007a) "A Review of the Stern Review on the Economics of Climate Change", Journal of

Economic Literature, Vol. 45, No. 3, September, pp. 686-702.

Nordhaus, W.D., (2007b) "Critical Assumptions in the Stern Review on Climate Change", Science, Vol. 317,

No. 5835, 13 July, pp. 201-202.

Nordhaus, W.D., (2008) A Question of Balance: Weighing the Options on Global Warming Policies, Yale

University Press, Boston MA, 256 pp.

Ormerod, P., (2010) "The Current Crisis and the Culpability of Macroeconomic Theory", Twenty-First Century

Society, Vol. 5, No. 1, February, pp. 5-18. http://www.paulormerod.com/pdf/accsoct09%20br.pdf

Scheffer, M., Baveco, J.M., DeAngelis, D.L., Rose, K.A. and van Nes, E.H., (1995) "Super-Individuals: A

Simple Solution for Modelling Large Populations on an Individual Basis", Ecological Modelling, Vol. 80, No.

2-3, July, pp. 161-170.

Schumpeter, J.A., (1934) The Theory of Economic Development: An Enquiry into Profits, Capital, Credit,

Interest and the Business Cycle, Transaction Publishers reprint, 1983, New Brunswick NJ & London; trans.

from the 2nd German edition of 1926 by Redvers Opie, lxiv + 255 pp.

Wilensky, U., (1999) "NetLogo", http://ccl.northwestern.edu/netlogo/, Evanston, IL, Center for Connected

Learning and Computer-Based Modeling, Northwestern University.

Wray, L.R., (2011) "The Dismal State of Macroeconomics and the Opportunity for a New Beginning", Working

Paper No. 652, Annandale-on-Hudson, NY, Levy Economics Institute of Bard College, March, 22 pp.

http://www.levyinstitute.org/pubs/wp_652.pdf

Wray, L.R., (2012) "Global Financial Crisis: A Minskyan Interpretation of the Causes, the Fed's Bailout, and the

Future", Working Paper No. 711, Annandale-on-Hudson, NY, Levy Economics Institute of Bard College,

March, 30 pp. http://www.levyinstitute.org/pubs/wp_711.pdf

6

�

Brett Parris

Brett Parris Elle Saber

Elle Saber