A Novel Evolving Clustering Algorithm with Polynomial

Regression for Chaotic Time-Series Prediction

Harya Widiputra1, Henry Kho2, Lukas3

1

Knowledge Engineering and Discovery Research Institute,

Auckland University of Technology, New Zealand

2

Faculty of Information and Technology, Swiss German University, BSD City, Indonesia

3

Cognitive Engineering Research Group (CERG), Universitas Katolik Atma Jaya, Indonesia

1

{harya.widiputra}@aut.ac.nz

2

{henry}@student.sgu.ac.id

3

{lukas}@atmajaya.ac.id

Abstract. Time-series prediction has been a very well researched topic in

recent studies. Some popular approaches to this problem are the traditional

statistical methods e.g. multiple linear regression and moving average, and

neural network with the Multi Layer Perceptron which has shown its supremacy

in time-series prediction. In this study, we used a different approach based on

evolving clustering algorithm with polynomial regressions to find repeating

local patterns in a time-series data. To illustrate chaotic time-series data we

have taken into account the use of stock price data from Indonesian stock

exchange market and currency exchange rate data. In addition, we have also

conducted a benchmark test using the Mackey Glass data set. Results showed

that the algorithm offers a considerably high accuracy in time-series prediction

and could also reveal repeating patterns of movement from the past.

Keywords: evolving clustering algorithm, polynomial regression, chaotic timeseries data

1

Introduction

Chaotic time-series prediction has become a very well-liked topic for research and

there have been a number of methods from different fields introduced before to solve

this problem. Some very popular approaches for time-series prediction come from

traditional statistic approaches, i.e. linear regression, multiple linear regressions, and

moving average [5]. Other than that, various models and algorithms from the machine

learning and data mining fields have also been introduced (e.g. Multi Layer

Perceptron, Pattern Recognition, and Support Vector Machine) [4], [8], [9]. All of

these approaches have shown their strength in solving the time-series prediction

problem by presenting a good-quality of accuracy in predicting future values,

however not much new knowledge can be revealed and learned from these models.

�2

Harya Widiputra, Henry Kho, Lukas

A breakthrough was made by [7] with the Dynamic Evolving Neuro-Fuzzy

Inference System (DENFIS) in which the algorithm was not only able to give good

accuracy in predicting movement of time-series data, but it was also able to extract

new knowledge in the form of sets of fuzzy rules which govern the movement of the

series. This has stimulated us to make an effort to mine knowledge about the

existence of repeating patterns in a time-series movement, particularly in a chaotic

time-series data (e.g. stock prices, exchange rates), and then to use extracted

knowledge to predict future movement of the series. We are aiming to represent the

rules in the form of repeating polynomial functions, group them based on their

likeness, and do prediction for future value by trying to discover similar patterns from

the past that can be associated with current condition. In addition, we also expect the

algorithm to acquire the ability to evolve when new data sample comes, therefore it

would be able to adapt when new problems emerge.

In this study, we used in general two different types of data set as experimental

data, which are; (1) the financial data set consists of the Indonesian stock prices data

and some currency exchange rates as these data can be considered as a Complex

Dynamic System (CDS) [5], and (2) a benchmark data set which in this case is the

Mackey Glass data set.

2

Clustering as Local Modeling

One of the challenges in information science is to be able to represent dynamic

systems, model them and then to reveal the rules that govern the behavior of the

variables over time [3]. An option to build a complete model of a dynamic system is

by clustering comparable problem sets from a complete problem space based on

certain condition into different groups. A model then can be created for each group

(i.e. a local regression), and by combining all models from each cluster it will

constitute a complete model which might be able to cover all problems from the

complete problem space [1], [2], [6]. Similarity in this case is usually (but not limited

to) determined by calculating a Euclidean distance between two data samples [5].

We developed a new algorithm which will extract pattern from a localized data set

or a chunk of data (as a sub-space problem from a complete problem space) using a

polynomial regression. Extracted patterns (in forms of polynomial functions) then will

be grouped based on the likeness of their shape (trend of movement). We believe that

repeating patterns of movement exist in a time-series data based on [2], [5], [7], even

in a chaotic one, and it can be used to predict future values.

2.1

Similarity and Distance Measurement

Defining similarity between two objects in clustering process is a very important step.

Different definition about similarity would give us diverse solutions or various groups

of data. In a clustering process, it is common to use the Euclidean distance to measure

similarity between objects [5]. This can be done by calculating distance from each

attributes that we used to describe the object.

�A Novel Evolving Clustering Algorithm with Polynomial Regression

3

Nonetheless, in our algorithm it will not be suitable to apply the Euclidean

distance, as what we would like to group are not objects but sets of polynomial

function which represent patterns of movement of a time-series data across time.

Therefore, we applied a different method to calculate similarity between two

polynomial functions, which is the Angular Separation or Cosine distance (equation

1). By using the Cosine distance, we were able to measure similarity between two

polynomial functions based on the shape and direction of the function. As for the

attributes that we used to describe a polynomial function, we took into consideration

the coefficients of each part of the polynomial function.

(1)

2.2

ECM as Evolving Clustering Algorithm

Evolving Clustering Method (ECM) was introduced by [6]. ECM is a fast, one-pass

algorithm for dynamic clustering of an input stream of data. It is a distance-based

clustering method where the cluster centres are represented by evolved nodes in an

on-line mode. In the clustering process, the data samples come from a data stream and

this process starts with an empty set of clusters. As new data samples come, new

clusters are created or if the new data sample is similar to those previous ones, it will

be added into one of the existing clusters and the cluster centre will be updated.

ECM is used in Dynamic Evolving Neuro-Fuzzy Inference Systems (DENFIS) [7].

In our proposed algorithm, we have also implemented ECM as the core evolving

clustering algorithm. Nevertheless, we have also made a fundamental change in the

algorithm. ECM uses the Euclidean distance to measure similarity between objects

when it creates or updates clusters. In our algorithm, we replaced the Euclidean

distance with Cosine distance. The main reason of this modification is explained in

sub-chapter 2.1.

2.3

DyCPR as a Novel Evolving Clustering Algorithm for Time-Series

Prediction

We named the proposed algorithm Dynamic Clustering with Polynomial Regression

(DyCPR). The main idea behind the algorithm is to extract patterns of movement

from a time-series data using a polynomial regression. After the patterns have been

extracted, it will be grouped using the modified ECM algorithm. Cluster centres will

represent the average movement calculated as a superposition function from all

polynomial functions belong to the cluster. These cluster centres will be used as

references to predict movement of the series by finding a centre that can be related

with current condition. Complete algorithm of DyCPR is described as follow;

�4

Harya Widiputra, Henry Kho, Lukas

• Step 0: First step of the algorithm is considered to be a data pre-processing step. In

this step the algorithm, we will calculate the difference of values from the timeseries data. difft = xt+1-xt, where difft is value difference at time t and X are actual

value at time point t+1 and t respectively. The motive why the algorithm calculates

values difference from time-series data is, because it is the movement of values

difference that will be predicted instead of the actual value.

• Step 1: After values difference has been calculated, the next step of the algorithm

is to find the best-fit regression function from a chunk of data, Xi with size n. For

every chunk of data which comes in, the best-fit regression function will be

extracted by calculating linear regression and polynomial regression up to certain

order (i.e. up to 6th order). PFi = {LRi, PR1i, PR2i, PR3i, PR4i, PR5i, PR6i} best-fit

regression function is defined by calculating bestPF = minMSE(PFi). Besides

calculating the best-fit regression function from the chunk of data with size n, the

algorithm will also calculated best-fit regression function for next movement,

PFMi using another chunk of data with the size n+1, Yi.

• Step 2: For the first chunk of data, found bestPF will become the cluster centre of

the first cluster, Ccj = bestPFi and the function to predict next movement of data

samples that belong to that cluster is set to PFMi. The radius of the cluster, Ruj is

set to 0. If there is no more chunks of data comes then the algorithm stops. If there

are still more chunks of data then the algorithm returns to Step 1, where the best-fit

regression function will be calculated again. After the bestPFi is calculated for Xi,

similarity between bestPFi with the Cc is measured. Similarity is calculated using

Cosine distance by taking coefficients of bestPFi function and Cc function into

account.

• Step 3: The forth step of the algorithm is basically the implementation of the ECM

algorithm, where the algorithm will calculate distance between bestPFi to all

existing cluster centres, Cc and makes update to cluster centre j, Ccj when it is

found that distance between bestPFi and Ccj is less than 2xDthr. The process of

updating the value of cluster radius, Ruj is the same as it is in ECM. However

DyCPR will update also the best-fit regression function for next movement of

cluster j, PFMj by calculating superposition value between existing PFMj and

PFMi when it decides that bestPFi belongs to cluster j. If all chunks of data sample

have been processed than the algorithm stops, else it returns to Step 1.

• Step 4: In the prediction step, the algorithm will calculate the best-fit regression

function from current chunk of data with size n, Xt = {xt, xt-1, xt-2, …, xt-(n-1)}.

Calculated best-fit regression function for time t, bestPFt, then will be compared to

all existing cluster centres, Cc. When closest Ccj is found, then PFMj will be used

as a reference function to calculate next movement of values differences, pxt+1.

Predicted actual value then will be calculated as, xt+1 = xt + pxt+1. Learning process

then will be continued by taking new data sample as a data sample to update

existing clusters and the algorithm returns to Step 1.

One key characteristics of DyCPR (other than its power to evolve by creating and

updating clusters when new data sample becomes available) is that the algorithm will

do prediction of future values by predicting the polynomial function that will

represent movement of the series in the future (this is explained in Step 1 and 3 in the

�A Novel Evolving Clustering Algorithm with Polynomial Regression

5

DyCPR algorithm). This is significantly different in comparison to DENFIS where

the algorithm does prediction by calculating real predicted values based on extracted

fuzzy rules represent by each cluster centres [7].

3

Experiments and Results

In this study, we used data from financial field as experimental data. These data are;

(1) data of five stock prices from Indonesian stock market (namely TLKMJK,

AALIJK, LMASJK, KLBFJK, and ELTYJK; data are available from:

http://finance.yahoo.com/q/cp?s=^JKSE) and (2) currency exchange rates data (i.e.

NZD to USD and IDR to USD) 1 . The five stock prices data represent three different

types of movement, which are; chaotic, increasing and decreasing. The stock prices

data cover period of January 2005 to January 2009, while the currency exchange rates

data expand from January 2006 to January 2009. As for benchmark data, we use the

Mackey Glass data set to examine the robustness of the algorithm. Figure 1 illustrates

movement of the Indonesian stock price data for ELTYJK data.

Fig. 1. Daily basis data (closing price) of ELTYJK in Indonesian stock exchange market

spanning from January 2005 to January 2009.

No normalization process applied to the data before the training process is started. On

the other hand, what will be extracted are patterns of movement of difference between

values across time instead of movement of the actual values (as it has been explained

in Step 1 in DyCPR algorithm).

Results showed that the algorithm demonstrated its strength by giving a

considerable high accuracy of prediction results (with RMSE of 2.4680 and 0.2449

for ELTYJK data and LMASJK data respectively; please note the RMSE is unnormalized RMSE). This can be seen in figure 2 and 3, where we attached prediction

results for two stock prices data with different behavior which are; (1) ELTYJK data

with increasing trend and (2) LMASJK data with decreasing trend, here we used 80%

1

NZD is New Zealand Dollar, USD is United States Dollar and IDR is Indonesian Rupiah

�6

Harya Widiputra, Henry Kho, Lukas

of total data set records as training set and 20% as test set. Even more, the algorithm

showed its ability to adapt to new problems (unusual pattern of movement) which did

not appear during the training step as in the case of LMASJK data for the last view

points (i.e. a flat-line pattern).

Fig. 2. Comparation of predicted value (in dashed line) and actual value (in solid line) for

ELTYJK data set on testing set. Number of training set is 850 and number of testing set is 200.

To predict value at t+1, values from time point t, t-1, t-2, t-3, t-4, t-5, t-6, t-7, t-8, and t-9 are

used to find the best fit polynomial regression. Distance threshold used in DyCPR is 0.3.

Fig. 3. Comparation of predicted value (in dashed line) and actual value (in solid line) for

LMASJK data set on testing set. Number of training set is 750 and number of testing set is 180.

To predict value at t+1, values from time point t, t-1, t-2, t-3, t-4, t-5, t-6, t-7, t-8, and t-9 are

used to find the best fit polynomial regression. Distance threshold used in DyCPR is 0.3.

As it is expected, the algorithm was not only able to provide excellent accuracy in

predicting future values, it was also capable to extract new knowledge in the form of

repeating polynomial functions which exist in the series over time. This can be seen in

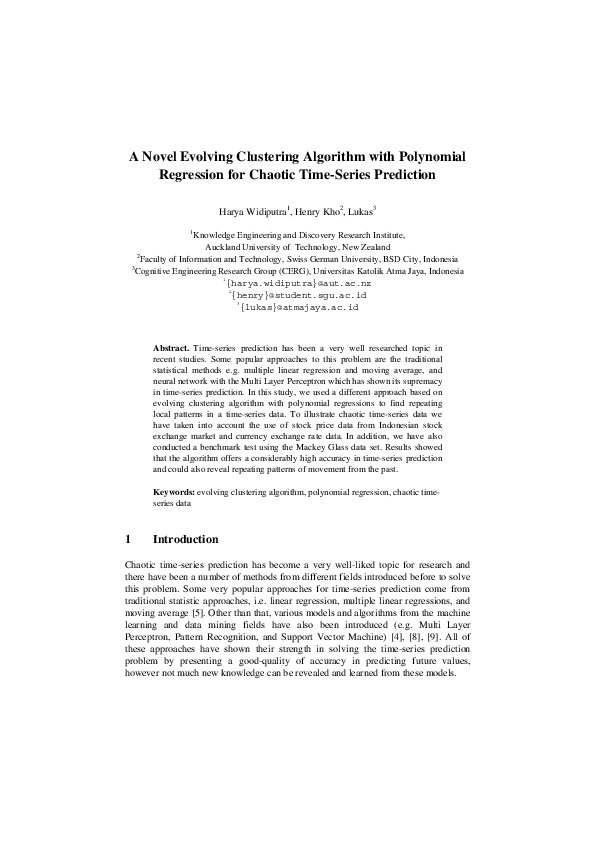

the clusters the algorithm created as showed in figure 4 for the ELTYJK data.

From figure 4, we can observe how the polynomial functions are being grouped

into different clusters, and how the cluster centres represent the average movement

�A Novel Evolving Clustering Algorithm with Polynomial Regression

7

function for each group. This finding justified our assumption that repeating patterns

of movement do exist in a time-series data, and that it can be modeled using a

polynomial functions. We have also conducted a benchmark test using the Mackey

Glass data set as part of our experiment. Complete results of our experiments with the

other data sets can be seen in table 1.

Fig. 4. Created clusters during training and testing process when predicting movement of stock

price difference for ELTYJK data. Each clusters show comparable patterns of movement based

on the likeness of shape and direction of extracted polynomial regression for each chunk of

data. Cluster centres (in wider line) represent movement of all polynomial functions which

belong to a cluster, are calculated as superposition functions.

Results from table 1 showed that the algorithm demonstrated its superiority in

chaotic time-series prediction. The algorithm is also effective to predict movement of

different types of time-series data with different behaviours (e.g. fluctuative,

increasing, and decreasing).

Table 1. Results of DyCPR used to predict 8 different types of data set covering stock prices

data set, currency exchange rate data set, and the Mackey Glass data set. 80% of data is used as

training set and 20% as testing set for each experiments. Value of distance threshold, Dthr in

DyCPR is set to 0.3.

Data Set

TLKMJK

AALIJK

LMASJK

ELTYJK

KLBFJK

NZDUSD

IDRUSD

Mackey Glass

Category

Indonesian Stock Price

Indonesian Stock Price

Indonesian Stock Price

Indonesian Stock Price

Indonesian Stock Price

Exchange Rate

Exchange Rate

Benchmark Data

Trend

Increasing

Fluctuate

Decreasing

Fluctuate

Fluctuate

Balanced

Decreasing

Fluctuate

Range of Values

3,853.9-11,933.0

346.0-32,026.0

35.0-1,304.8

331.75-1,508.4

10.0-680.0

1.2235-1.9058

8,684.0-12,209.0

0.2192-1.3137

RMSE

34.0077

109.3862

0.2449

2.4680

3.1927

0.0083

72.6284

0.0057

�8

Harya Widiputra, Henry Kho, Lukas

4

Conclusion and Future Works

Dynamic Clustering with Polynomial Regression (DyCPR) showed its strength by

giving high accuracy in predicting movement of chaotic time-series data. The

robustness of the algorithm has also been tested by conducting experiment using

different data sets with different behaviours. Furthermore, proposed algorithm was

also able to extract repeating patterns of movement from chaotic time-series data. It

has also been verified that by using polynomial regressions to model patterns of

movement in a localized sub-space of time-series data, we were able to acquire

prediction of next movement with a considerably high accuracy.

As for future works, we would like to extend the algorithm so it can be used to

predict movement of not only a single chaotic time-series data but for multiple timeseries data as well. One possibility to achieve this is by implementing a recursive

clustering method, where the first clustering process will group data from different

series into a number of groups with comparable behaviour, and the second clustering

process will be to extract patterns of movement from created clusters in the first step.

References

1. Kasabov, N.: Adaptation and interaction in dynamical systems: Modelling and

rule discovery through evolving connectionist systems. Applied Soft Computing

6: 307-322, (2006)

2. Kasabov, N.: Global, local and personalised modelling and pattern discovery in

bioinformatics: An integrated approach. Pattern Recognition Letters 28: 673-685,

(2007)

3. Kasabov, N.: Evolving Connectionist Systems: The Knowledge Engineering

Approach. Springer, (2007)

4. Kim, T., Adali, T.: Approximation by Fully Complex Multilayer Perceptrons.

Neural Computation 15: 1641-1666, (2003)

5. Serguieva, A., Kalganova, T., Khan, T.: An intelligent system for risk

classification of stock investment projects. Journal of Applied Systems Studies 4

(2): 236-261, (2003)

6. Song, Q., Kasabov, N.: ECM – A Novel On-line Evolving Clustering Method and

Its Applications. In: Posner, M.I. (Ed.), Foundations of cognitive science: 631682, (2001)

7. Song, Q., Kasabov, N.: Dynamic evolving neuro-fuzzy inference system

(DENFIS): On-line learning and application for time-series prediction. IEEE

Transactions of Fuzzy Systems 10: 144-154, (2002)

8. Yang, H., Chan L., King, I.: Support Vector Machine Regression for Volatile

Stock Market Prediction. Lecture Notes in Computer Science 0302: 143-152,

(2002)

9. Zanghui, Z., Yau, H., Fu, A.M.N.: A new stock price prediction method based on

pattern classification. In: International Joint Conference on Neural Network 1999:

3866-3870, (1999)

�

Russel Pears

Russel Pears Lukas Lukas

Lukas Lukas